Markets have a spring in their step

Equity markets strengthened against a more robust outlook for the global economy in March, which was positive for our portfolios.

3 min read

SHARE

Most Popular

-

Ukraine invasion: Keeping our clients informed | Coutts

15 Mar 20221 min

-

Coutts and charitable giving in the Covid era

02 Dec 20214 min

Become A Client

When you become a client of Coutts, you will be part of an exclusive network.

March felt like a much more ‘normal’ month for investors and there were fewer surprises than earlier in the year. After spiking in February, bond yields stabilised and the knock-on effects to other parts of the market faded.

Optimism about the rapid deployment of vaccines and the recovery continued to boost global equities, despite disrupted distribution in the EU. Economic data remained strong and the additional fiscal stimulus announced in the UK and US during March bolstered investor confidence.

Bonds continued to underperform in March, although less so than in February. Prices have fallen as investors shift to equities, but also as a reaction to the potential for higher inflation, which reduces the attractiveness of bond income.

Overall, the MSCI World Index of global equities returned 4.2% in March (local currency basis, including income), while US 10-year Treasury bonds returned -1.5% (US dollar basis).

Looking back over the first quarter of the year, the trends that were established in the last months of 2020 continued. After a strongly positive year, tech has been weaker in 2021, and investors have continued to favour companies that tend to do well as the economy improves. These include sectors like energy, materials and financials, as they provide vital resources and support for businesses as they step up production to meet rising consumer demand.

Strength of global equities supports returns

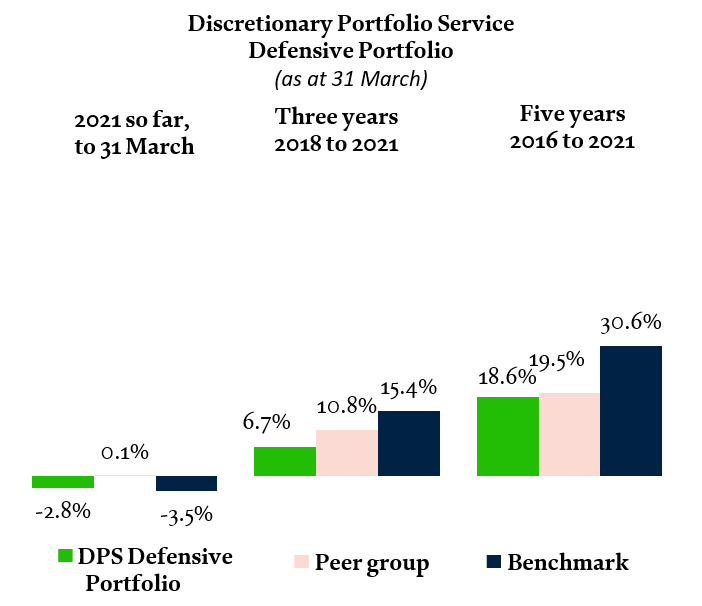

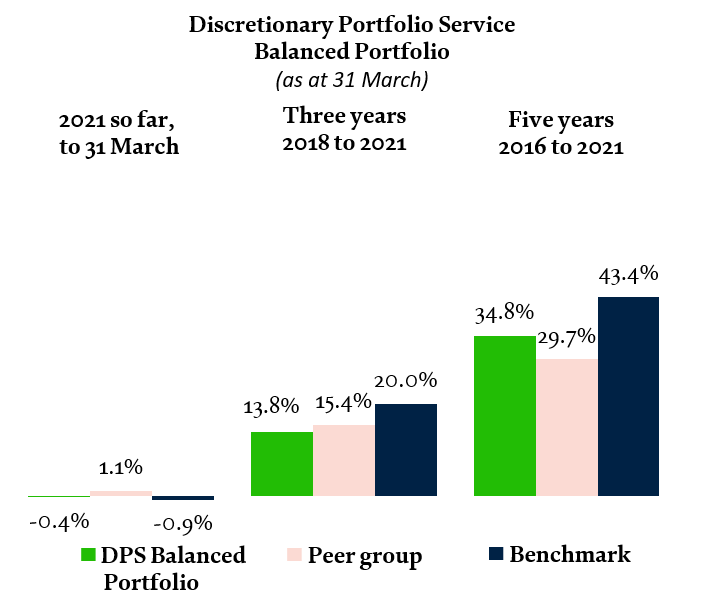

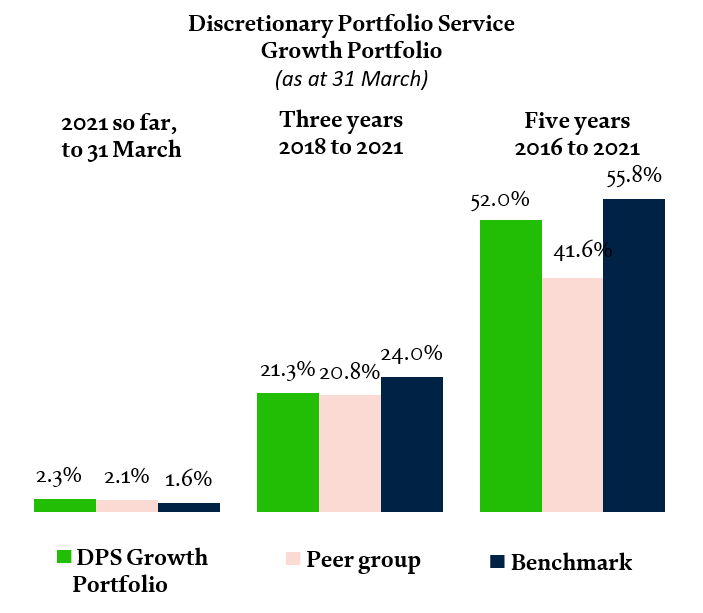

All strategies were positive in March. We also outperformed our internal benchmark in the first quarter of 2021 and over the last 12 months as we navigated the most difficult period of the crisis. We’ve maintained our preference for equities over bonds, and growth strategies – with a high allocation to equities – have benefited most from market moves. Defensive strategies had a more difficult time due to their allocation to government bonds.

Our US banks investment theme was beneficial in March and over the quarter, as the financial sector continues to benefit from the brightening economic outlook. Bonds issued by financial companies and short-dated emerging market bonds (denominated in hard currencies, primarily US dollars) have been positive over the quarter. These investments are less sensitive to interest rate rises, the possibility of which caused bond yields to rise (ie, prices to fall) in February as investors grew concerned about inflationary pressures.

Following this positive performance, we took profits from our holdings in EM as well as investment grade bonds in March, as we don’t see much room for further appreciation relative to government bonds. We’ve used the money to add tactically to UK government bonds while prices have retraced; while we don’t see much potential for big gains in the near future, they continue to be an important way to stabilise portfolios during periods of equity market turbulence.

Cumulative returns calculated on sterling basis, including fees, charges and income to 31 March 2021. These data are based on composite performance, individual portfolio monthly returns are asset-weighted based on their respective asset values at the beginning of the month. Peer group returns provided by Asset Risk Consultants (ARC); end-March data represents ARC estimate. Past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can go down as well as up and you may not recover the amount of your original investment. Sources: Coutts & Co, ARC. April 2021.

This is just a narrow snapshot of recent performance. For a more detailed view, refer to the tables at the end of this article.

UK equities should benefit from brighter outlook

The UK’s vaccination programme continues to make rapid progress, and the government’s latest Budget outlined more spending on workers and businesses until the autumn to cushion the blow of the pandemic. As a result, the outlook for the UK economy remains positive.

At the beginning of March, we took profits in Chinese equities and added to UK equities. China has performed well, and it was time to bank those gains. On the other hand, the UK has been undervalued for some time and should benefit from the rotation to economically sensitive sectors, as well as a general improvement in sentiment and less uncertainty associated with Brexit. With this in mind we’ve topped up our negative position in the UK to a more neutral weight.

Vaccines and economic stimulus boost market health

In the US, President Joe Biden’s $1.9 trillion stimulus package finally passed through both houses of Congress. According to the OECD, the stimulus should turbocharge the US economy and boost global growth when considered alongside the country’s rapid vaccination programme. Overall, the OECD expects the global economy to expand by 5.6% in 2021, an improved outlook from their previous estimate of 4.2%.

Europe has been slow to deploy its €1.8 trillion pandemic relief package and its vaccine rollout has been delayed due to manufacturing and procurement issues. But concerns about a potential third wave didn’t seem to deter investors in March, as Europe was one of the better-performing regions over the period. Looking ahead, while there is some catching-up to do, we believe that improving vaccination distribution and the impact of stimulus when it arrives will be good for Europe later in the year.

You can find a more detailed take on our view for the rest of the year as part of our spring investment focus, Here Comes the Sun.

As economic conditions begin to stabilise around the world, we’ve sold our position in gold. We originally increased our investment in this safe-haven asset during the extreme market conditions of 2020 as inflation and interest rates plummeted. As economic conditions have stabilised, we believe it’s less useful as a diversifier.

long-term PERFORMACE

31 March 2016 to 31 March 2017 |

31 March 2017 to 31 March 2018 |

31 March 2018 to 31 March 2019 |

31 March 2019 to 31 March 2020 |

31 March 2020 to 31 March 2021 |

|

MSCI World (local currency, including income) |

31.9% |

1.3% |

12.0% |

-5.8% |

38.4% |

Coutts Defensive Portfolio |

9.2% |

1.8% |

1.7% |

-1.6% |

6.6% |

Peer group - ARC Cautious PCI |

7.1% |

0.7% |

1.7% |

-2.3% |

11.5% |

Composite benchmark |

11.2% |

1.8% |

5.0% |

3.3% |

6.4% |

Coutts Balanced Portfolio |

15.3% |

2.7% |

2.8% |

-4.6% |

16.0% |

Peer group - ARC Balanced Asset PCI |

11.5% |

0.8% |

3.0% |

-5.4% |

18.5% |

Composite benchmark |

17.3% |

1.9% |

6.2% |

-1.5% |

14.6% |

Coutts Growth Portfolio |

21.4% |

3.3% |

4.1% |

-9.0% |

28.1% |

Peer group - ARC Steady Growth PCI |

15.8% |

1.3% |

4.8% |

-7.7% |

24.8% |

Composite benchmark |

23.0% |

2.1% |

7.5% |

-6.3% |

23.1% |

Returns calculated on a sterling basis, including fees, charges and income. Discretionary portfolio calculated based on composite performance, individual portfolio monthly returns are asset-weighted based on their respective asset values at the beginning of the month. Peer group returns provided by Asset Risk Consultants (ARC); end-March 2021 data represents ARC estimate. Past performance should not be taken as a guide to future performance. The value of investments, and the income you get from them, can go down as well as up and you may not recover the amount of your original investment. Sources: Coutts & Co, ARC, Investment Association, Thomson Reuters Eikon/Datastream. March 2021.

Share