Investing & Performance | 20 August 2025

CIO Update – US Interest rate uncertainty

The US central bank is yet to reduce interest rates this year amidst the current rate cutting cycle. But with the future of inflation unknown, could the next interest rate decision leave markets – and the President – unhappy?

The US Federal Reserve’s (Fed) decision to pause its rate cutting cycle so far in 2025 has left the central bank in hot water with President Donald Trump. However, given that the US economy has managed to weather this prolonged, gradual loosening of monetary policy, there’s been little in the way of reasoning for the Fed to cut rates sooner than necessary.

Markets are expecting a 0.25% interest rate cut at next month’s meeting, which would make it the first reduction since December last year.

Why the long wait?

Since mid-2023, inflation has shown its stubbornness and has failed to reach the central bank’s 2% target. Last week’s headline inflation was below expectations at 2.7% in July. Stock markets responded positively to this as expectations grew that the Fed will cut rates next month. Core inflation however, which strips out volatile goods, was above expectations at 3.1%

A further challenge for the Fed includes uncertainty over the true impact tariffs will have on prices. The postponement to when tariffs would take effect coupled with the front-loading of international orders to get ahead of the levies mean US businesses are yet to fully pass on these increased costs to consumers. This suggests that inflation – and ultimately consumers – are yet to feel the squeeze of tariffs.

What the data says

While investors are comfortable where prices are for the consumer currently, the cost of wholesale goods for businesses is starting to pick up. The Producer Price Index (PPI) reported a 12-month rise of 3.3%, up from 2.4% the month before. This can be a canary-in-the-coalmine for consumer price inflation (CPI): if producers face rising input costs, they often – but not always – pass those costs on to retailers, who then raise prices for consumers.

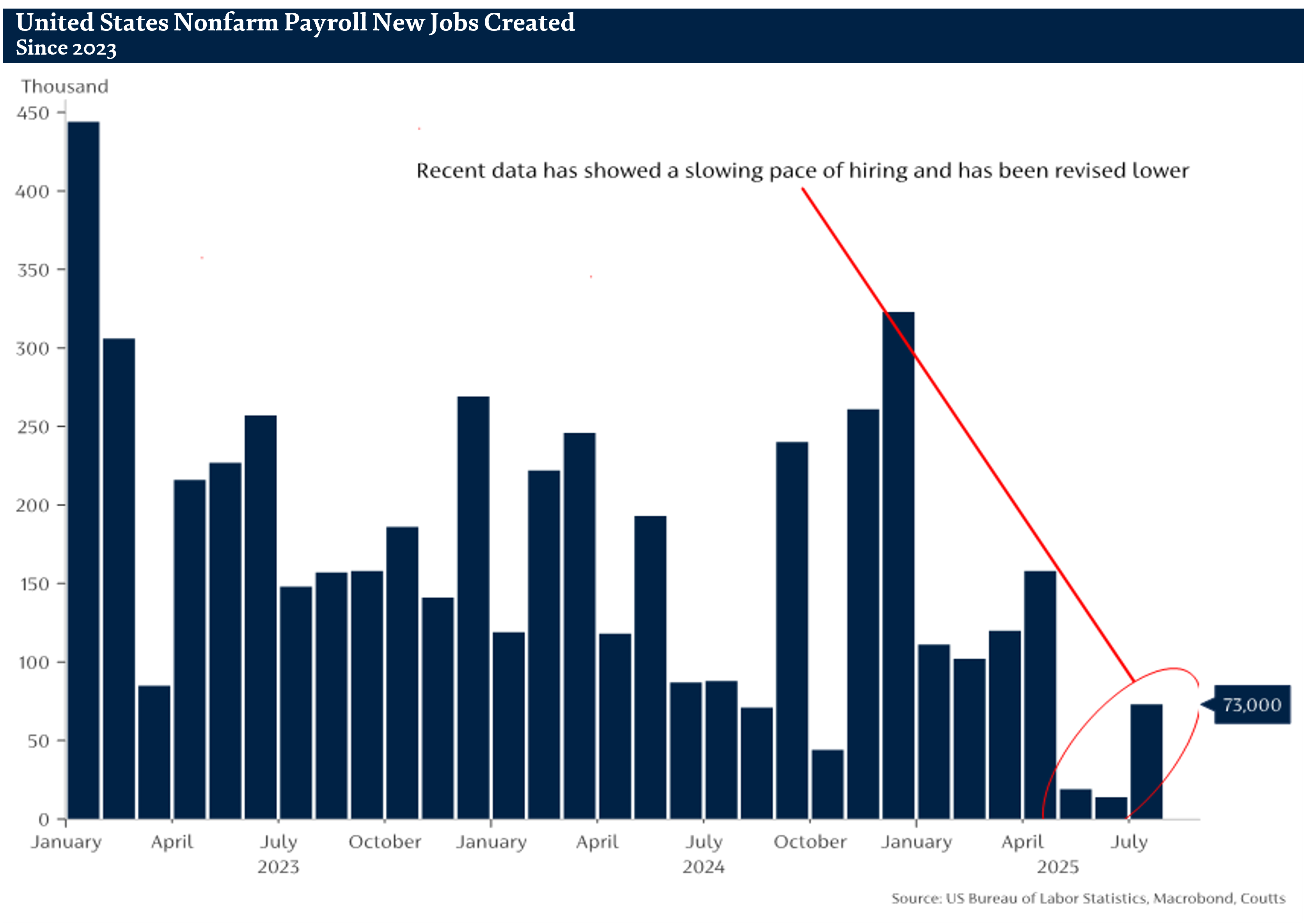

One of the main priorities for the Fed is to keep inflation down without being detrimental to economic growth. Currently, GDP growth is expected to remain positive with consensus for 1.6% in 2025. However, the jobs market is showing signs of weakening, partly because companies are bracing for the tariff impact by reducing job openings.

The above chart shows the number of US jobs created since 2023, according to the Bureau of Labor Statistics. The number of hires has begun to slow since President Trump’s ‘Liberation Day’ back in April. What took investors by surprise were the revisions made to the previously published payroll numbers in May and June. These figures were revised lower from 291,000 over the two-month period down to just 33,000.

Interest rate roadmap

Following this month’s PPI print, the dollar and short-term bond yields rose as investors managed their expectations that the Fed will cut interest rates when the committee next meet in September. Markets are still currently expecting a 0.25% cut, although a month is a long time considering that we will get refreshed inflation and jobs numbers before the announcement.

Our view:

- If the economy continues to weaken, the Fed could be more dovish in cutting interest rates over the course of this year and next. But from our perspective, this economic slowdown – most notably the labour market – does not mirror market behaviour that is typical at the start of a recession. Indeed, we may well be in the midst of a productivity boom, which boosts real wages and corporate profits.

- We believe rate cuts will resume, starting in September, however the roadmap for interest rates is less certain over the next 18 months. Our base case remains that recession will be avoided, relieving some pressure on the Fed to lower rates by too much, too soon. Given the current momentum of the economy, markets may be disappointed in the total number of cuts this year and next with rates expected to fall by 1.25% by the end of 2026.

- This is all under the assumption that the Fed continues to dispassionately analyse inflation and economic data. But political pressure to speed up rate cuts cannot be ruled out. Fed Chair Jerome Powell’s term is set to expire early next year, and a number of individuals have thrown their hats in the ring. President Trump has already voiced his opinion on where he wants interest rates to go, and Powell’s replacement would likely echo this strategy.

Past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can fall as well as rise and you may not get back what you put in. You should continue to hold cash for your short-term needs.

Speak to us

If you are a Coutts client and would like to discuss market developments or your own investments with us in more detail, please contact your private banker.

Share

More insights

CIO Update – Managing risk amid periods of uncertainty

The future of diversification

Monthly update: Rate Cuts, Resilient Earnings and the Rise of AI: A Market Perspective

When you become a client of Coutts, you'll be part of an exclusive network