Vaccine breakthrough soothes market ills

Positive news about coronavirus vaccines boosted markets in November as investors embraced the idea of a COVID recovery

3 min read

SHARE

Most Popular

-

Ukraine invasion: Keeping our clients informed | Coutts

15 Mar 20221 min

-

Coutts and charitable giving in the Covid era

02 Dec 20214 min

Become A Client

When you become a client of Coutts, you will be part of an exclusive network.

Global stock markets soared following the announcement that Pfizer and BioNTech’s COVID-19 vaccine proved to be more than 90% effective in late-stage trials. Alongside a gradually rising sense of political stability in the US after Joe Biden’s victory in the US presidential election, the breakthrough provided a sense of relief to investors.

The MSCI All Country World index reached a record high, returning 9% by the end of November (in sterling, income reinvested).

Vaccine news boosts lockdown laggards

The good news kept coming, with vaccines developed by Moderna as well as Oxford University and AstraZeneca also showing promising results. In response, there’s been a substantial rotation into the areas of the market that had been hard hit during lockdown, such as financials, energy, transportation and hospitality.

While hopes of a vaccine have spurred investors to shift their portfolios away from growth stocks, they’ve continued to perform well too. Elsewhere, very defensive sectors struggled, and investment grade corporate bonds, financial credit and emerging market debt outperformed safe-haven government bonds and gold.

After a long period of underperformance, the UK did particularly well this month – the MSCI UK Index returned 13.1% in November. European stocks also benefited from the change of mood, with the MSCI Europe Index returning 13.4%.

Focus on cyclical stocks pays off

Since April, we’ve been adding equities in markets and sectors that we think will benefit from an economic recovery and boosting our holdings in equities relative to defensive assets like government bonds. We’ve taken profits from the US, which has done well during the lockdown months largely thanks to the high number of tech companies, and bought into economically sensitive areas that offered good value and the potential for recovery, such as banks, emerging markets and Japan.

We also have a structural bias to the UK in our sterling funds, which means that strong returns were beneficial for this month’s performance in absolute terms.

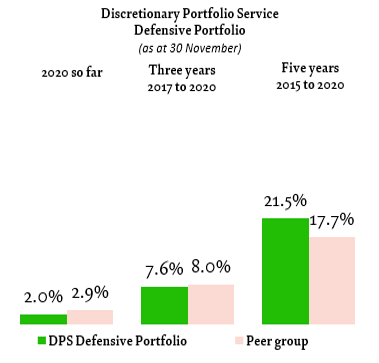

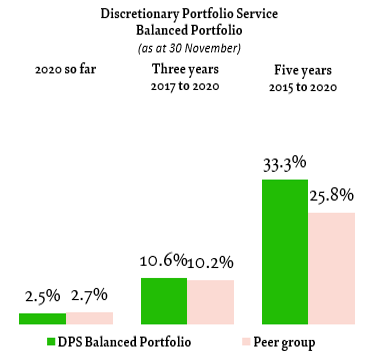

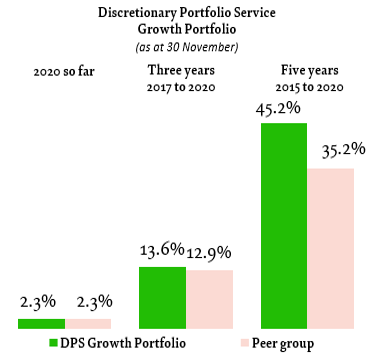

As a result, November was very positive for Coutts portfolios, which saw the strongest average monthly performance for several years. The average balanced portfolio was up 5.4% for November. With their high allocation to equities, the average growth portfolio rose by 8.1%, while even our defensive portfolios – which focus on lower risks assets – returned a healthy 3.0%.

As our tactical view for 2020 has begun to pay off, this has also lifted our performance over 2020 so far. At the end of November, the average balanced portfolio had returned 2.5% since the start of the year, including the impact of plummeting markets in March. The average growth portfolio has returned 2.3% while the average defensive portfolio has returned 2.0%.

These results demonstrate the benefit of maintaining a long-term focus. While some of the areas we’ve been adding to over the year were unloved when pandemic-led uncertainty drove markets, we remained confident they would bounce back when growth and certainty returned. This certainty was rewarded this month.

And importantly, five-year performance remains consistently ahead of industry averages for similar strategies.

Cumulative returns calculated on sterling basis, including fees, charges and income to 30 November 2020. These data are based on composite performance, individual portfolio monthly returns are asset-weighted based on their respective asset values at the beginning of the month. Peer group returns provided by Asset Risk Consultants (ARC); end-October data represents ARC estimate. Past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can go down as well as up and you may not recover the amount of your original investment. Sources: Coutts & Co, ARC. November 2020.

As ever, you shouldn’t rely on past performance as an indicator of future returns. The value of investments, and the income you get from them, can go down as well as up and you may not get back the amount you invested. These figures provide a limited snapshot – for more context please refer to the table of long-term returns at the end of this article.

US election outcome positive for markets

Investors reacted positively to Joe Biden’s victory in the US presidential election. The race for the Senate continues in Georgia, with a special runoff election planned for January which will decide whether Republicans or Democrats control the House of Representatives.

With the US Federal Reserve providing economic easing, financial markets are comfortable with a balance of power in the US, and the Republicans are likely to moderate Biden’s plans to increase spending, raise taxes and tighten regulations. Although there could still be an impact on company earnings in the near term, the US has elected a moderate president which should be positive for equity markets.

The final countdown

In the UK, Brexit remains a concern. With less than a month to go until the Brexit transition period ends, a final deal is yet to be struck between the EU and UK. Although solid progress has been made, sticking points remain at the time of writing. While we still believe a deal is likely to be reached, we are watching progress carefully. Whatever the outcome, sterling is likely to feel the largest effect. Investors are generally expecting a deal to be reached, so a no-deal scenario could cause the pound to slide.

A more certain outlook reassures investors

Though it remains to be seen how safe and effective the coronavirus vaccines are and how quickly they can be rolled out, the news has provided hope for a possible return to normality soon. We remain positioned with a recovery in mind.

|

30 September 2015 to 30 September 2016 |

30 September 2016 to 30 September 2017 |

30 September 2017 to 30 September 2018 |

30 September 2018 to 30 September 2019 |

30 September 2019 to 30 September 2020 |

MSCI AC World Index |

30.6% |

14.9% |

12.9% |

7.3% |

5.3% |

MSCI Emerging Markets Index |

36.2% |

18.6% |

2.0% |

3.7% |

5.4% |

MSCI China Index |

31.7% |

28.8% |

0.6% |

1.7% |

27.3% |

Coutts Defensive Portfolio |

9.9% |

4.2% |

1.4% |

5.4% |

-0.4% |

Defensive strategy benchmark |

14.4% |

2.8% |

2.3% |

11.1% |

2.6% |

Coutts Balanced Portfolio |

13.5% |

8.5% |

4.0% |

4.6% |

-0.4% |

Balanced strategy benchmark |

18.6% |

6.1% |

5.0% |

9.4% |

0.7% |

Coutts Growth Portfolio |

17.8% |

11.9% |

6.9% |

3.7% |

-0.8% |

Growth strategy benchmark |

22.4% |

9.7% |

7.7% |

7.7% |

-1.7% |

Past performance should not be taken as a guide to future returns. Portfolio performance figures are composite returns from the actual portfolios of all clients calculated in sterling, shown on a total return basis and quoted net of all fees. For the composite portfolio performance calculation, individual portfolio monthly returns are asset-weighted based on their respective asset values at the beginning of the month. Benchmarks represent a static mix of equities and bonds in proportions relevant to each strategy. Source: Coutts & Co, November 2020.