Investing & Performance | 27 May 2025

CIO Update – Reducing our equity exposure

We’ve reduced our overweight position in equities in light of recent tariff policy headwinds – but we still have a positive outlook on earnings and the business cycle.

Since October 2023, we’ve had an overweight allocation to global equities as our investment process signalled a positive outlook on the business cycle. Solid corporate earnings expectations encouraged us to be more bullish in our strategy which has been a significant driver in our portfolio performance.

Now that this backdrop is shifting off the back of the evolving trade and political landscape, we’ve decided to reduce our global equity allocation within portfolios, notably to the US and Japan.

The tariff policies introduced by the US in April have resulted in elevated risks that mean we now have a lower conviction level than we did previously. Uncertainty surrounding economic growth and inflation will limit central banks’ ability to continue reducing interest rates quite so freely without having some form of impact on either the economy or rising prices.

With that said, the business cycle and earnings outlook remain positive, supporting our view to maintain an overweight position in global equities, with lower conviction than the start of the year.

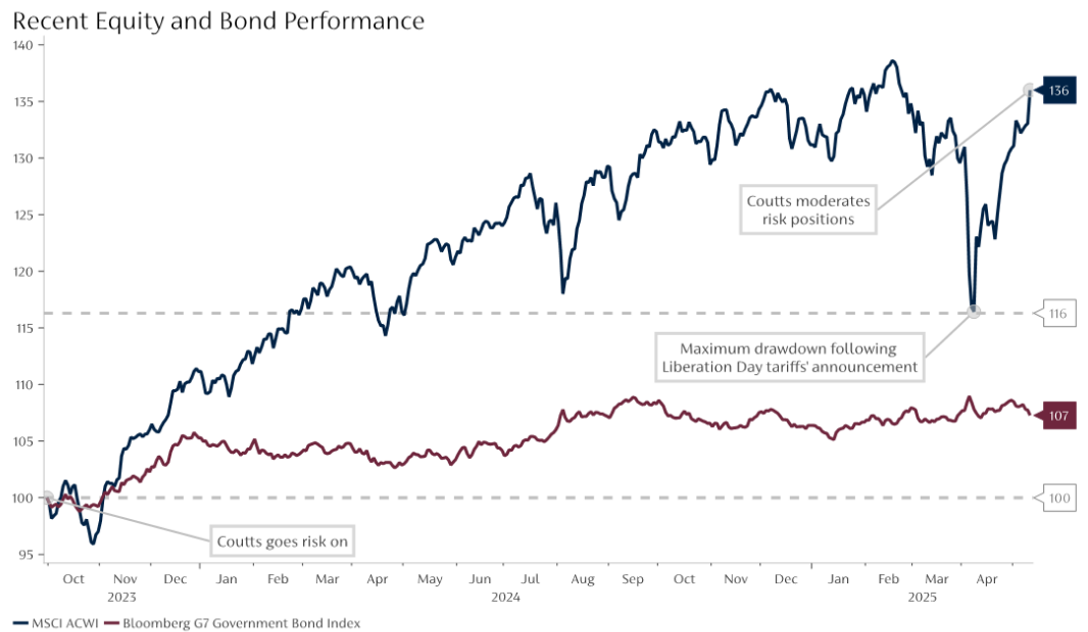

Trusting the process

Source: S&P Global, Macrobond, Coutts. As at 16 May 2025

Past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can fall as well as rise and you may not get back what you put in. You should continue to hold cash for your short-term needs.

As detailed in the graph above, the MSCI All Country World Index (ACWI) has been on an upward trajectory since we made the decision to go risk-on back in 2023. While there was a significant drawdown following ‘Liberation Day’, our process guided us to be patient and stick with our existing strategy.

We identified a significant divergence between the ‘hard’ data (backward-looking prints) and ‘soft’ data (forward-looking surveys) suggesting that the market declines were an event shock rather than the start of a cyclical downtrend. Riding out this volatility meant our portfolios captured some of this recovery before we decided to moderate our risk exposure.

Japanese stocks out, Japanese bonds in

Replacing this equity exposure, we have invested more in Japanese government bonds (JGBs), closing our underweight position.

JGB yields are at a 15-year high, having risen sharply over the past 12 months from around 0.9% to 1.3%. This means the prospects for future returns from JGBs have improved as any future decline in yields would mean prices rise.

The investment team and I are constantly reviewing the developing situation with regards to global trade and the knock-on effect this could have on the global economy. We are in the fortunate position to be nimble and reactive as and when greater clarity comes or if the situation intensifies. We can and will adjust our portfolios should our process guide us to do so.

Speak to us

If you are a Coutts client and would like to discuss market developments or your own investments with us in more detail, please contact your private banker.

Share

More insights

CIO Update – Managing risk amid periods of uncertainty

The future of diversification

Monthly update: Rate Cuts, Resilient Earnings and the Rise of AI: A Market Perspective

When you become a client of Coutts, you'll be part of an exclusive network