Investing

Mid-year Investment Outlook 2023: our macroeconomic outlook

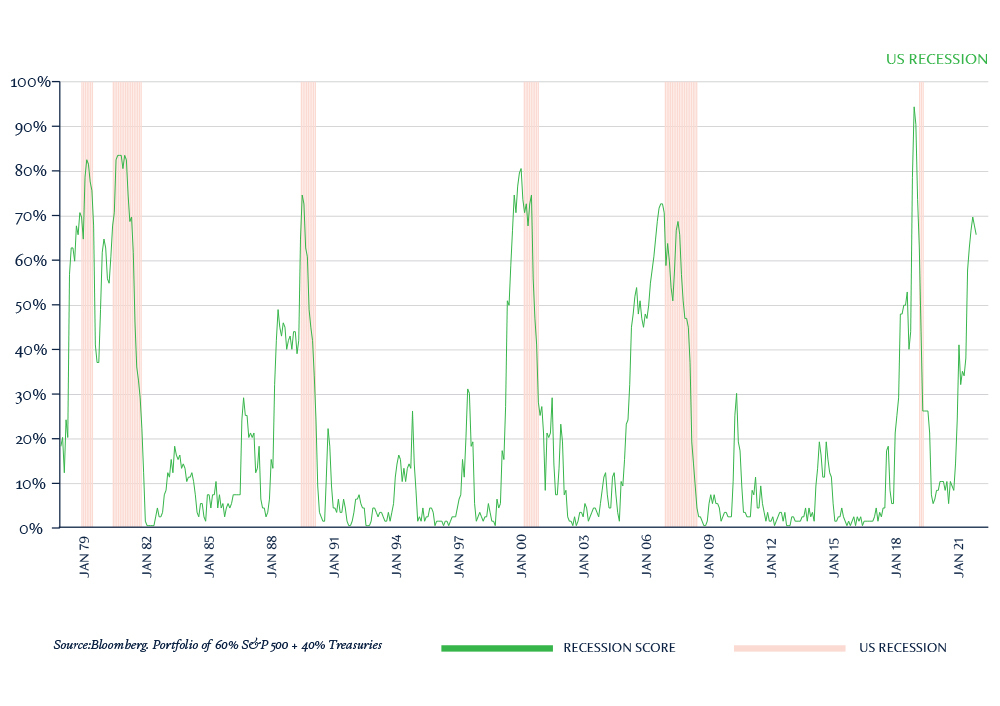

Time for caution

It’s easy to argue both the positive and negative narratives for the economy and equity markets. But if we look deeper, it seems that the likelihood of a US recession is still the main story of 2023. Let’s start with the weight of the macroeconomic evidence and why it still seems appropriate to steer a more cautious course in the coming months.