Rising inflation – what could it mean for your investments?

The prospect of rising inflation ruffled feathers in February, but your investments with Coutts are well positioned to cope.

3 min read

SHARE

Most Popular

-

Ukraine invasion: Keeping our clients informed | Coutts

15 Mar 20221 min

-

Coutts and charitable giving in the Covid era

02 Dec 20214 min

Become A Client

When you become a client of Coutts, you will be part of an exclusive network.

As vaccine programmes continue to make progress across the world, there’s a rising sense of optimism about the year ahead. As well as the prospect for a summer holiday and a drink with friends, the global economic recovery is gathering pace.

The first quarter earnings season has been much better than expected, which indicates that the economy is expanding. Notably, the tech giants reported strong earnings – Apple’s revenue reached $111.4 billion in its best quarter ever. Resilient numbers from companies more sensitive to economic growth reinforced the view of improving confidence.

But the prospect of recovery brings higher inflation expectations, which had an impact on markets in February. The most striking thing was the impact on bonds, where prices fell sharply – for example, the 10-Year US Treasury bonds returned -2.7%. The MSCI World Index of global equities fell -0.8% as inflation concerns made their way through equity markets. (Local currency terms, income included, source Reuters Eikon/Datastream.)

Careful management helps navigate market volatility

We’ve positioned your investments for higher inflation expectations. Inflation tends to boost profits in cyclical sectors, and so allocations we made last year to banks, emerging markets and Japan have performed well, as did our more recent shifts within UK equity. We have a low allocation to bonds, which don’t perform so well under these conditions.

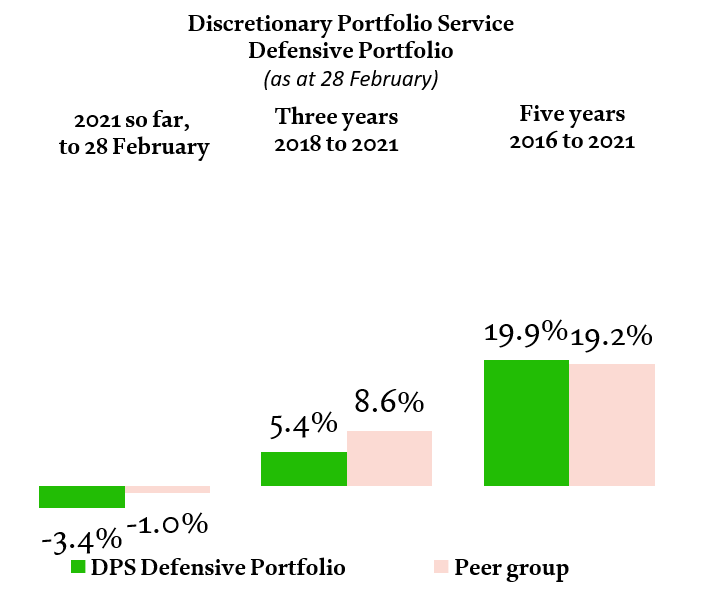

The impact of bond market falls was noticeable in defensive portfolios and funds, which have more bonds than other strategies.

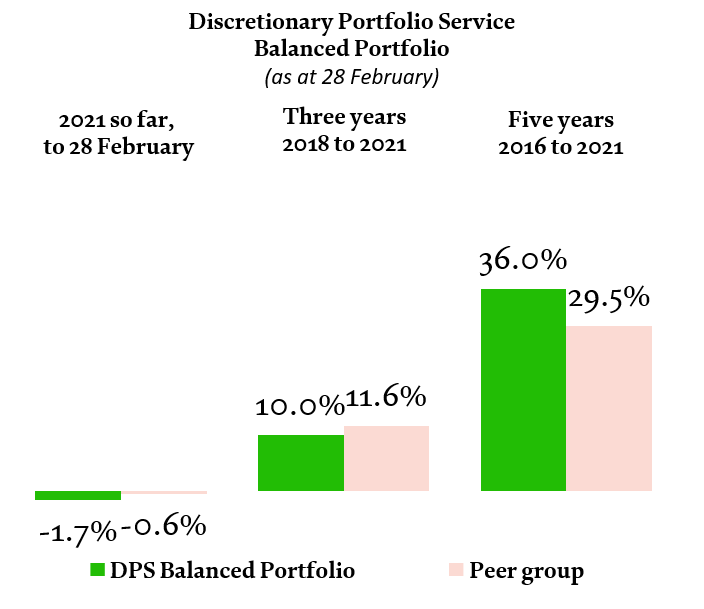

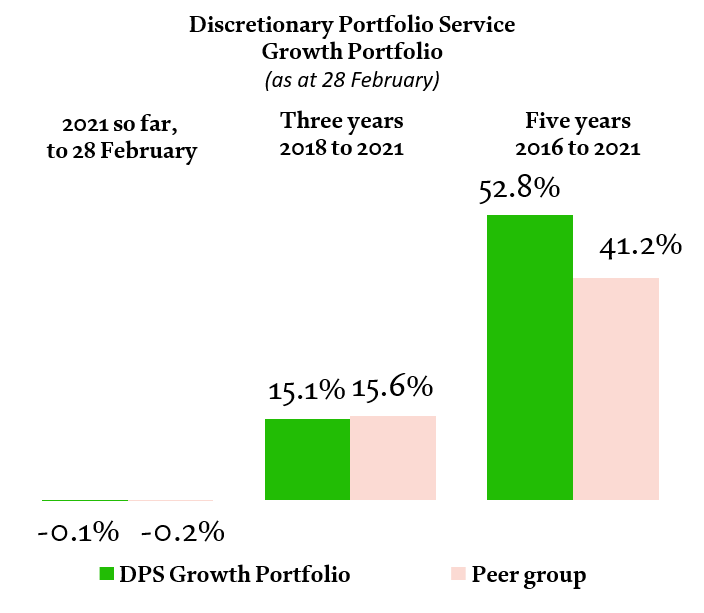

Cumulative returns calculated on sterling basis, including fees, charges and income to 28 February 2021. These data are based on composite performance, individual portfolio monthly returns are asset-weighted based on their respective asset values at the beginning of the month. Peer group returns provided by Asset Risk Consultants (ARC); end-February data represents ARC estimate. Past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can go down as well as up and you may not recover the amount of your original investment. Sources: Coutts & Co, ARC. March 2021.

WHAT IS REFLATION?

With the economic recovery continuing, we see ‘reflation’ as one of the key investment themes for the months ahead.

When the economy suffers a recession or period of uncertainty, it can cause deflation, where the prices of goods and services fall. This can be very bad for the economy, and so policymakers act to stimulate growth through reflationary measures – such as government spending and central bank quantitative easing.

This is what we’ve seen since April last year, and the signs suggest that it’s been largely successful. Economic activity is restarting and inflation is likely to rise from its current, very low levels – annual price inflation is 0.7% in the UK and 0.3% in the US, according to the latest data, against the 2% targeted by both the Bank of England and US Federal Reserve.

Looking ahead, the $1.9 trillion US stimulus package, passed in the first week of March, will provide a vital boost to the country’s economy. Combined with previous stimulus, this historic level of economic support is likely to spur the economy to one of its best years of growth since World War 2. Coronavirus cases should continue to fall as the temperature rises and more people receive the vaccine, which should further stimulate economic activity.

These are all likely to increase inflationary pressure on the global economy.

“We’ve positioned your investments for higher inflation expectations.”

WHAT DOES THIS MEAN FOR YOUR INVESTMENTS?

On the one hand, investors are concerned that higher inflation will reduce the real value of future returns across several types of assets. On the other, they worry that inflation may start rising quickly, leading policymakers to take a sudden change in direction that could leave businesses wrong-footed.

While we don’t expect a sudden change in monetary policy, it’s likely that inflation will rise. In this environment, businesses that are more sensitive to the economy such as industrials and energy companies – known as ‘cyclical stocks’ – tend to perform well. Their products are typically in demand as companies invest and grow, increasing profits.

Growth stocks, such as technology companies, tend to be less popular. Their valuations reflect potentially higher cashflows in the future, which become less attractive in the face of higher inflation. Bond prices also fall (often expressed in terms of a rising yield) as investors price-in the impact of higher inflation on returns.

With the sharp rise in inflation expectations in February, and the subsequent impact on bonds, a lot of these impacts could now be priced-in. We made some tactical changes at the start of March that take into account rapid market moves and evolving market conditions to make sure we’re well-positioned.

long-term returns

31 December 2015 to 31 December 2016 |

31 December 2016 to 31 December 2017 |

31 December 2017 to 31 December 2018 |

31 December 2018 to 31 December 2019 |

31 December 2019 to 31 December 2020 |

|

MSCI World Index (sterling) |

28.2% |

11.8% |

-3.0% |

22.7% |

12.3% |

Coutts Defensive Portfolio |

8.4% |

5.8% |

-3.7% |

8.3% |

3.5% |

Defensive strategy benchmark |

12.8% |

5.7% |

-1.6% |

11.1% |

7.7% |

Coutts Balanced Portfolio |

12.2% |

9.1% |

-5.1% |

12.4% |

4.4% |

Balanced strategy benchmark |

17.6% |

7.9% |

-2.9% |

14.1% |

6.5% |

Coutts Growth Portfolio |

16.2% |

12.1% |

-6.5% |

16.9% |

4.7% |

Growth strategy benchmark |

21.8% |

10.4% |

-4.2% |

17.0% |

4.9% |

Returns calculated on sterling basis, including fees, charges and income. Benchmarks represent a static mix of equities and bonds in proportions relevant to each strategy. Source: Reuters Eikon/Datastream, Coutts & Co, March 2021.

Past performance should not be taken as a guide to future returns. The value of your investments, and the income you get from them, can go down as well as up and you may not get back the amount you first invested.

Share