Consolidating markets

The coronavirus Delta variant affected economies and markets around the world in July, while China moved to restrict private companies.

3 min read

SHARE

Most Popular

-

Ukraine invasion: Keeping our clients informed | Coutts

15 Mar 20221 min

-

Coutts and charitable giving in the Covid era

02 Dec 20214 min

Become A Client

When you become a client of Coutts, you will be part of an exclusive network.

The Delta variant of the coronavirus caused a rise in cases in many regions in July, tasking policymakers with vaccinating a majority of the public and getting ahead of the new strain to enable the lifting restrictions with confidence. In particular, a spike in the rate of infections in the US and Europe led to concerns about whether the economic recovery would remain on track. While we think that economic growth will moderate from the current very high levels, it will remain strong overall.

Towards the end of the month, markets experienced an unstable period, but fears were alleviated by the expectation of continued support from central banks as well as strong corporate earnings in both the US and Europe. Overall, the MSCI World Index of global equities rose 1.79% in July, while US 10-year Treasury bonds returned 2.0%. In fixed income, bond yields accelerated their decline in July pushing up prices of sovereign bond and investment grade credit.

CHARTING A WAY THROUGH CHOPPY MARKETS

We’ve made a number of changes to portfolios in recent months that have helped us navigate these market conditions. They include adding an overweight position in the global healthcare sector. We believe the sector has attractively priced fundamentals and a stable earnings outlook that is less pressured by rising input prices.

After the price appreciation of gilts and investment grade credit we saw in July, we sold some of both, buying in their place high yield and Chinese sovereign bonds. The recent action in bond yields has surprised many investors and the reasons for it are hotly debated. We think a consolidation is now warranted as well and increased our underweight in both.

As economic activity looks set to moderate from its very elevated levels, our portfolios remain well balanced. Investors will be pondering interest rates moves, earnings reports and especially FED monetary policy guidance in August.

Emerging market equity saw more weakness in July. After last year’s great run, we had sold our standalone Chinese equity position in March. We further reduced our broad emerging market equity exposure in May in light of the China-led economic slowdown in Asia. As a result, our portfolios and funds were barely impacted by the rapid market decline of Chinese and Hong-Kong equities towards the end of July.

GROWTH JOINS INFLATION AS A TOUCHPOINT

The first half of this year was marked by the re-opening of economies which then sparked a rapid rise of inflation. Consumer spending and input prices have risen, and investors moved into sectors and regions that could benefit from this trend, such as banks and European equities. However, markets readjusted in July owing to concerns over whether good news about the recovery itself had already been priced in. Any anxiety around rising inflation has been largely overtaken by concerns over the Delta variant of the virus and whether it could slow the recovery.

Against this background, we saw a change in sector preferences to growth (Technology and Healthcare) and away from value sectors (Transport or Industrials).

This is reflected in the negative returns from Japanese and emerging market equities while markets in the US, UK and EU fared better. High quality bonds, like US Treasuries and UK Gilts ended the month in positive territory. We expect to see continued sector and regional rotation as markets consolidate between concerns about growth and concerns about inflation. However, we are still positive about the outlook, and expect the recovery to reaffirm itself and continue into the first half of next year. More volatility is likely, but this will allow us to identify opportunities as they present themselves.

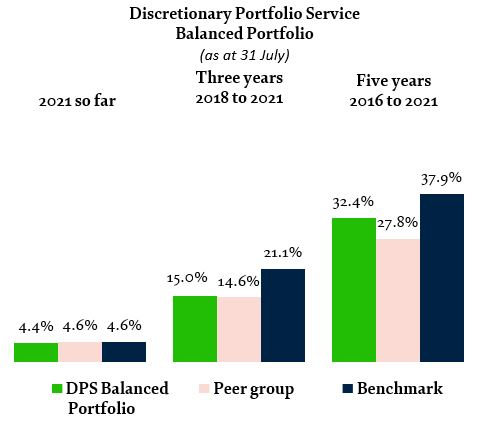

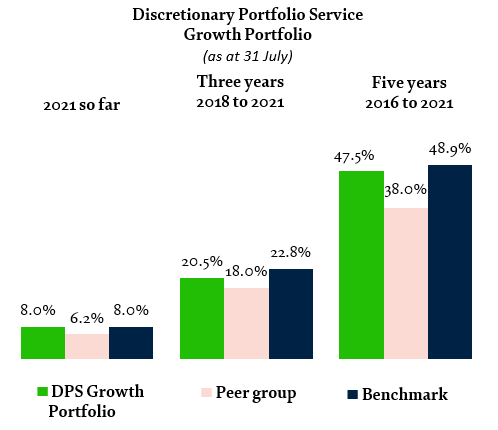

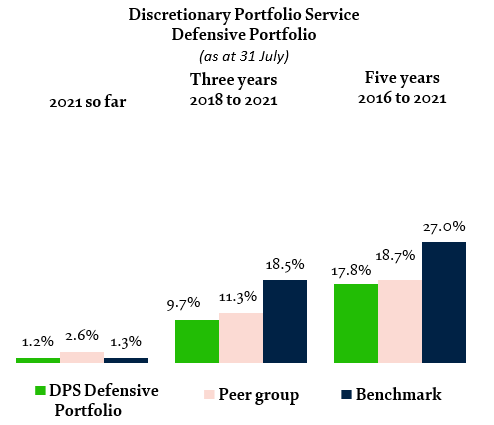

POSITIVE MARKET PERFORMANCE CONTINUES IN CLIENTS’ PORTFOLIOS AND FUNDS

The portfolio performance shown below is net, so has fees and charges deducted, while the benchmark performance is gross with no such deductions.

Cumulative returns calculated on sterling basis, including fees, charges and income to 31 July 2021. These data are based on composite performance, individual portfolio monthly returns are asset-weighted based on their respective asset values at the beginning of the month. Peer group returns provided by Asset Risk Consultants (ARC); end-July data represents ARC estimate. Benchmarks represent a static mix of equities and bonds in proportions relevant to each strategy. Past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can go down as well as up and you may not recover the amount of your original investment. Sources: Coutts & Co, ARC. August 2021.

“The latest actions by Chinese authorities signal again that the traditional ‘growth at any price’ policy is finished. Policy now allows for a higher tolerance for short-term pain in exchange for long-term gain on topics like demography or wealth inequality. Chinese policymakers will however not risk letting equity market volatility threaten domestic economic stability or private-sector investment.”

Sven Balzer, Head of Investment Strategy, Coutts

CHINESE EQUITY SETBACK

Emerging market equities have been weakening for some time. Due to low vaccination rates, the COVID impact (accelerated by the Delta variant) has been more negative than in Europe or the US. China has also been reducing monetary and fiscal support for some time and that, coupled with a stronger USD, are headwinds for the region. Towards the end of the month, China announced new regulations impacting private tutoring firms, which in turn led to a sharp fall in the share prices of those firms impacted, including two of the largest players in the sector. The regulations prohibit foreign investment and designate after-school tutoring firms as ‘non-profit’ institutions, basically killing the business model of the whole sector. This move marked a continuation of the trend in increasing government regulatory oversight in the affairs of high-profile companies. However, despite what we saw in July, we don’t think the Chinese government will allow volatility in equity markets to threaten domestic economic stability, as was evidenced by the continued stability of Chinese government bonds and the Yuan in the currency markets.”

long-term PERFORMAnCE

Name |

30 June 2016 to 30 June 2017 |

30 June 2017 to 30 June 2018 |

30 June 2018 to 30 June 2019 |

30 June 2019 to 30 June 2020 |

30 June 2020 to 30 June 2021 |

MSCI World (local currency, including income) |

18.8% |

10.9% |

6.7% |

3.3% |

36.9% |

Coutts Defensive Portfolio |

7.7% |

1.7% |

3.1% |

1.8% |

3.4% |

Peer group - ARC Cautious PCI |

6.5% |

1.4% |

2.4% |

1.7% |

7.1% |

Composite benchmark |

5.4% |

3.0% |

6.5% |

7.4% |

2.6% |

Coutts Balanced Portfolio |

13.2% |

4.2% |

3.6% |

0.7% |

10.5% |

Peer group - ARC Balanced Asset PCI |

10.6% |

3.0% |

2.7% |

0.5% |

11.5% |

Composite benchmark |

9.8% |

5.0% |

6.6% |

4.4% |

8.9% |

Coutts Growth Portfolio |

18.3% |

6.5% |

3.9% |

-1.1% |

18.8% |

Peer group - ARC Steady Growth PCI |

14.4% |

4.9% |

3.5% |

-0.5% |

15.4% |

Composite benchmark |

14.6% |

7.1% |

6.7% |

1.2% |

15.4% |

Return data for funds are calculated net of fees, in sterling and assumes reinvestment of dividends. Past performance should not be taken as a guide to future performance. Peer group returns provided by Asset Risk Consultants (ARC). Benchmarks represent a static mix of equities and bonds in proportions relevant to each strategy. The value of investments, and the income you get from them, can go down as well as up, and you may not recover the amount of your original investment. Source: Coutts & Co., Asset Risk Consultants (ARC), Morningstar, Reuters/Eikon Datastream, July 2021

Share