Stormy final week of July shouldn’t blow markets off course

What happened to investment markets in July? Our latest update examines the trends.

3 min read

SHARE

Become A Client

When you become a client of Coutts, you will be part of an exclusive network.

Investor confidence faltered at the end of last month but we think the long-term trend is positive.

July saw generally positive returns, before markets stuttered in the last week in light of Q2 GDP data showing the economic damage caused by coronavirus lockdowns. Most markets still ended the month positive in local currency terms, although the UK and Europe gave back all the gains they’d made in the month up to that point.

We’ve never anticipated the market recovery as being a straight line pointing up, and this kind of reality check in the wake of new data was to be expected. And while the economic data made for grim reading, markets remained broadly resilient against the backdrop of rising infections. The coronavirus pandemic has now moved from being a worrying question mark for investors to a quantifiable, and therefore manageable, event.

It’s also worth remembering that GDP data is backward-looking. Forward-looking measures such as Purchasing Manager Indices, which survey companies about incoming business, suggest that economic activity is returning, and in the longer term we see the economic growth trend as positive.

“Forward-looking measures such as Purchasing Manager Indices, which survey companies about incoming business, suggest that economic activity is returning, and in the longer term we see the economic growth trend as positive.”

EU deal strikes a chord with investors

The big news in July came out of Europe as the European Union agreed a €750 billion recovery package for EU countries. As well as the scale of the stimulus measures, the agreement evidenced a renewed commitment to cooperation in the EU, with debt obligations shared between all members rather than falling on the poorer countries that will be the main beneficiaries.

The announcement bolstered European markets and strengthened our own confidence in European equities. We added to our exposure in July on the basis of the firm foundation that the new deal provides to the region’s businesses.

Read more about the EU agreement and its impact for investors

Market jitters rein-in performance

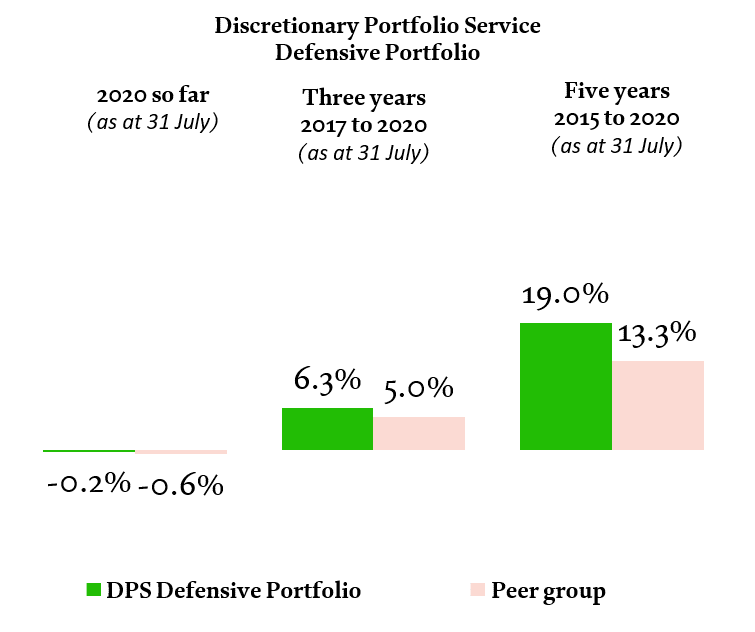

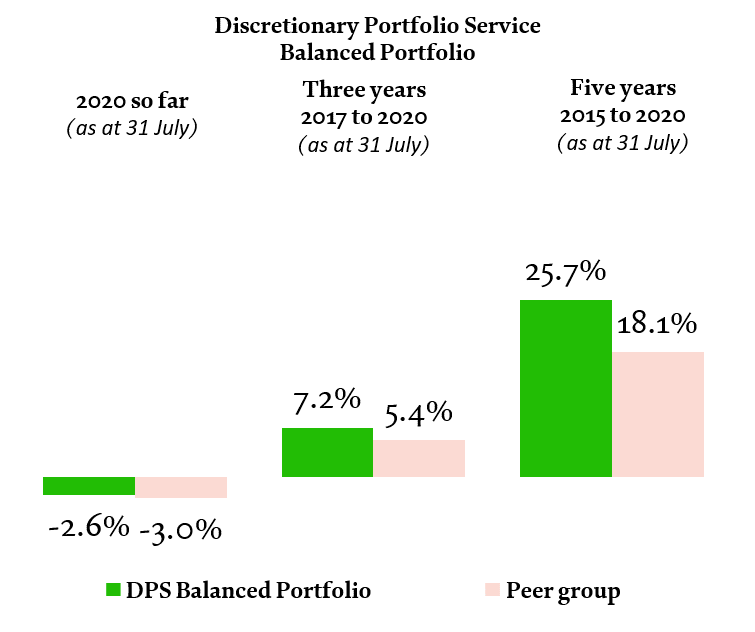

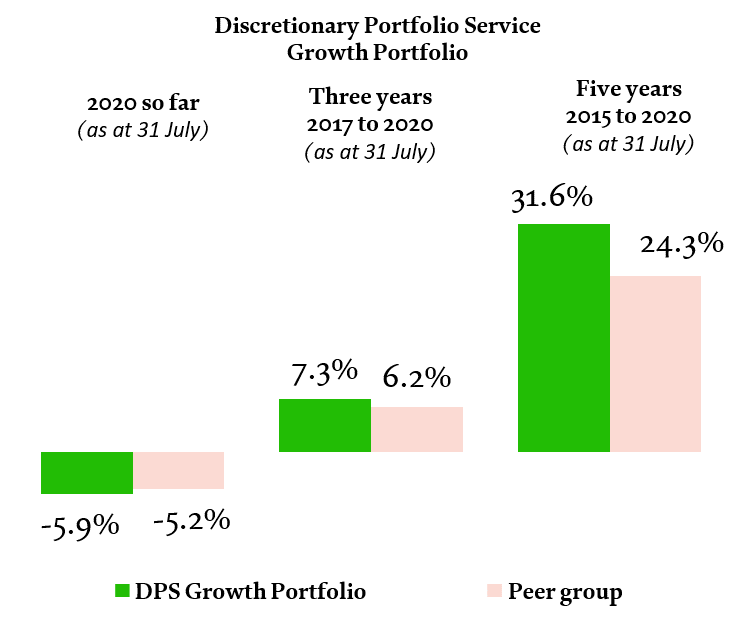

Despite good returns in the first weeks of July, volatility at the end of the month was tough for portfolios with high equity exposure. The average growth portfolio gave back the gains made at the beginning of the month to end down by -0.7%, while the average balanced portfolio fell -0.4%. Our lower-risk strategies were more resilient and ended the month flat.

Cumulative returns calculated on sterling basis, including fees, charges and income to 31 July 2020. These data are based on composite performance, individual portfolio monthly returns are asset-weighted based on their respective asset values at the beginning of the month. Peer group returns provided by Asset Risk Consultants (ARC); end-July data represents ARC estimate. Past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can go down as well as up and you may not recover the amount of your original investment. Sources: Coutts & Co, ARC. August 2020.

Emerging markets thrive under weaker dollar

US dollar weakness in July was positive for emerging market equitiess and our holdings – including our small direct allocation to China – were particularly helpful in boosting the overall performance of our portfolios as other markets fell.

We’ve added to our overall emerging market holdings in July, as part of our tilt towards more economically sensitive sectors. We believe that as the global economy recovers from the lockdown measures imposed by the coronavirus response, these are the parts of the market that stand to benefit the most.

A stronger pound, on the other hand, reduced the value of returns from investments in non-sterling assets – in particular, in US dollar and yen-based assets – which was a drag on performance for sterling-based investors.

Low interest rates make yields harder to find

Or view on interest rates has been ‘lower for longer’ for some time, but the COVID-19 pandemic means we now think they’ll be even lower for even longer. We outlined our reasons for thinking this and the significance for investors in our recent article Down for a decade - why interest rates are going nowhere.

This has a number of knock-on effects for our investment decisions, in particular our positions in government bonds where yields are likely to be very low for the foreseeable future. Our recent addition of gold in funds and portfolios reflects our view that yields on government bonds are less compelling than the potential medium-term return from the precious metal.

|

30 June 2015 to 30 June 2016 |

30 June 2016 to 30 June 2017 |

30 June 2017 to 30 June 2018 |

30 June 2018 to 30 June 2019 |

30 June 2019 to 30 June 2020 |

MSCI UK Index (total return) |

-3.4% |

16.7% |

8.2% |

-1.6% |

-0.8% |

MSCI Emerging Markets Index (total return) |

3.5% |

27.4% |

6.5% |

5.0% |

-0.5% |

Coutts Defensive Portfolio |

4.0% |

7.7% |

1.7% |

3.1% |

1.8% |

Defensive strategy benchmark |

10.0% |

5.4% |

3.0% |

6.5% |

7.4% |

Coutts Balanced Portfolio |

3.1% |

13.2% |

4.2% |

3.6% |

0.7% |

Balanced strategy benchmark |

10.2% |

9.8% |

5.0% |

6.6% |

4.4% |

Coutts Growth Portfolio |

2.8% |

18.3% |

6.5% |

3.9% |

-1.1% |

Growth strategy benchmark |

10.0% |

14.6% |

7.1% |

6.7% |

1.2% |

Past performance should not be taken as a guide to future performance. Market returns shown in sterling terms, total return. Portfolio performance figures are composite returns from the actual portfolios of all clients calculated in sterling, shown on a total return basis and quoted net of all fees. For the composite performance calculation, individual portfolio monthly returns are asset-weighted based on their respective asset values at the beginning of the month. Benchmarks represent a static mix of equities and bonds in proportions relevant to each strategy. Source: Coutts & Co, August 2020.

When investing, past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can go down as well as up, and you may not recover the amount of your original investment.

Share

We’re committed to supporting clients who may be affected by coronavirus and have robust plans in place to minimise any disruption to our service.

ABOUT Coutts INVESTMENTS

With unstinting focus on client objectives and capital preservation, Coutts Investments provide high-touch investment expertise that centres on diversified solutions and a service-led approach to portfolio management. Our investment process is as disciplined as it is creative – ensuring tailored solutions with robust results.

Find Out More About Investing with Coutts