SHARE

SHARE

Focus

insight and expertise to help you achieve your goals

We keep a sharp eye on the deep trends and tides that power long-term investment returns. Taking this understanding and turning it into decisive investment strategies is just one part of how Coutts helps its clients realise their aspirations.

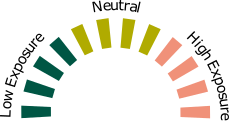

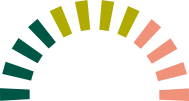

Asset Allocation Update

PORTFOLIO POSITIONS AS AT 31 JULY 2020

cash

Cash remains important to provide liquidity and ensure we can act decisively when new investment opportunities arise.

Equity

We are positive over the medium term as unprecedented stimulus from central banks and governments will help companies recover from the COVID-induced recession.

Gold

Gold currently offers attractive diversification benefits, particularly as low real yields are likely to persist given the accommodative stance of central banks. The debt-financed stimulus and geopolitical tensions also support gold.

Government bonds

Expensive valuations and yields close to zero mean return potential and diversification benefits are muted for the time being.

corporate bonds

Central bank support for companies should support corporate debt, and reinforces its relative attractiveness against government bonds at the moment.

Equity

We are positive over the medium term as unprecedented stimulus from central banks and governments will help companies recover from the COVID-induced recession.

Government bonds

Expensive valuations and yields close to zero mean return potential and diversification benefits are muted for the time being.

cash

Cash remains important to provide liquidity and ensure we can act decisively when new investment opportunities arise.

Gold

Gold currently offers attractive diversification benefits it offers, particularly as low real yields are likely to persist given the accommodative stance of central banks. The debt-financed stimulus and geopolitical tensions also support gold.

corporate bonds

Central bank support for companies should support corporate debt, and reinforces its relative attractiveness against government bonds at the moment.

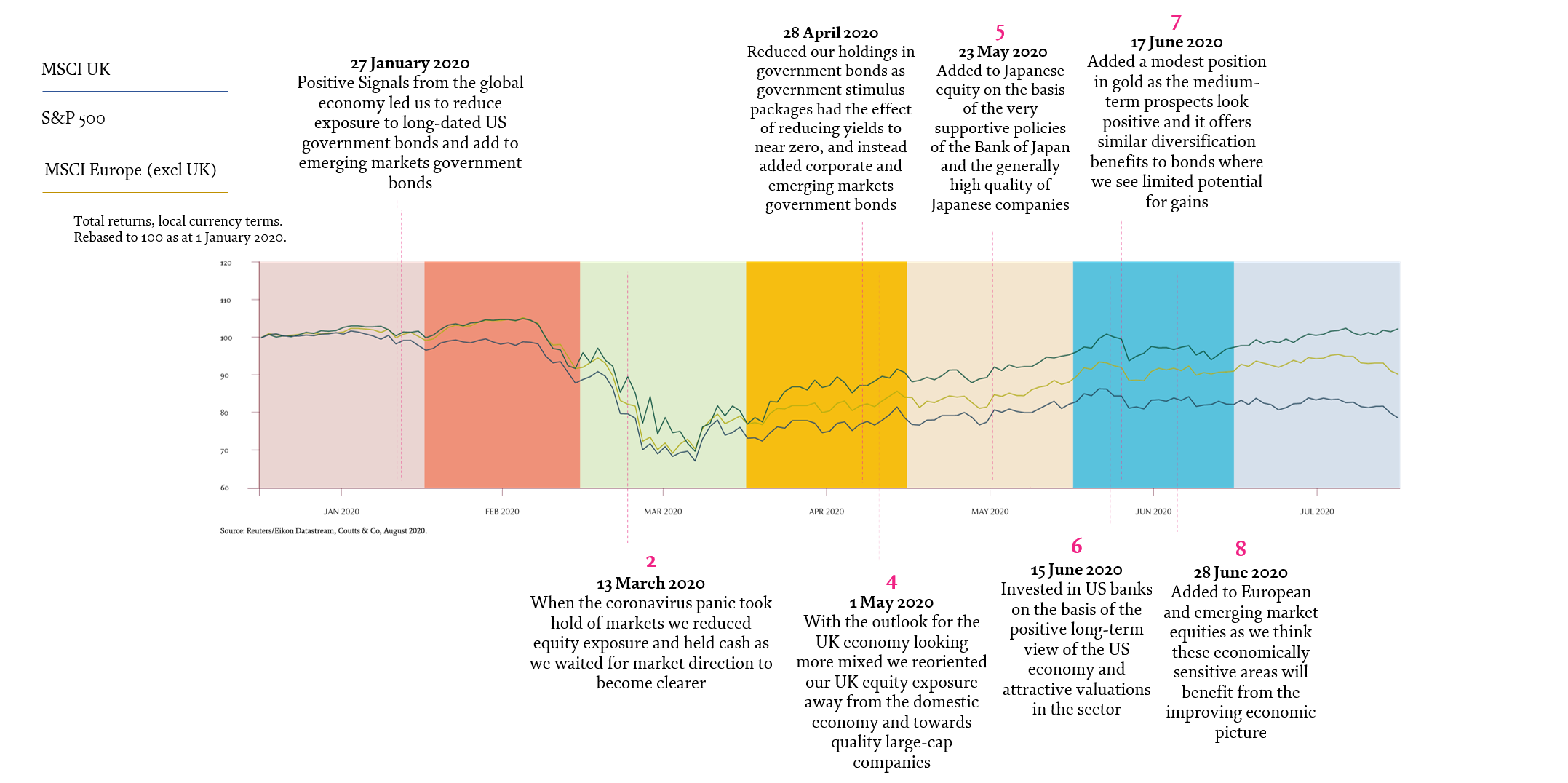

Taking Action

OVER 2020 WE HAVE BEEN ADAPTING OUR INVESTMENTS TO THE RAPIDLY CHANGING CIRCUMSTANCES

Markets fell sharply as the extent of the crisis became clear

PORTFOLIO THEMES

INCREASED BIAS TOWARDS EQUITY

The swift and sizeable response to the COVID-19 pandemic from central banks and governments has supported equity markets through the crisis so far and provides a sound backdrop for the coming months. We’ve increased our exposure in regions and sectors that are mostly likely to benefit as economic momentum takes root and continues to improve.

JAPAN

europe

us banks

EMERGING MARKETS

JAPAN

europe

us banks

EMERGING MARKETS

CORPORATE DEBT OVER GOVERNMENT BONDS

Government bonds offer low yields and little potential for gains in the coming months. Corporate debt meanwhile has higher yields and default risk has been substantially reduced by the scale of support from government and central banks.

Investment grade

financial credit

emerging market debt

Investment grade

financial credit

emerging market debt

GOLD

Provides portfolio diversification and ballast in the event of big market drawdowns and offers protection against the potential for big currency moves due to the build-up of government debt during the pandemic.

RESPONSIBLE INVESTING

Stronger balance sheets, good employment policies and better risk management of highly ESG-rated companies all help to preserve shareholder value during times of economic disruption. Low-carbon tracker funds have reduced exposure to the energy sector, which has suffered from low demand during the lockdown period, and increased exposure to technology, which has benefitted.

sustainable policies

low-carbon funds

sustainable policies

low-carbon funds

Risks in the months ahead

CORONAVIRUS

- If cases continue to rise, new restrictions could result in further market stress.

- Early development of a vaccine could lead to a more vigorous market recovery.

US ELECTIONS

- Likely to be an acrimonious campaign

- Technical issues – such as mail-in voting and the details of Electoral College system – could lead to disputes over the result that would be destabilising for markets.

- Sharp differences between candidates on key issues – for example, corporate tax, healthcare and green agenda – means the result could be meaningful for investors.

BREXIT

.gif)

- Transition ends on 31 December and will likely not be prolonged.

- A comprehensive trade deal is unlikely to happen given the time that remains, but several ‘mini deals’ should minimise disruption and negative economic impact.

- There are implications for sterling and the performance of domestically exposed UK stocks.

US/CHINA TENSIONS

.gif)

- A theme with deep structural drivers that is likely to run for years to come and have profound long-term consequences for the global economic framework.

- Markets have largely been ignoring the risk as the coronavirus has taken centre stage, and so we could see some volatility when it comes back into focus.

- While the rhetoric could get more bellicose in the run up to the US election in November, we don’t think either side has the appetite for strong action that could prove economically disruptive.

Risks in the months ahead

CORONAVIRUS

- If cases continue to rise, new restrictions could result in further market stress.

- Early development of a vaccine could lead to a more vigorous market recovery.

US ELECTIONS

- Likely to be an acrimonious campaign

- Technical issues – such as mail-in voting and the details of Electoral College system – could lead to disputes over the result that would be destabilising for markets.

- Sharp differences between candidates on key issues – for example, corporate tax, healthcare and green agenda – means the result could be meaningful for investors.

BREXIT

- Transition ends on 31 December and will likely not be prolonged.

- A comprehensive trade deal is unlikely to happen given the time that remains, but several ‘mini deals’ should minimise disruption and negative economic impact.

- There are implications for sterling and the performance of domestically exposed UK stocks.

US/CHINA TENSIONS

- A theme with deep structural drivers that is likely to run for years to come and have profound long-term consequences for the global economic framework.

- Markets have largely been ignoring the risk as the coronavirus has taken centre stage, and so we could see some volatility when it comes back into focus.

- While the rhetoric could get more bellicose in the run up to the US election in November, we don’t think either side has the appetite for strong action that could prove economically disruptive.

DANIEL WOOD IS CHIEF OPERATING OFFICER OF THE ASSOCIATION OF UK INTERACTIVE ENTERTAINMENT. HE PROVIDES HIS VIEW ON THE RAPIDLY EXPANDING FIELD OF PROFESSIONAL COMPUTER GAMES PLAYERS, OR ‘ESPORTS’.

What is eSports?

Competitive video games played by professional players.

“It’s grown up with the games industry, alongside the popularity of games themselves. The expansion of broadband in the 2000s and then the arrival of streaming platforms like twitch and youtube that let people share the games have been crucial in the development of the sector.”

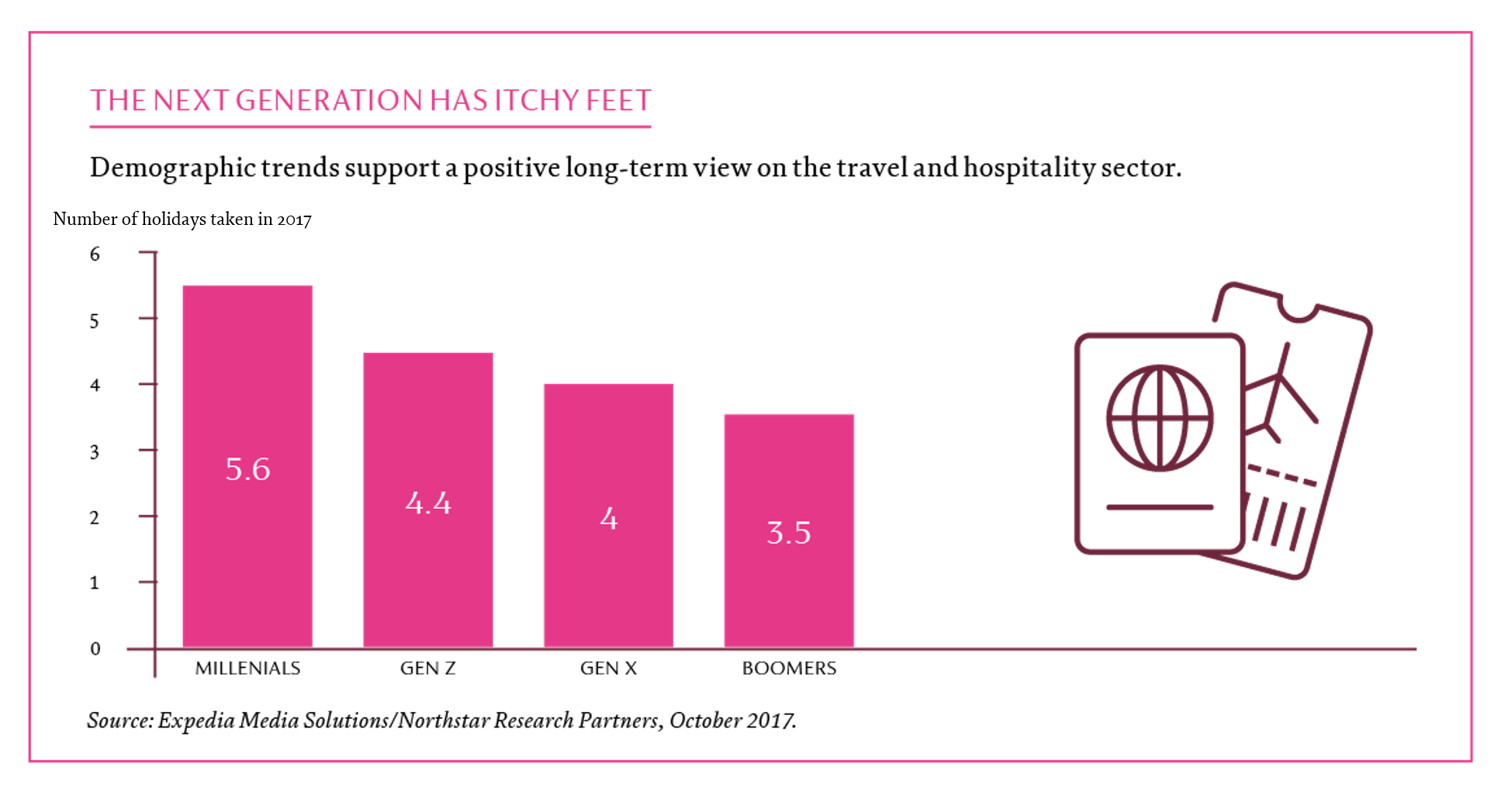

Which are the biggest eSports games?

“In one sense, there’s no such thing as ‘eSports’. Players prefer their own game and there’s not often a lot of cross over between someone who plays and watches, say, FIFA and players of League of Legends. So, when you ask about which games are most important, audiences will tend to name their own game.”

New Olympians?

- Intel World Open eSport championships will be held in Tokyo in partnership with International Olympics Committee ahead of the Olympic Games (the event has been postponed until 2021, alongside the main games)

- In the Paris 2024 Olympics, eSports will be included as demonstration events

“You’re increasingly seeing games designed with eSports in mind. Obviously, they’re great games but publishers are thinking about the eSports sector and how new games might fit in.”

Who watches esports?

“It’s vital to make sure that commercial partners see the importance of the number of eyeballs you can reach through eSports. As an alternative to digital marketing this is a high-quality spend compared to a banner on a website.”

eSports audience growth

Use two fingers to zoom in

“There are live events – like the ESL One in Birmingham – but the big audience is online. There’s a new generation who see it as the norm, and for the next generation digitally native viewers it just fits in to the way they consume media.”

“Lockdown has helped eSports achieve a wider cultural platform and cultural acceptance. The BBC streaming the League of Legends final this year, for example, really helped to promote eSports as a legitimate pastime rather than just a niche.”

What are the commercial

AND INVESTMENT OPPORTUNITIES?

“eSports exist at the cutting edge of digitally delivered entertainment and the landscape is made up of lots of component parts. You have game designers and publishers, players, tournaments hosts, streaming platforms and tech providers all contributing. So, for investors there are many ways to get involved.”

Advertisers include companies like Intel – which has made a big investment in eSports – to more surprising brands like Mercedes or DHL.

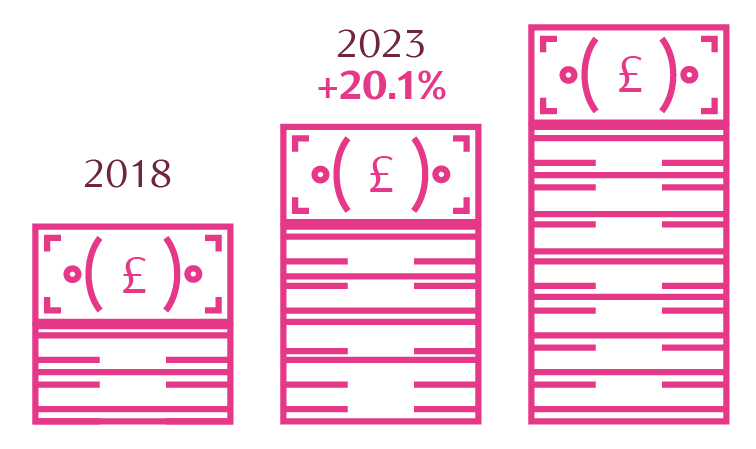

Revenue has grown quickly

20.1% - projected annual revenue growth between 2018 and 2023

Source: PWC Global Entertainment & Media Outlook 2019-2023

“I think broadcast rights will be something to keep an eye on. They’re going to increase in value as the sector grows.”

income sources

Sectors: Travel

WE THINK PREDICTIONS OF DOOM FOR THE TRAVEL AND HOSPITALITY SECTORS ARE PREMATURE.

Travel restrictions have seen the usual tourist destinations abandoned this summer. Meanwhile the cramped conditions of an aeroplane and enclosed environment of a cruise ship present logistical challenges for industries where margins can be tight.

But the urge to see the world and seek new experiences is deeply ingrained. We think that in the longer term people will get back on the road and the travel and hospitality sector is likely to recover.

Use two fingers to zoom in

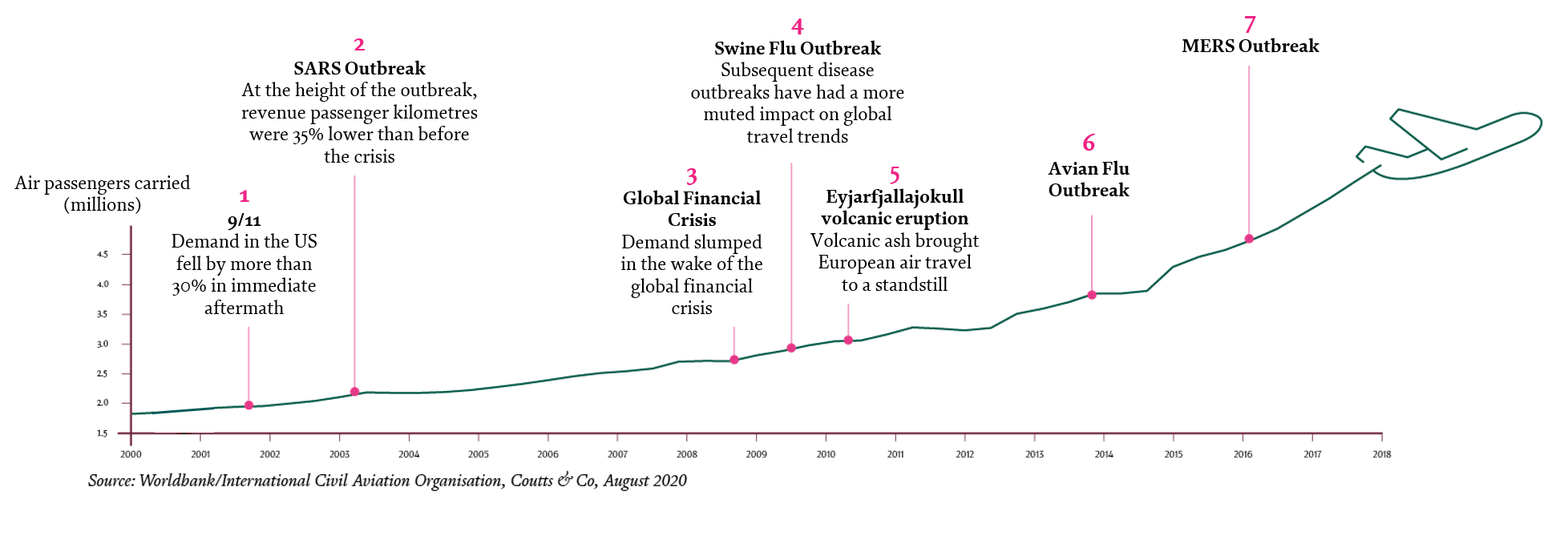

THE ASCENT OF AIR TRAVEL HAS NOT BEEN STOPPED BY PREVIOUS CRISES

The difference in travel between 2019 to 2020. Predictions of the end of the travel sector have come after every global crisis, but the long-term trend shows no sign of slowing.

Use two fingers to zoom in

Cruise liners - 'All aboard'

Cruises were a prime example of a sector hit hard by coronavirus, with high rates of on-board infections and cruises caught in quarantine. And yet:

+40 Percent

2021 bookings were 40% higher in April 2020 than in April 2019, even as cruise ships were stranded by coronavirus lockdowns

Source: cruisecompete.com

May 2020

75 Percent

Percentage of respondents in a poll by cruisecritic.com who said they would be taking either the same amount of cruises or more once the coronavirus crisis subsides

Source: cruisecritic.com

April 2020

Long distance rail - the sleeper wakes

After a decade of closures thanks to competition from short-haul flights, long-distance rail routes are reopening.

paris to nice

French President Emmanuel Macron promised to redevelop night trains in his Bastille Day speech this year, starting with a revival of the overnight service between Paris and Nice.

munich to budapest, zagreb, berlin to moscow

Austrian state rail operator OBB has bought the night train operations of German railway company Deutsche Bahn and is planning to buy 20 trains to service the routes.

prague to rijeka, vienna, warsaw

A new summer service launched by Czech operator RegioJet between the Czech Republic and Croatia has proved so popular it has been upgraded to a daily service. RegioJet now has plans to launch a service travelling through the Czech Republic, Austria and Poland.

stockholm to berlin

Swedish operator Snälltåget is quadrupling the number of night trains on its Stockholm-Malmö-Copenhagen-Hamburg-Berlin route.

LONG DISTANCE RAIL - THE SLEEPER WAKES

After a decade of closures thanks to competition from short-haul flights, long-distance rail routes are reopening.

PARIS TO NICE

French President Emmanuel Macrons promised to redevelop night trains in his Bastille Day speech this year, starting with a revival of the overnight service between Paris and Nice.

MUNICH TO BUDAPEST, ZAGREB, BERLIN TO MOSCOW

Austrian state rail operator OBB has bought the night train operations of German railway company Deutche Bahn and is planning to buy 20 trains to service the routes.

PRAGUE TO RIJEKA, VIENNA, WARSAW

A new summer service launched by Czech operator RegioJet between the Czech Republic and Croatia has proved so popular it has been upgraded to a daily service. RegioJet now has plans to launch a service travelling through the Czech Republic, Austria and Poland.

STOCKHOLM TO BERLIN

Swedish operator Snalltaget is quadrupling the number of night trains on its Stockholm-Malmo-Copenhagen-Hamburg-Berlin route.

MACRO: POLITICS

GET READY FOR MORE GOVERNMENT

Over the decade since the global financial crisis, the ‘old ways’ of monetary policy have been increasingly perceived as ineffective.

This could lay the ground for a shift in popular mood, and policy makers could decide that the time is right for a new economic policy.

MEASURES INTRODUCED TO FIGHT THE COVID-19 PANDEMIC HAVE ACCELERATED THE TREND TOWARDS ‘MORE GOVERNMENT’

FURLOUGH

PROGRAMMES

FISCAL STIMULUS

PACKAGES

REGULATION OF

DIVIDENDS AND

SHARE BUY-BACKS FOR

COMPANIES GETTING GOVERNMENT

ASSISTANCE

CHANGES TO THE TAX

SYSTEM (LIKELY TO SEE

TAXES RISE)

MAY BE AROUND THE

CORNER

FURLOUGH

PROGRAMMES

FISCAL STIMULUS

PACKAGES

REGULATION OF

DIVIDENDS AND

SHARE BUY-BACKS FOR

COMPANIES GETTING GOVERNMENT

ASSISTANCE

CHANGES TO THE TAX

SYSTEM (LIKELY TO SEE

TAXES RISE)

MAY BE AROUND THE

CORNER

THE POLICY SCALE SEEMS TO BE TIPPING TOWARDS MORE GOVERNMENT

GLOBALISATION

Rising global trade, lower trade barriers and regulation, established trading blocks, eg European Union, North American Free Trade Agreement, inclusion of China in the World Trade Organisation

CENTRAL BANK DOMINANCE

Falling interest rates, stimulus measures (qualitative easing), budget and fiscal austerity

FINANCIALISATION

Markets and financial institutions key influencers on policy and economy, financial markets becoming increasingly significant chunk of GDP

OUTCOME

Deflation, falling interest rates, higher asset prices, lower GDP growth

LOCALISATION

Supply chain shifts, Trump’s stance against North American Free Trade Agreement (Nafta), protectionist trade policies, more regulation or companies and people, redistribution a key political motivator.

FISCAL STIMULUS PROMOTE GROWTH

Rising budget deficits, higher public spending and rising public sector weight, radical new ideas eg Modern Monetary Policy, Universal Basic Income

LOCAL INDUSTRY

Governments may require that products or services considered to be of national importance are locally produced

OUTCOME

Potentially higher inflation in the long run, growth in local industry, reduced international co-operation and increasing multi-polarity, higher taxes and regulatory burden

THE POLICY SCALE SEEMS TO BE TIPPING TOWARDS MORE GOVERNMENT

LESS GOVERNMENT

GLOBALISATION

Rising global trade, lower trade barriers and regulation, established trading blocks, eg European Union, North American Free Trade Agreement, inclusion of China in the World Trade Organisation

CENTRAL BANK DOMINANCE

Falling interest rates, stimulus measures (qualitative easing), budget and fiscal austerity

FINANCIALISATION

Markets and financial institutions key influencers on policy and economy, financial markets becoming increasingly significant chunk of GDP

OUTCOME

Deflation, falling interest rates, higher asset prices, lower GDP growth

MORE GOVERNMENT

LOCALISATION

Supply chain shifts, Trump’s stance against North American Free Trade Agreement (Nafta), protectionist trade policies, more regulation

or companies and people, redistribution a key political motivator.

FISCAL STIMULUS TO PROMOTE GROWTH

Rising budget deficits, higher public spending and rising public sector weight,

radical new ideas eg Modern Monetary Policy, Universal Basic Income

LOCAL INDUSTRY

Governments may require that products

or services considered to be of national importance

are locally produced

OUTCOME

Potentially higher inflation in the long run, growth in local industry, reduced

international co-operation and increasing multi-polarity, higher taxes and

regulatory burden.

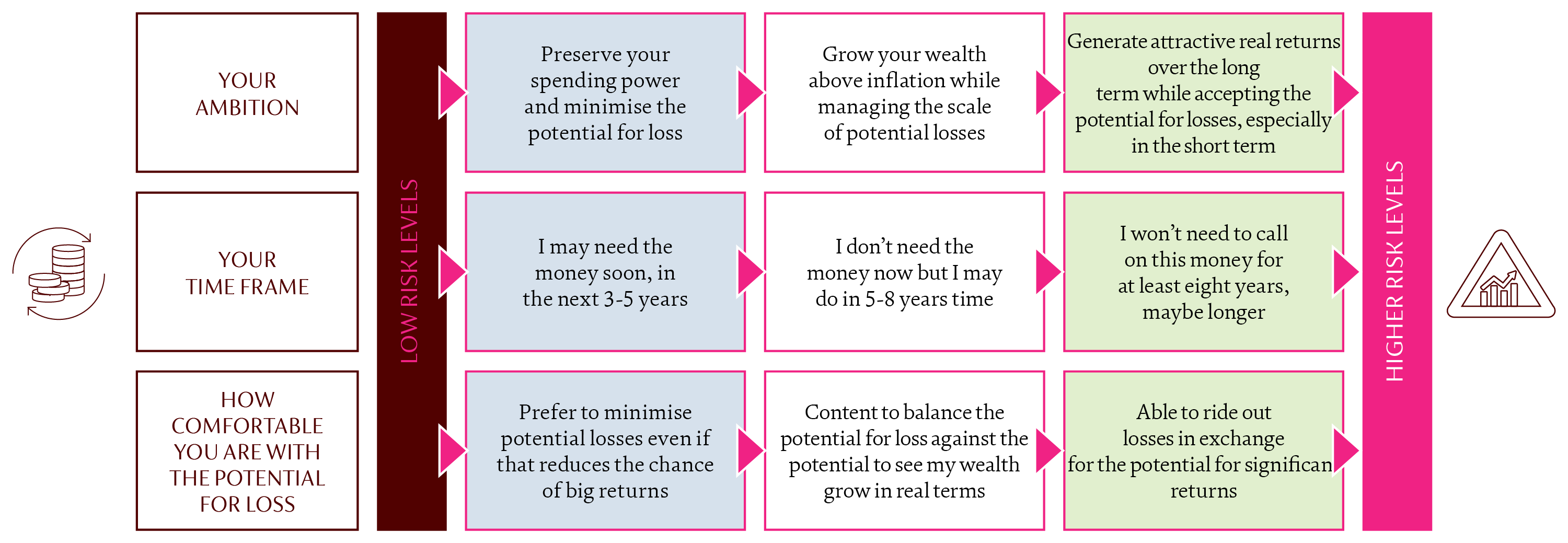

What Investing means to you

1. CHOOSING THE RIGHT INVESTMENT APPROACH FOR YOU

Understanding where you fall on the risk spectrum will help you invest with confidence.

Senior Wealth Manager at Coutts, Hannah Buxton, explains what you should think about as you plan to invest.

Where to start

“Think about what’s really important to you. What do you want to achieve with your investment? Who will be the ultimate beneficiary of it? You? Your family? A cause you care about? Then, think about how much return you’ll need to meet those goals.”

How risk levels can make a difference

“It’s important to remember that all investment comes with an element of risk. But risk is not necessarily a bad thing. It’s an integral part of investing. Balancing your need for a high return with your capacity to cope with the ups and downs of investment markets will help you find your place on the risk spectrum.”

What do you want to do with your money?

Use two fingers to zoom in

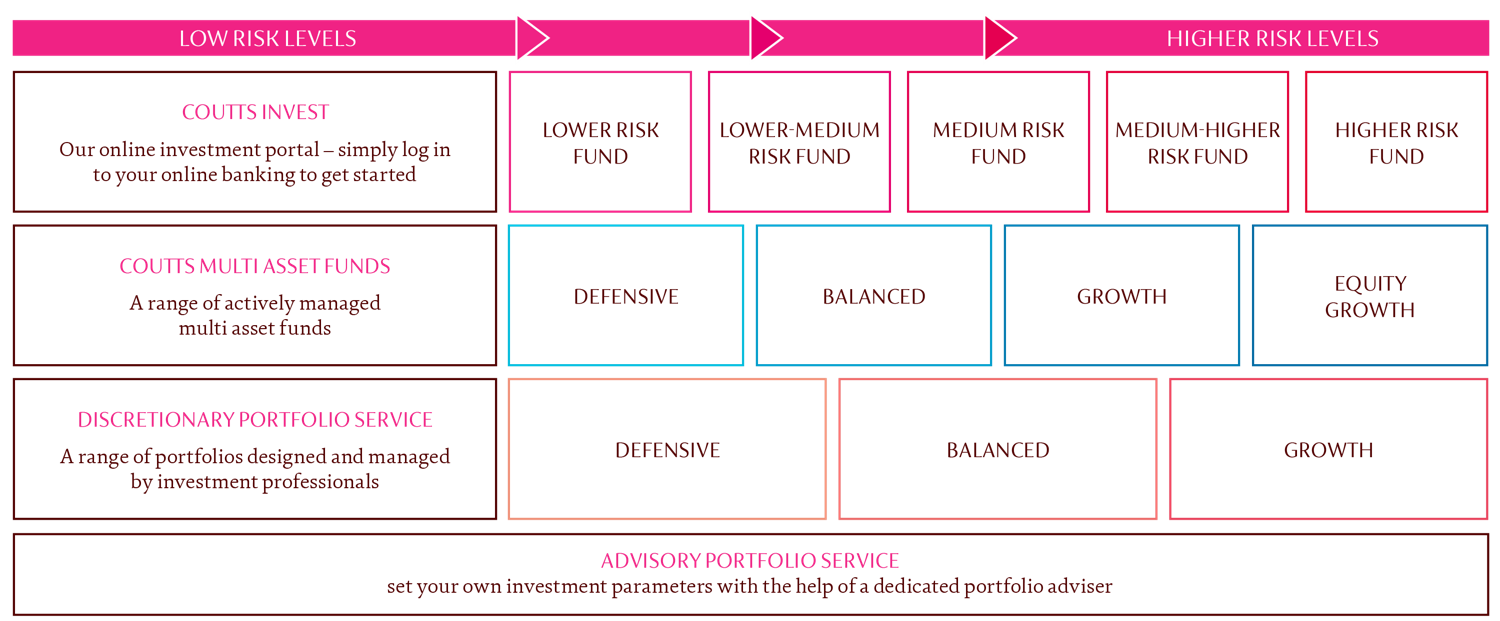

A RISK PROFILE TO SUIT YOUR PREFERENCES

“At Coutts, our portfolios and funds cater for a wide variety of different risk levels, ranging from low-risk defensive strategies to higher-risk strategies that aim to grow your wealth significantly over the long-term. Remember, we’re here to help. If you have a question or want to know more, get in touch with your private banker or wealth manager.”

Use two fingers to zoom in

When investing, past performance should not be taken as a guide to future performance. The value of investments, and the income from them, then go down as well as up, and you may not recover the amount of your original investment.

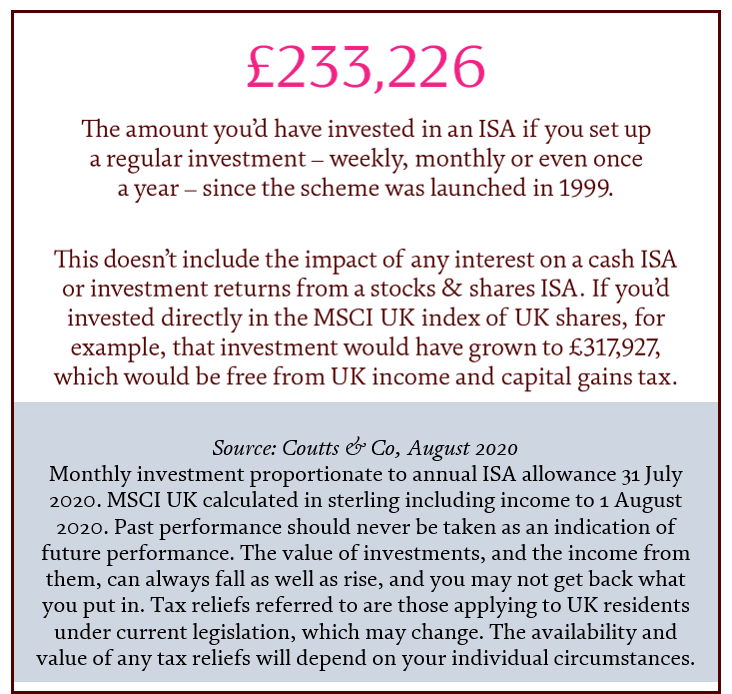

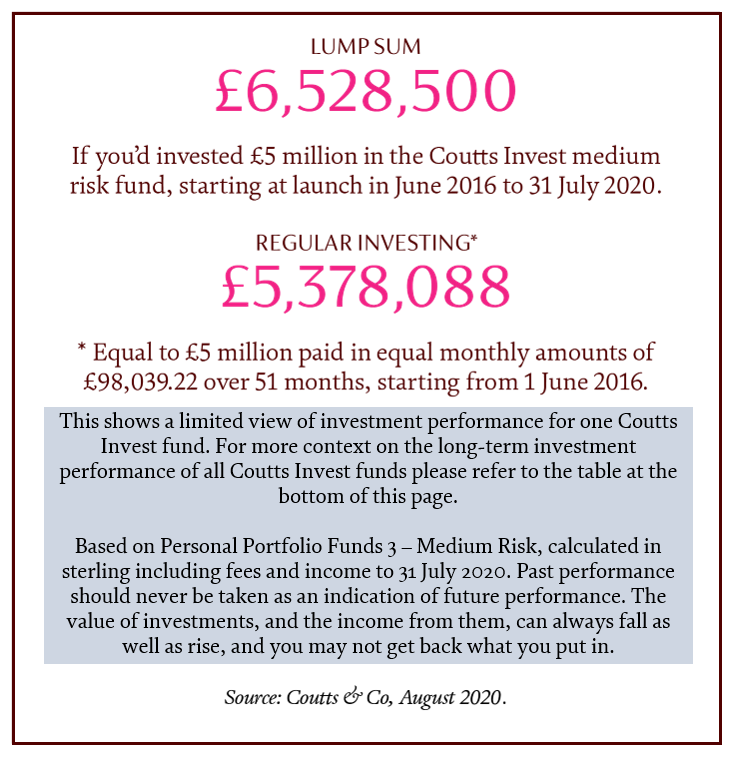

2. REGULAR INVESTING VERSUS INVESTING A LUMP SUM

Why you should regularly invest

>> Regular investing is a good way to build up a substantial portfolio over time

>> Setting up an automated regular payment is a great way to make sure you use your full ISA and pension allowance every year

Why you should consider investing a lump sum

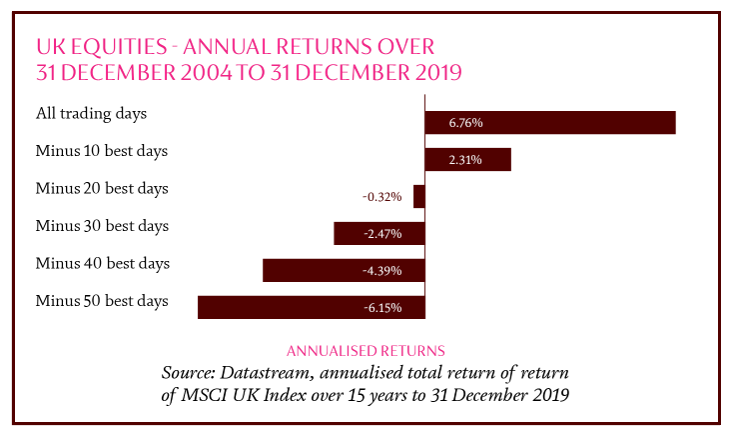

DON’T TRY TO TIME THE MARKETS

Markets can rise and fall unpredictably as investor sentiment changes. In the meantime, missing the best days in the market can materially impact your returns. Holding out for ‘the right time’ could mean you miss out on returns.

Get your money to work early

Lump sums tend to outperform drip-feeding smaller amounts in over time because all your money will benefit from long-term market performance.

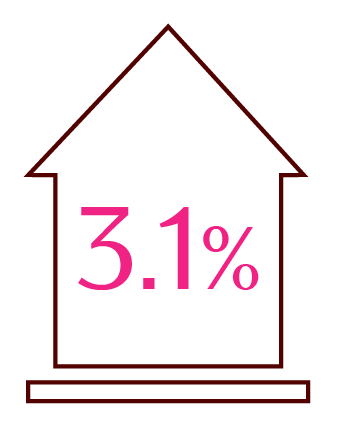

3. INFLATION IS EATING UP THE SPENDING POWER OF YOUR CASH

Inflation is at historic lows right now, but the long-term impact on the spending power of your money can be significant. While there are good reasons to have cash on hand – to meet upcoming expenses, for example, or as a cushion against unexpected bills – holding large amounts of money in low-interest deposit accounts will see its spending power eroded as prices rise.

Use two fingers to zoom in

According to the Bank of England inflation calculator, it would cost £13,510 to buy the same amount of goods and services that you would have been able to get for £10,000 in 2009.

Annual return you would need to maintain the spending power of your cash in the decade 2009 to 2019

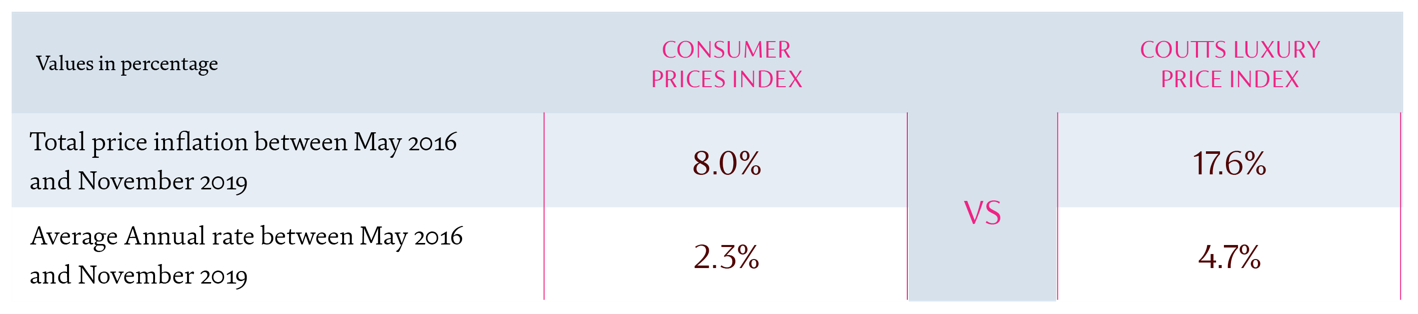

The Coutts Luxury Price Index

How exposed you are to rising prices depends on where you spend your money.

The Coutts Luxury Price Index is based on a basket of goods that reflects the spending patterns of Coutts clients. It provides an alternative view of the impact rising prices could have on your lifestyle.

Luxury prices rise much faster than normal consumer prices

Source: Office for National Statistics, Coutts & Co, August 2020

Use two fingers to zoom in

More information on the Coutts Luxury Price Index

Using our unparalleled insight into the spending habits of our clients, we have constructed the Coutts Luxury Price Index (CLPI) as a unique tool to measure the rate of inflation experienced by UK consumers of luxury goods and services. For example, whereas category ‘3 – Clothing & Footwear’ in the CPI might include jeans and a t-shirt from a high street menswear shop, the CLPI instead tracks the cost of a bespoke suit.

The CLPI is intended as a complement to the CPI. In reality, any individual’s spending will represent a mix of the two rather than be purely one or the other. The CLPI will help you get a more rounded understanding of the impact of inflation on your own spending than looking at the CPI alone.

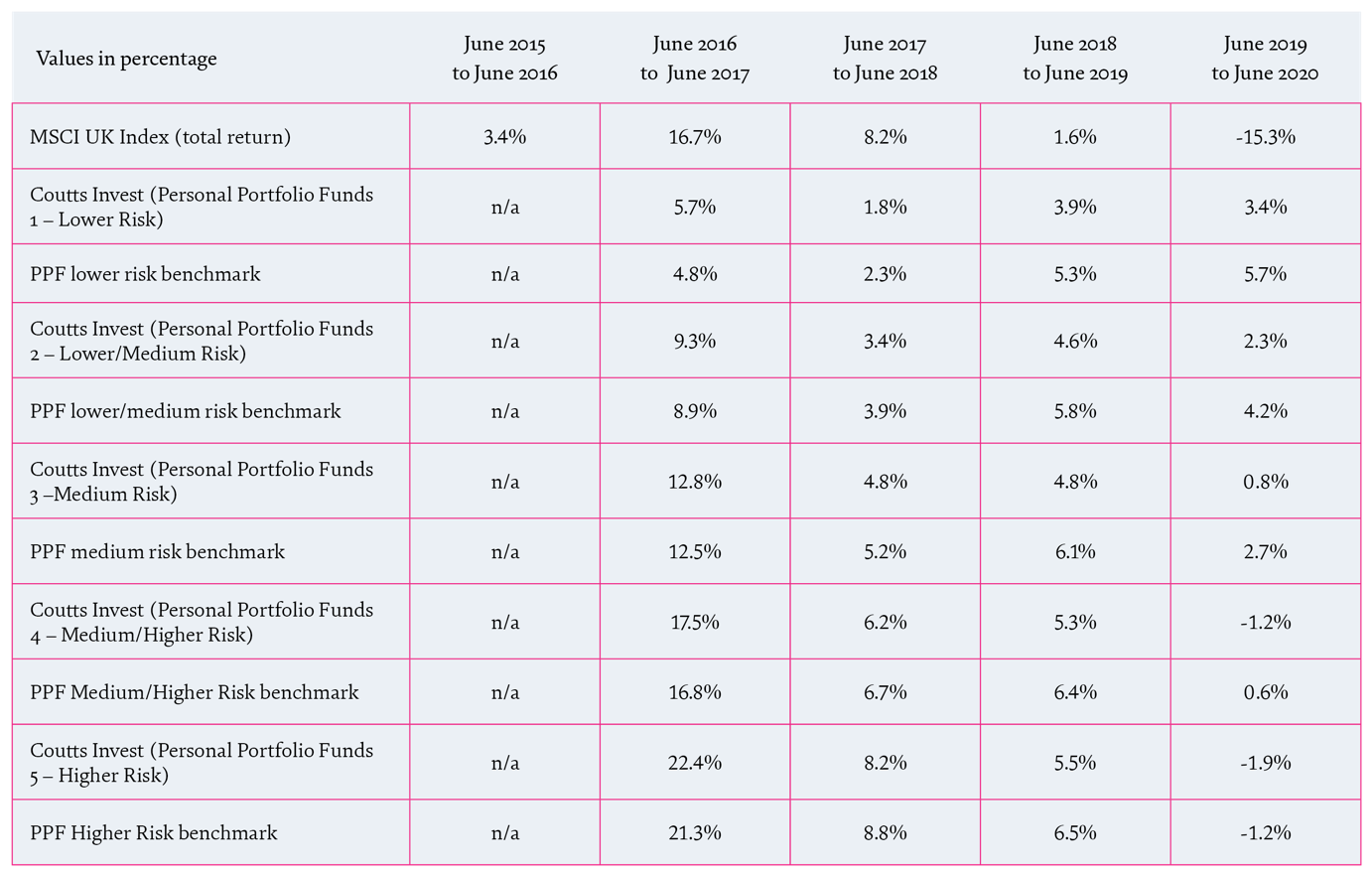

Return data for funds are calculated net of fees, in sterling and assume reinvestment of dividends. Past perfomance should not be taken as a guide to future performance. Benchmarks represent a static mix of equities and bonds in proportions relevant to each strategy.

Source: Thomson Reuters Eikon/Datastream, Coutts & Co, September 2020.

Use two fingers to zoom in

SHARE

SHARE

Already a client?

For more information about our services, please speak to your adviser or call 020 7957 2424.

Become a client

Please get in touch online or call 020 7753 1365 to find out more about our services.

Calls may be recorded.