Life after Brexit – Opportunity in the UK?

With Brexit behind us and COVID clouds clearing, we could see a revival of fortunes for UK equities.

4 min read

SHARE

Most Popular

-

Ukraine invasion: Keeping our clients informed | Coutts

15 Mar 20221 min

-

Coutts and charitable giving in the Covid era

02 Dec 20214 min

Become A Client

When you become a client of Coutts, you will be part of an exclusive network.

The double headwinds of the COVID-19 pandemic and Brexit may be abating. A lot of the Brexit-related uncertainty should end soon and a vaccine against COVID-19 is making its way to the population, meaning economic recovery is in sight.

Against this backdrop, based on our research, UK equities stand out as under-owned, attractively valued and heavy in economically sensitive sectors that could outperform in an economic recovery. This could make them attractive as the world gradually returns to normal.

how we got there - the brexit shock

The British national character is renowned for its stiff upper lip. But while British companies have endeavoured to remain stoical through a period of historic uncertainty, there can be no avoiding the impact of the vote to leave the European Union (EU) and the compounding effect of the COVID-19 epidemic in 2020.

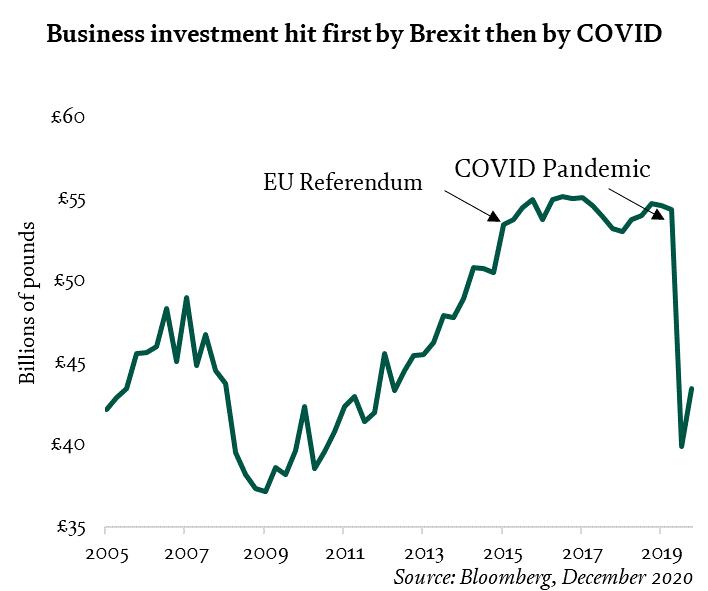

The impact can be very clearly seen in business investment data.

After the EU referendum result, a steadily rising trend in business investment was stopped in its tracks. It’s worth remembering that at the time of the vote, most polls suggested a remain result, albeit with a narrow margin, and so the vote to leave came as a surprise to many. Businesses that had a settled strategy for the coming years suddenly had those plans thrown unexpectedly into disarray.

Investment then collapsed when the COVID-19 pandemic hit the world. What’s more, it’s recovering only slowly relative to other developed markets. In the third quarter of 2020, it recovered less than 25% of its losses from the previous three months; the US, in contrast, recovered over half the decline in investment over the same period.

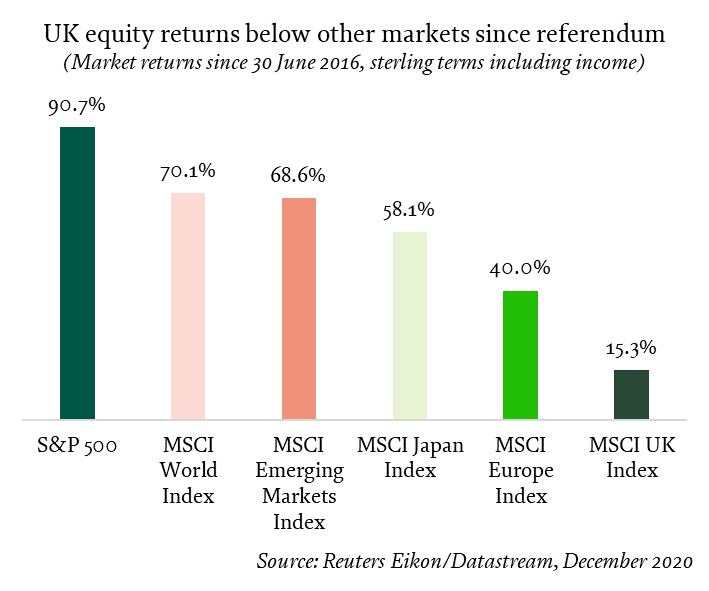

Uncertainty around the UK’s relationship with Europe has led many investors to shy away from British companies. The UK is under-owned by global investors and share prices have stagnated relative to other markets.

Past performance is not a guide to future returns. The value of your investments, and the income you receive from them, can go down as well as up and you may not get back as much as you invested. Returns calculated on local currency basis including income. See charts below to get a better understanding of long-term investment performance.

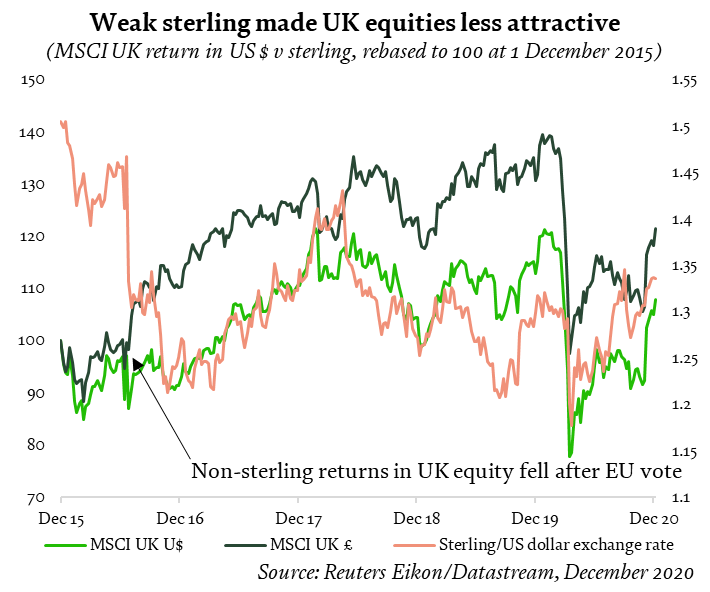

As well as uncertainty over the impact of the future trade relationship with the UK’s biggest and nearest market, a weaker pound has added to investor concerns.

If you’re a dollar-based investor, every cent by which the value of the pound falls means your investment loses value, regardless of share price movements. And if you invest in sterling, a falling pound makes your non-sterling investments more valuable, encouraging domestic investors to look outside the UK.

Past performance is not a guide to future returns. The value of your investments, and the income you receive from them, can go down as well as up and you may not get back as much as you invested. Returns calculated including income. See charts below to get a better understanding of long-term investment performance.

Sterling has been on a rollercoaster since the June 2016 Brexit vote. From trading at near $1.50 before the referendum, the pound has had several brief forays below $1.20 - its lowest level since the 1980s. It is now trading in a range of around $1.30 to $1.35, indicating that a Brexit discount remains.

The Coutts approach – finding opportunities for our clients

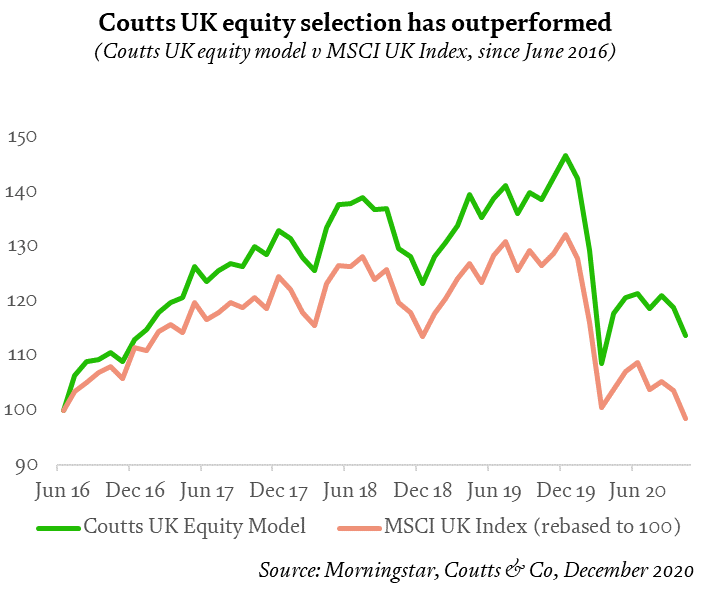

At Coutts, our UK model has outperformed the UK market since 2016.

We’ve favoured ‘quality’ companies in the UK for those four years. These are typically well-established, large-cap companies with a dependable international market, which we saw as more resilient and better able to navigate these exceptional times.

We added a specific domestic theme in early 2019, when we thought the valuation differential between domestically and internationally focused companies indicated excessive pessimism over the chances of a no deal outcome. Our view was that, once these fears abated, domestically oriented companies would increase in value.

Both those decisions performed strongly within our client portfolios and funds.

Past performance is not a guide to future returns. The value of your investments, and the income you receive from them, can go down as well as up and you may not get back as much as you invested. Returns calculated on a sterling basis including income. See charts below to get a better understanding of long-term investment performance.

REASONS TO BE optimistic about uk equities

a) Under owned

Most fund managers have a low allocation to UK equities. The Bank of America Global Fund Manager survey for November 2020 showed that net allocation to UK equities was 33% below the long-term average. As the outlook has started to improve, global investors started adding to their allocations, and as demand increases prices could rise.

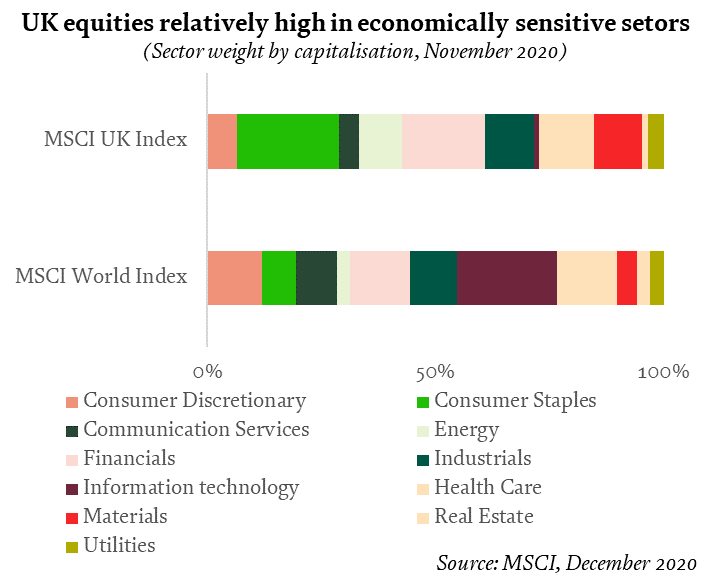

b) Cyclical bias

The UK market has a higher component of sectors that are more sensitive to the economic cycle – commonly called ‘cyclical’ sectors – including energy, financials and materials. This means they perform well relative to other sectors as the economy expands, and conversely do less well during times of contraction.

This partly explains the poor performance of UK equities during the COVID-19 pandemic, but it also means that UK equities could outperform as the global economy improves in 2021.

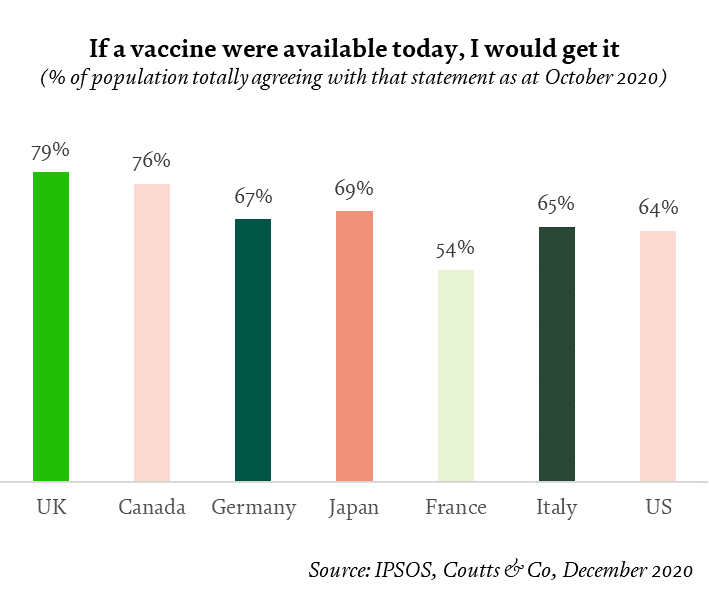

c) Vaccination response

The UK is at an advantage versus other countries in terms of its ability to vaccinate the population. In terms of doses ordered per capita, the UK is second only to the US globally, and the British public also appears to be more willing to take a vaccine than their peers in other developed markets.

d) Low likelihood of negative interest rates

The Bank of England has been considering the possibility of negative rates for some time. While we don’t expect significantly higher rates any time soon, tackling the COVID crisis will reduce the possibility of negative rates in 2021. This removes a significant headwind for UK banks and other financial companies, which are a significant part of the UK equity index.

While Brexit will dominate the British economy for years to come, and the overall impact is hard to judge, the end of negotiations will improve clarity at the very least. Combined with the reopening of economies across the world and the massive support from central banks and governments, the outlook for the UK is improving.

We believe a change in focus could be a catalyst for investors to start reconsidering the case for UK assets. Combined with global economic developments, positive for companies like the ones featuring in UK indices, we see potential for a brighter outlook for UK shares at the start of 2021. Longer-term outperformance of UK equities will require a sustained economic recovery and higher inflation globally.

long-term market performance

|

30 September 2015 to 30 September 2016 |

30 September 2016 to 30 September 2017 |

30 September 2017 to 30 September 2018 |

30 September 2018 to 30 September 2019 |

30 September 2019 to 30 September 2020 |

MSCI World Index (local currency basis) |

10.5% |

17.9% |

12.3% |

2.9% |

8.5% |

MSCI UK Index (sterling) |

18.4% |

11.0% |

5.8% |

2.8% |

-19.8% |

MSCI Emerging Markets (local currency basis) |

13.0% |

21.8% |

2.7% |

-0.2% |

12.5% |

MSCI Japan Index (yen basis) |

30.7% |

10.5% |

13.4% |

0.9% |

1.9% |

MSCI Europe ex UK Index (euro terms) |

20.0% |

21.4% |

1.3% |

5.9% |

-0.5% |

S&P 500 (US dollar basis) |

34.6% |

14.8% |

21.3% |

10.3% |

9.8% |

Past performance should not be taken as a guide to future returns. Returns calculated on local currency basis, including income. Source: Coutts & Co, Thomson Reuters/Eikon, December 2020.