Markets show resilience and overcome “wall of worry”

Stock markets recorded impressive highs in October following several unsettled weeks.

3 min read

SHARE

Most Popular

-

Ukraine invasion: Keeping our clients informed | Coutts

15 Mar 20221 min

-

Coutts and charitable giving in the Covid era

02 Dec 20214 min

Become A Client

When you become a client of Coutts, you will be part of an exclusive network.

Global markets shrugged off the many challenges they’d been facing and bounced back last month, with some stock indices breaking records.

Supply shortages, soaring energy prices and an inflation spike were among the issues making investors nervous in September and early October. None of those issues escalated, however, and markets responded positively.

Bond markets have had a turbulent time in the face of rising inflation and higher interest rate expectations. But even they settled towards the end of the month as markets adapted, with UK government bonds even seeing a sharp uptick following supportive announcements in the government’s Autumn Budget.

Sven Balzer, Head of Investment Strategy at Coutts, said: “Markets very much overcame a wall of worry and rebounded in October, delivering good returns across most regions. The Chinese market stabilised, the US performed strongly and the UK showed just how resilient it can be – its performance bolstered by rising energy stocks.”

Looking ahead, Sven thinks the supply chain disruptions which have plagued markets will sort themselves out, but it’ll take time.

“Patience is required,” he said. “The global economy is adjusting from extreme swings to a new equilibrium. But many of the bottlenecks should start to get back to normal over the course of next year.”

The MSCI World Index of global equities returned 5.5% in October (local currency terms), while US 10-year Treasury bonds stayed flat, returning -0.1%.

Stock markets scale new heights

In early October the FTSE 100 had its best first week of the month since May, helping it to a 20-month high and a recovery of most of its losses since February 2020. Meanwhile, the S&P 500 reached a record high in October, helped by strong earnings announcements from companies.

Despite the strong month, many UK active fund managers had a difficult time as they tend to hold fewer energy or bank stocks than the FTSE 100 – stocks which did well – and more small or medium sized businesses, which underperformed. This year’s oil price rise of 80% to the end of September drove energy returns, while banks were buoyed by rising interest rate expectations.

Meanwhile, the performance turnaround of UK government bonds, or gilts, came about after two key announcements in Chancellor Rishi Sunak’s Budget. The Office for Budget Responsibility revised its forecast for UK economic growth in 2021 up to 6.5% from 4%, which implies less government borrowing will be needed. The Debt Management Office consequently adjusted its plans and said it would issue fewer UK government bonds, which had a positive impact on gilt prices.

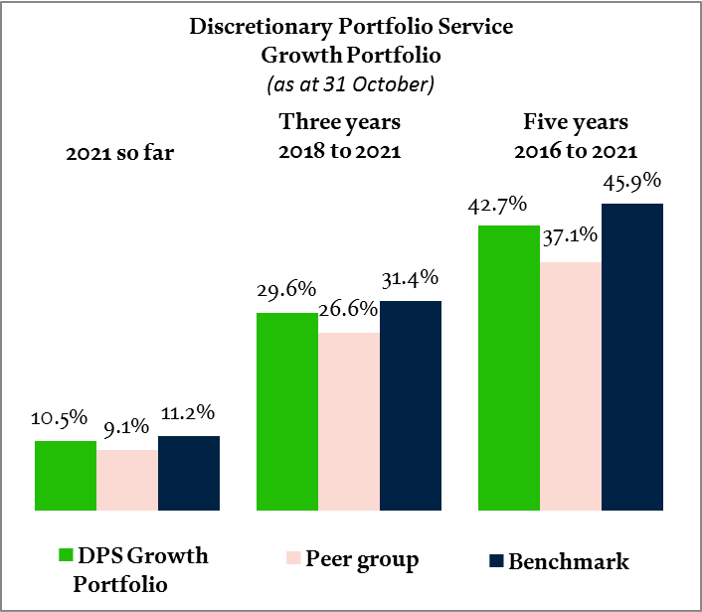

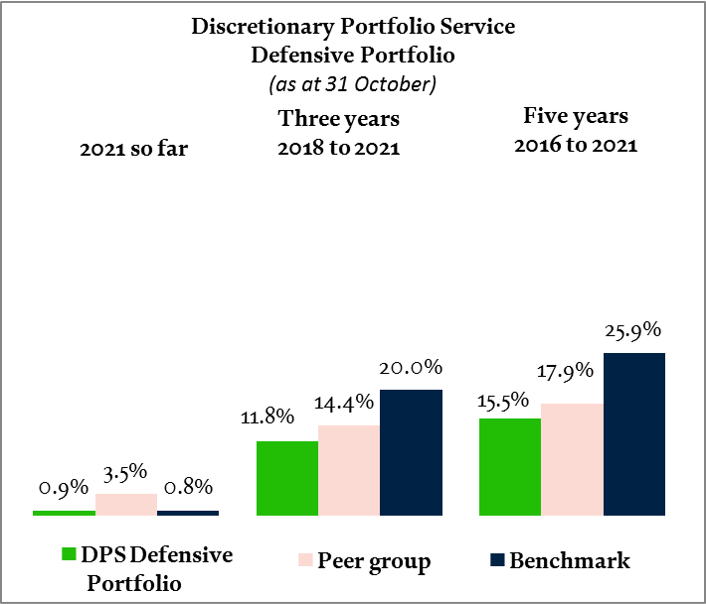

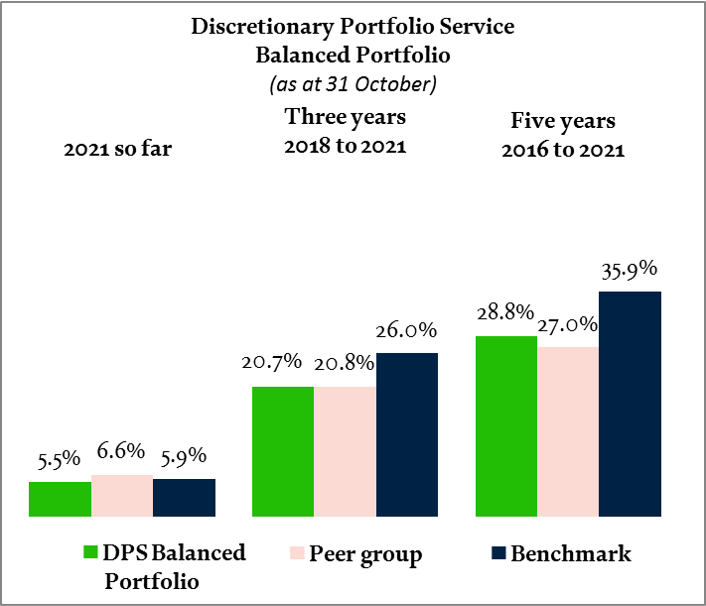

Peer-beating performance

Our clients’ growth portfolios delivered returns ahead of the competition so far this year, and over the last three and five years. Balanced portfolios are broadly in line with competitors over the same timeframes, while defensive mandates remain flat so far this year, largely because of bond market performance.

The portfolio performance shown below is net, so has fees and charges deducted, while the benchmark performance is gross with no such deductions.

Cumulative returns calculated on sterling basis, including fees, charges and income to 31 October 2021. These data are based on composite performance, individual portfolio monthly returns are asset-weighted based on their respective asset values at the beginning of the month. Peer group returns provided by Asset Risk Consultants (ARC); end-October data represents ARC estimate. Benchmarks represent a static mix of equities and bonds in proportions relevant to each strategy. Past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can go down as well as up and you may not recover the amount of your original investment. Sources: Coutts & Co, ARC. November 2021.

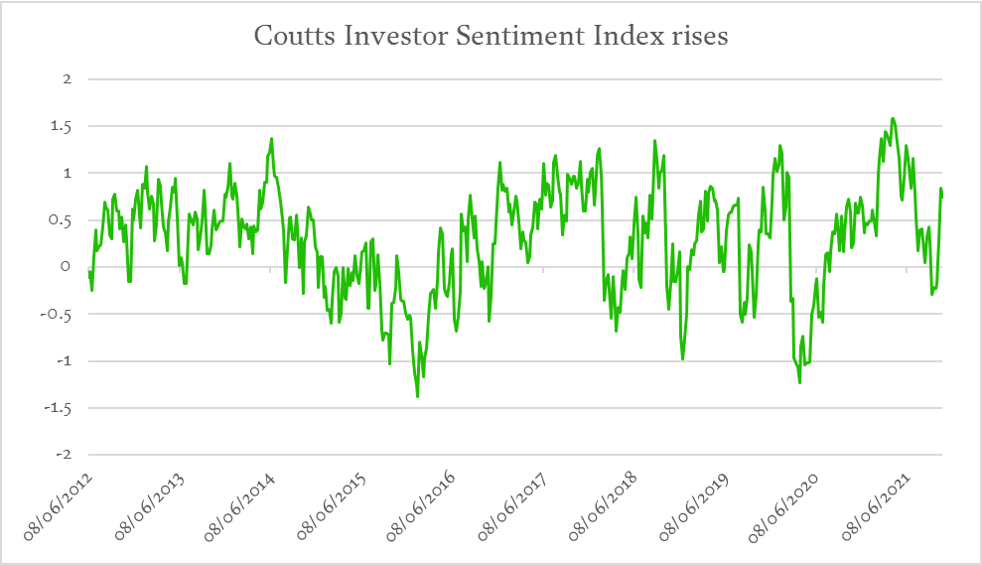

The more buoyant market mood is reflected in the Coutts Investor Sentiment Index. The index rose in October to 0.74. Readings over 1 show investor complacency, readings below -1 show anxiety. Our index brings together various key market measures looking at volatility and investor positioning.

Higher inflation still on cards but

central banks stay supportive

Inflation expectations have risen in the US, UK and Europe, which initially pushed up government bond yields (pushing prices down). The main causes were the higher energy prices and global supply chain problems.

Attention was firmly fixed on whether the Bank of England would increase UK interest rates at its meeting in early November, a widely expected move. But policymakers voted against raising the rate from the historical low of 0.1% to allow the jobs market to respond to the end of the furlough scheme.

Meanwhile, the annual inflation rate in the US climbed again. But higher consumer prices didn’t deter shoppers, with retail sales up from previous months. At the start of November the US Federal Reserve (Fed) announced it would reduce its bond-buying programme by $15 billion a month, but markets expected it so were unflustered by it. The Fed also re-iterated the need for a patient approach to raising interest rates.

Sven said: “We still see inflation moderating over the next 12 months because the energy price rises and supply bottlenecks should reverse themselves in the coming quarters – although they probably won’t reach their peak before early next year.”

US companies beat expectations

The third-quarter US earnings season kicked off in October. By the end of the month, around 80% of the companies that had announced beat expectations, which further supported the equity rally.

Although company costs have gone up with inflation riding high, many firms passed those costs on to their customers to maintain profits.

The US’s heavyweight tech sector saw particularly impressive gains that pushed the S&P 500 to its record highs towards month-end.

Coutts was proud to be a Principal Partner of the COP26 event in Glasgow. Our special report, The Power Of Sustainability, covers how we're working towards building a better world.

OUR LONG-TERM PERFORMANCE

30 Sept 2016 to 30 Sept 2017 |

30 Sept 2017 to 30 Sept 2018 |

30 Sept 2018 to 30 Sept 2019 |

30 Sept 2019 to 30 Sept 2020 |

30 Sept 2020 to 30 Sept 2021 |

|

MSCI World (sterling, including income) |

14.4% |

14.4% |

7.8% |

5.2% |

23.5% |

Coutts Defensive Portfolio |

4.2% |

1.4% |

5.4% |

-0.4% |

3.2% |

Peer group - ARC Cautious PCI |

3.9% |

1.3% |

3.4% |

1.5% |

6.3% |

Composite benchmark |

2.8% |

2.3% |

11.1% |

2.6% |

2.2% |

Coutts Balanced Portfolio |

8.5% |

4.0% |

4.6% |

-0.4% |

10.2% |

Peer group - ARC Balanced Asset PCI |

6.1% |

3.1% |

3.6% |

0.5% |

10.9% |

Composite benchmark |

6.1% |

5.0% |

9.4% |

0.7% |

9.1% |

Coutts Growth Portfolio |

11.9% |

6.9% |

3.7% |

-0.8% |

18.0% |

Peer group - ARC Steady Growth PCI |

8.7% |

5.2% |

3.8% |

-0.2% |

15.0% |

Composite benchmark |

9.7% |

7.7% |

7.7% |

-1.7% |

16.2% |

Return data for funds are calculated net of fees, in sterling and assumes reinvestment of dividends. Past performance should not be taken as a guide to future performance. Peer group returns provided by Asset Risk Consultants (ARC). Benchmarks represent a static mix of equities and bonds in proportions relevant to each strategy. The value of investments, and the income you get from them, can go down as well as up, and you may not recover the amount of your original investment. Source: Coutts & Co., Asset Risk Consultants (ARC), Morningstar, Refinitiv, November 2021

Share