SHARE

SHARE

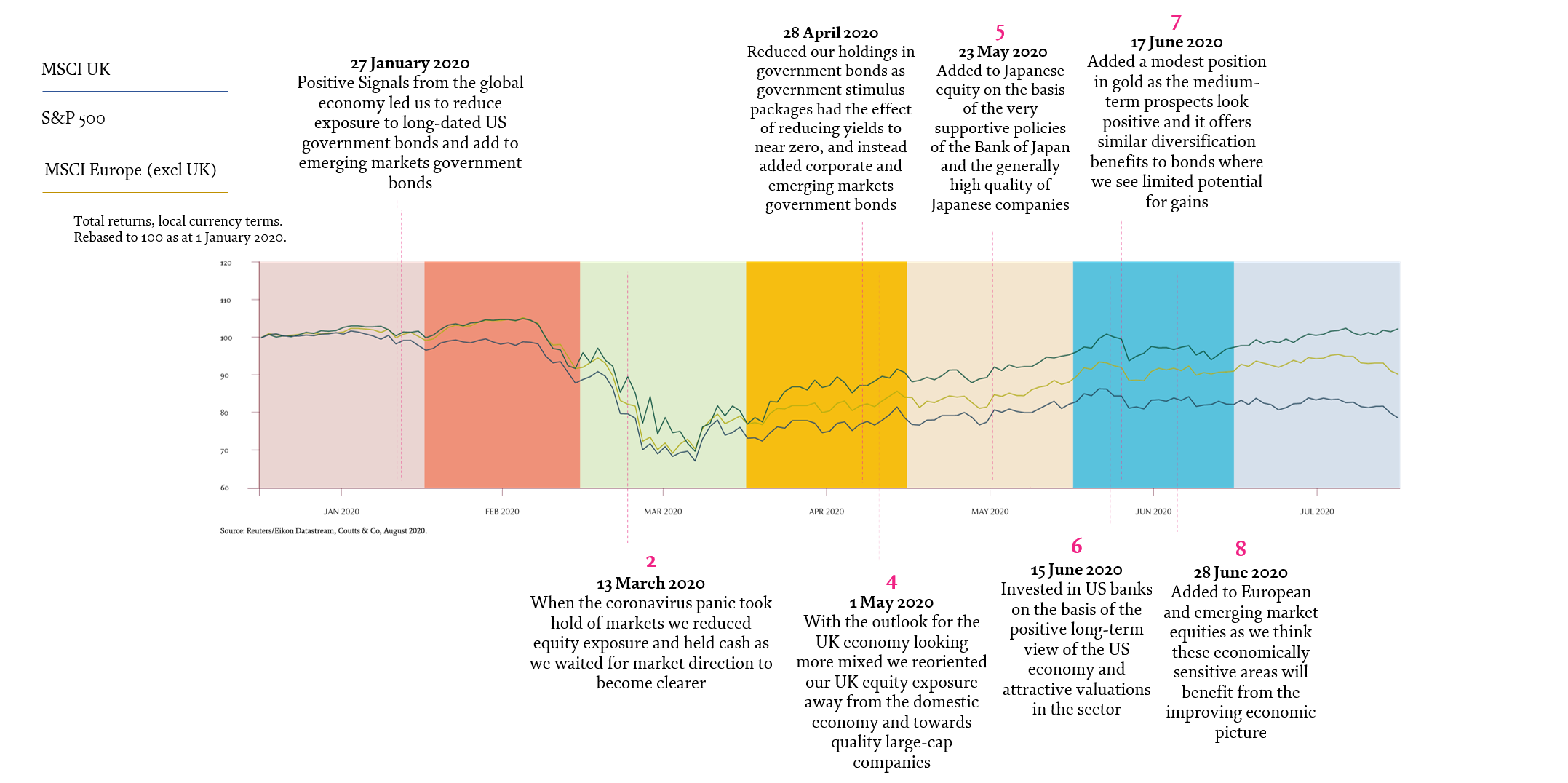

A focus on the future informed by the past

insight and expertise to help you achieve your goals

We keep a sharp eye on the deep trends and tides that power long-term investment returns. Taking this understanding and turning it into decisive investment strategies is just one part of how Coutts helps its clients realise their aspirations.

Asset Allocation Update

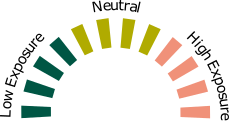

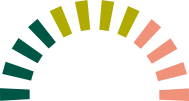

PORTFOLIO POSITIONS AS AT 31 JULY 2020

cash

Cash remains important to provide liquidity and ensure we can act decisively when new investment opportunities arise.

Equity

We are positive over the medium term as unprecedented stimulus from central banks and governments will help companies recover from the COVID-induced recession.

Gold

Gold currently offers attractive diversification benefits, particularly as low real yields are likely to persist given the accommodative stance of central banks. The debt-financed stimulus and geopolitical tensions also support gold.

Government bonds

Expensive valuations and yields close to zero mean return potential and diversification benefits are muted for the time being.

corporate bonds

Central bank support for companies should support corporate debt, and reinforces its relative attractiveness against government bonds at the moment.

Equity

We are positive over the medium term as unprecedented stimulus from central banks and governments will help companies recover from the COVID-induced recession.

Government bonds

Expensive valuations and yields close to zero mean return potential and diversification benefits are muted for the time being.

cash

Cash remains important to provide liquidity and ensure we can act decisively when new investment opportunities arise.

Gold

Gold currently offers attractive diversification benefits it offers, particularly as low real yields are likely to persist given the accommodative stance of central banks. The debt-financed stimulus and geopolitical tensions also support gold.

corporate bonds

Central bank support for companies should support corporate debt, and reinforces its relative attractiveness against government bonds at the moment.

Taking Action

OVER 2020 WE HAVE BEEN ADAPTING OUR INVESTMENTS TO THE RAPIDLY CHANGING CIRCUMSTANCES

Markets fell sharply as the extent of the crisis became clear

PORTFOLIO THEMES

INCREASED BIAS TOWARDS EQUITY

The swift and sizeable response to the COVID-19 pandemic from central banks and governments has supported equity markets through the crisis so far and provides a sound backdrop for the coming months. We’ve increased our exposure in regions and sectors that are mostly likely to benefit as economic momentum takes root and continues to improve.

JAPAN

europe

us banks

EMERGING MARKETS

JAPAN

europe

us banks

EMERGING MARKETS

CORPORATE DEBT OVER GOVERNMENT BONDS

Government bonds offer low yields and little potential for gains in the coming months. Corporate debt meanwhile has higher yields and default risk has been substantially reduced by the scale of support from government and central banks.

Investment grade

financial credit

emerging market debt

Investment grade

financial credit

emerging market debt

GOLD

Provides portfolio diversification and ballast in the event of big market drawdowns and offers protection against the potential for big currency moves due to the build-up of government debt during the pandemic.

RESPONSIBLE INVESTING

Stronger balance sheets, good employment policies and better risk management of highly ESG-rated companies all help to preserve shareholder value during times of economic disruption. Low-carbon tracker funds have reduced exposure to the energy sector, which has suffered from low demand during the lockdown period, and increased exposure to technology, which has benefitted.

sustainable policies

low-carbon funds

sustainable policies

low-carbon funds

Risks in the months ahead

CORONAVIRUS

- If cases continue to rise, new restrictions could result in further market stress.

- Early development of a vaccine could lead to a more vigorous market recovery.

US ELECTIONS

- Likely to be an acrimonious campaign

- Technical issues – such as mail-in voting and the details of Electoral College system – could lead to disputes over the result that would be destabilising for markets.

- Sharp differences between candidates on key issues – for example, corporate tax, healthcare and green agenda – means the result could be meaningful for investors.

BREXIT

.gif)

- Transition ends on 31 December and will likely not be prolonged.

- A comprehensive trade deal is unlikely to happen given the time that remains, but several ‘mini deals’ should minimise disruption and negative economic impact.

- There are implications for sterling and the performance of domestically exposed UK stocks.

US/CHINA TENSIONS

.gif)

- A theme with deep structural drivers that is likely to run for years to come and have profound long-term consequences for the global economic framework.

- Markets have largely been ignoring the risk as the coronavirus has taken centre stage, and so we could see some volatility when it comes back into focus.

- While the rhetoric could get more bellicose in the run up to the US election in November, we don’t think either side has the appetite for strong action that could prove economically disruptive.

Risks in the months ahead

CORONAVIRUS

- If cases continue to rise, new restrictions could result in further market stress.

- Early development of a vaccine could lead to a more vigorous market recovery.

US ELECTIONS

- Likely to be an acrimonious campaign

- Technical issues – such as mail-in voting and the details of Electoral College system – could lead to disputes over the result that would be destabilising for markets.

- Sharp differences between candidates on key issues – for example, corporate tax, healthcare and green agenda – means the result could be meaningful for investors.

BREXIT

- Transition ends on 31 December and will likely not be prolonged.

- A comprehensive trade deal is unlikely to happen given the time that remains, but several ‘mini deals’ should minimise disruption and negative economic impact.

- There are implications for sterling and the performance of domestically exposed UK stocks.

US/CHINA TENSIONS

- A theme with deep structural drivers that is likely to run for years to come and have profound long-term consequences for the global economic framework.

- Markets have largely been ignoring the risk as the coronavirus has taken centre stage, and so we could see some volatility when it comes back into focus.

- While the rhetoric could get more bellicose in the run up to the US election in November, we don’t think either side has the appetite for strong action that could prove economically disruptive.

SHARE

SHARE

Already a client?

For more information about our services, please speak to your adviser or call 020 7957 2424.

Become a client

Please get in touch online or call 020 7753 1365 to find out more about our services.

Calls may be recorded.