Investing & Performance | 23 June 2025

CIO Update – Markets steady despite Middle East conflict

How the conflict with Iran could impact markets and how we’re assessing the situation alongside client portfolios.

The conflict between Israel and Iran has now been joined by the US, whose military attacked three nuclear sites in Iran. This new development has prompted speculation on how Iran may seek to retaliate or de-escalate through negotiation.

What’s happening in markets?

Market reaction has been relatively benign. The dollar and oil prices did rise though US equity futures were unchanged Monday morning. We do continue to see resilience in the broader data, including in the US economy which is largely energy independent and where we remain overweight in our investment allocations.

Markets are currently ~2% from their all-time highs, driven by solid economic activity, robust earnings growth, and an understanding that the worst-case tariffs fears from April are unlikely to materialise. Last Wednesday the Federal Reserve (Fed) gave a statement underpinning this, saying “recent indicators suggest that economic activity has continued to expand at a solid pace. The unemployment rate remains low, and labour market conditions remain solid”.

Past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can fall as well as rise and you may not get back what you put in. You should continue to hold cash for your short-term needs.

What are we doing?

This is obviously no time for complacency. Mitigating risk in markets means we constantly monitor global events and scenarios as part and parcel of our investment process.

Our Risk team assess a range of what-ifs constantly from systemic risk to market contagion to geopolitical risk. We are currently particularly focused on two possible outcomes, namely a proxy war in the vein of the current conflict versus a direct war, that involves more robust US involvement. This helps us assess how these respective situations, or variables within them, could impact trade and markets and how best we should react to them. We are monitoring these alongside more positive market scenarios such as de-escalation and negotiation.

Active diversification remains central to our multi-asset strategies, helping to reduce the impact of short-term shocks. Bonds have performed well as have our proprietary liquid alternative fund. This fund plays a key role – targeting areas with low sensitivity to traditional equity and bond markets – strengthening portfolio stability in uncertain times.

Our view

Despite the distressing news from the Middle East, from an investment perspective, these are the signals that matter to long-term investors: the estimated risk premia on offer, the state of the underlying macro fundamentals (growth, policy, and inflation) and the expected path of corporate earnings. For now, as the Fed summarised, and our ‘Anchor & Cycle’ framework supports, conditions remain favourable for risk taking.

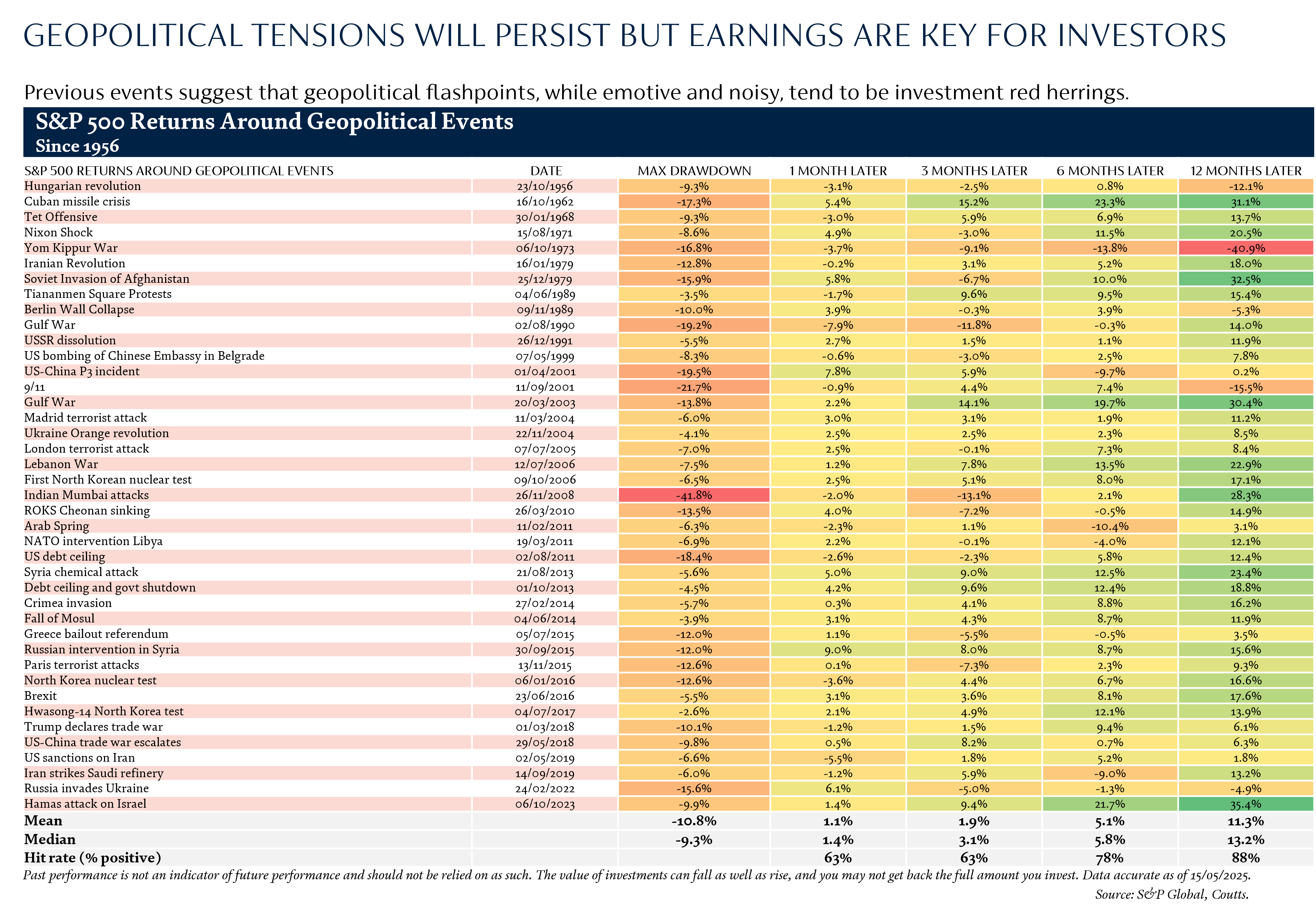

Our base case is for a limited shock which won’t derail markets over the medium to long-term. Looking at the data, we can see that historically, markets quickly get used to uncertain environments and have a strong track record of recovering from similar periods of volatility. Recent price movements may similarly create opportunities for investors. When there is a sudden shock we can see adverse reaction in markets, but they can and do recover, as shown by the below chart. We’ve already seen this happen this year in the months following President Trump’s ‘Liberation Day’ in April as markets made a full recovery.

Geopolitical events can impact markets, usually via oil market volatility and the subsequent impact on inflation. However, our analysis of ~50 geopolitical events since the 1950s shows that market corrections are common, but these events do not on average prevent markets experiencing double digit returns over the subsequent 12 months. It’s also worth reiterating that US equities, to which we remain overweight, tend to be more protected during geopolitical crises, given the US is the world’s largest producer of oil and is positioned as a net exporter of oil.

Going forward, we’re closely monitoring the situation, using real-time data and a disciplined, evidence-based approach. Given the current volatility, we’re holding our position for now, waiting for clearer signals — particularly on valuations — before making any adjustments through our Anchor and Cycle investment strategy.

Speak to us

If you are a Coutts client and would like to discuss market developments or your own investments with us in more detail, please contact your private banker.

Share

More insights

CIO Update – Managing risk amid periods of uncertainty

The future of diversification

Monthly update: Rate Cuts, Resilient Earnings and the Rise of AI: A Market Perspective

When you become a client of Coutts, you'll be part of an exclusive network