Investing & Performance | 6 August 2025

CIO Update – The land of rising earnings

How corporate reforms and trade agreements are supporting a positive narrative for Japanese equities.

Fahad Kamal, Chief Investment Officer

Nobel Prize-winning economist Simon Kuznets once remarked, “There are four categories of countries: developed, under-developed, Argentina and Japan.” Japan remains a uniquely positioned economy—one that is once again drawing investor attention.

Following decades of stagnation, there are signs that the Japanese economy is emerging from this into a more robust nominal growth backdrop. Combined with corporate governance reforms and the successful conclusion of trade talks with the US recently, the outlook for Japanese equities looks compelling.

A renewed focus on shareholders

Historically, Japanese companies have been criticised for inefficient management and a limited focus on shareholder returns. Many operated across diverse, unrelated sectors, diluting strategic focus. However, reforms introduced by the Tokyo Stock Exchange have begun to shift this dynamic.

Companies are now placing greater emphasis on capital efficiency and shareholder value. Share buybacks in 2024 were approximately 70% higher than in 2023, and there have been a number of high-profile spin-offs and divestments —clear signs of progress.

Past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can fall as well as rise and you may not get back what you put in. You should continue to hold cash for your short-term needs.

Our view

For large parts of the last fifteen years, investors have not been rewarded for diversifying portfolios, as equity market leadership was unusually narrow. Going forward, we think the value of diversification could increase, given shifting macroeconomic dynamics and policy volatility globally.

In December 2024, we diversified our overweight equity allocation by adding Japanese equities alongside our US exposure, and this has supported our performance.

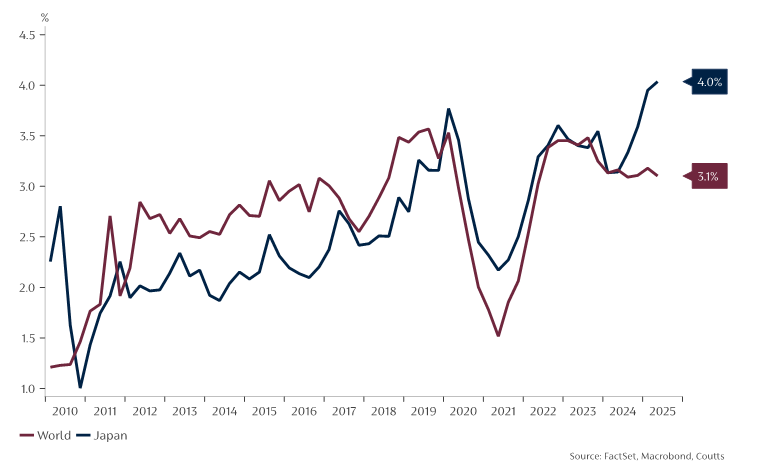

Improved Shareholder Governance is Boosting Japanese Returns

Shareholder yield (buybacks plus dividends)

Data accurate as of 09/07/2025.

Japanese corporate earnings continue to grow, and Japanese companies’ increasing focus on returning capital to shareholders is a positive development for investors. Share buybacks contribute to total shareholder returns, as the chart above shows, and enhance earnings per share for remaining shareholders— an important driver of long-term value.

However, the political backdrop in Japan remains uncertain.

In 2024, Japan’s ruling Liberal Democratic Party (LDP) lost its majority in the lower house, and last month lost in the upper house. This uncertainty may cause volatility moving forward, but ultimately Prime Minister Ishiba will look to maintain power, likely via increased fiscal stimulus. And although this could increase pressure on Japanese government bond markets, it could prove a tailwind for the economy and equity market earnings.

Speak to us

If you are a Coutts client and would like to discuss market developments or your own investments with us in more detail, please contact your private banker.

Share

More insights

CIO Update – Managing risk amid periods of uncertainty

The future of diversification

Monthly update: Rate Cuts, Resilient Earnings and the Rise of AI: A Market Perspective

When you become a client of Coutts, you'll be part of an exclusive network