US election: Backing the winner

We get under the hood of our funds and portfolios to find what the US election result could mean for our investment clients

4 min read

SHARE

Most Popular

-

Ukraine invasion: Keeping our clients informed | Coutts

15 Mar 20221 min

-

Coutts and charitable giving in the Covid era

02 Dec 20214 min

Become A Client

When you become a client of Coutts, you will be part of an exclusive network.

Most Popular

-

CIO Update – Managing risk amid periods of uncertainty | Insights | Coutts

10 Oct 20253 min Whether financial markets ever face a downturn again in the future isn’t a matter of ‘if’ but ‘when’. While it’s impossible to predict the exact moment, managing risk in our portfolios in advance of future events is fundamental to our investment philosophy and process. Read our latest CIO update.

Whether financial markets ever face a downturn again in the future isn’t a matter of ‘if’ but ‘when’. While it’s impossible to predict the exact moment, managing risk in our portfolios in advance of future events is fundamental to our investment philosophy and process. Read our latest CIO update.

-

How could the Budget affect your inheritance planning? | Insights | Coutts

08 Oct 20254 min Coutts Wealth Structuring Manager Irene Wolstenholme and Head of Specialists Greg Kyle-Langley have assessed the current tax landscape and what might change in the upcoming Autumn Budget. They share their view on key considerations when planning for the future.

Coutts Wealth Structuring Manager Irene Wolstenholme and Head of Specialists Greg Kyle-Langley have assessed the current tax landscape and what might change in the upcoming Autumn Budget. They share their view on key considerations when planning for the future.

As the day of the US election draws near, investors are reading the auguries to try and divine the potential result. While nothing's certain even at this late stage, it makes sense to consider the core scenarios that may impact markets and investors in the weeks ahead.

Bonds point to Biden

60%

Approximate chance of ‘blue wave’ victory for Democrats taking the Presidency and both houses of the Congress according to betting odds

(Source: Bloomberg/Predictit)

Right now, market behaviour indicates that investors are reasonably confident of a Biden victory. Betting odds – which are often a good indicator of conviction among people with money at stake – put the chance of a Biden win at 60%. (Source: Bloomberg/Predictit)

Rising bond yields (meaning lower bond prices) are one indicator that markets expect a Democrat victory. A Democrat president – particularly with the backing of a Democrat House and Senate – will swiftly introduce a generous government support package for people and companies affected by the coronavirus pandemic. This should lead to higher spending, improved economic growth and higher inflation, all of which are negative for bonds.

We can see that bond yields have risen as the odds of a Biden victory has improved. While the rise is modest relative to longer-term moves, it shows the market expectation that that the support package will be bigger than previously anticipated.

At Coutts, we've been cautious on government bonds for some time due to structurally low interest rates and yields. This means our funds and portfolios have a low allocation to them. In the event of a Trump victory and a revival for government bonds we could miss out on some short-term gain but this wouldn’t change our longer-term view that they don’t offer great value.

All things equal for equities

9.9%

Year-on-year growth in Chinese exports to September 2020, despite continued US trade hostilities

While there could be a sharp market reaction – positive or negative – to the result on the day, the medium-term effect on equities of a Trump or Biden victory is likely to be limited. Trump’s policies are slightly more ‘business friendly’; Biden has proposed increases to tax and regulation that could be a drag on corporate profit, although this could be offset by higher spending.

But these factors are secondary compared to the impact of the coronavirus on the economy and the measures the government takes to support the economy and employment. The speed with which a vaccine can be developed and deployed, and whether a second wave of infections will require more lockdown measures, are the backdrop for any policy proposed by either candidate. That said, a larger-than-expected support package could be positive for markets, and for specific sectors.

We're keeping an eye on some specific areas where politics could be influential:

- Banks - loan defaults since lockdown have been much lower than provisioned for, thanks to the substantial government support package agreed in April. Another large support package would help reduce bad debt risk in the sector even further.

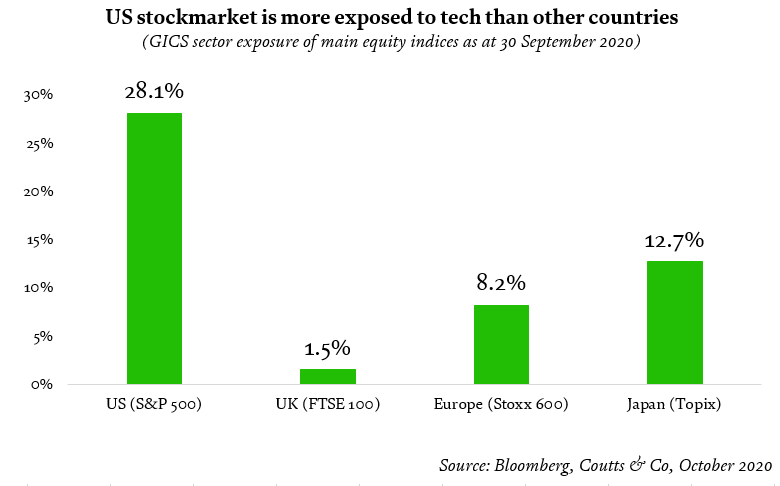

- Technology – both parties have challenged the big tech firms, and there’s broad agreement that their monopolistic positions require some kind of response. The Justice Department has just announced anti-trust proceedings against Google, and there may be more to come.

- Health care – Joe Biden is committed to allowing hospitals and other health care providers to negotiate more widely when sourcing drugs and medicines to reduce costs. This could be a negative for pharmaceutical companies.

- Emerging markets – Both parties are concerned about China’s growing economic power and policies, although a less erratic foreign policy under Joe Biden could be helpful for emerging markets. But China is doing well regardless of Trump’s rhetoric – its share of global exports is currently at an all-time high – and if this continues it'll benefit the whole sector.

“While there could be a sharp market reaction – positive or negative – to the result on the day, the medium-term effect on equities of a Trump or Biden victory is likely to be limited.”

THE POTENTIAL IMPACT ON COUTTS INVESTORS

20%

Exposure to US equities in average Coutts sterling balanced portfolio

At Coutts, while we believe long-term trends will favour technology and health care, we don’t have specific positions in these sectors at the moment. We reduced our weighting to the US recently, which has a high concentration of tech companies, and this has slightly reduced our exposure to tech companies.

Investors could move into areas of the market more sensitive to economic growth – such as banks – as fiscal and monetary stimulus take hold and a vaccine becomes available.

We added US banks as a portfolio theme in June. A generous support package from the Democrats could be positive for the sector and helpful for our portfolios and funds. On the other hand, we don’t anticipate a major sell-off in banks should Biden lose, and even more modest support measures would be supportive.

We have a slight bias towards emerging markets, and Asia in particular, including a direct holding in China – about 1% of the average balanced portfolio. This could benefit from China’s continued economic growth and a steadier approach to foreign policy that could come from a Biden administration could be positive for China and surrounding countries.

The third alternative – no result on the night

There's a possibility that there'll be no clear result on the night. While not our central scenario, the chances of this happening have risen thanks to the huge increase in the number of people choosing to vote by post due to social distancing considerations. In addition, President Trump has equivocated on his willingness to accept anything other than a landslide defeat, which may lead him to hang on to the bitter end before conceding.

We'd expect equity markets to fall in this scenario. As we’ve often said, markets hate uncertainty and any sign of political turmoil in the world’s biggest economy will be particularly unwelcome.

While the depth of the dip will depend on the nature of the dispute, we'd expect the negativity to pass when the issue resolves. Investor confidence will gradually return, whoever ends up victorious.

Obviously, our funds and portfolios won’t be immune from any short-term volatility, and we may even see a buying opportunity. But when the dust clears, our experience suggests that investors tend to refocus on the underlying economic drivers of long-term investment returns.

Looking back at US history, the presence of a Democrat or Republican in the White House has not been a decisive factor for US equity market performance. Markets have done well under both in the past, and it is monetary policy, productivity, innovation and earnings growth that ultimately determine asset price returns.

You can read our earlier analysis on the election and the candidates here.

When investing, past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can go down as well as up, and you may not recover the amount of your original investment.

Share

About Coutts investments

With unstinting focus on client objectives and capital preservation, Coutts Investments provide high-touch investment expertise that centres on diversified solutions and a service-led approach to portfolio management.

Discover more about Coutts investmentsMost Popular

-

CIO Update – Managing risk amid periods of uncertainty | Insights | Coutts

10 Oct 20253 min

Whether financial markets ever face a downturn again in the future isn’t a matter of ‘if’ but ‘when’. While it’s impossible to predict the exact moment, managing risk in our portfolios in advance of future events is fundamental to our investment philosophy and process. Read our latest CIO update.

-

How could the Budget affect your inheritance planning? | Insights | Coutts

08 Oct 20254 min

Coutts Wealth Structuring Manager Irene Wolstenholme and Head of Specialists Greg Kyle-Langley have assessed the current tax landscape and what might change in the upcoming Autumn Budget. They share their view on key considerations when planning for the future.