“The endgame for LIBOR is now increasingly clear. There is no longer any reason for delay.”

Financial Conduct Authority (FCA)

-

What is SONIA?

WHAT IS SONIA?

What is SONIA?

Moving away from LIBOR to alternative interest rates

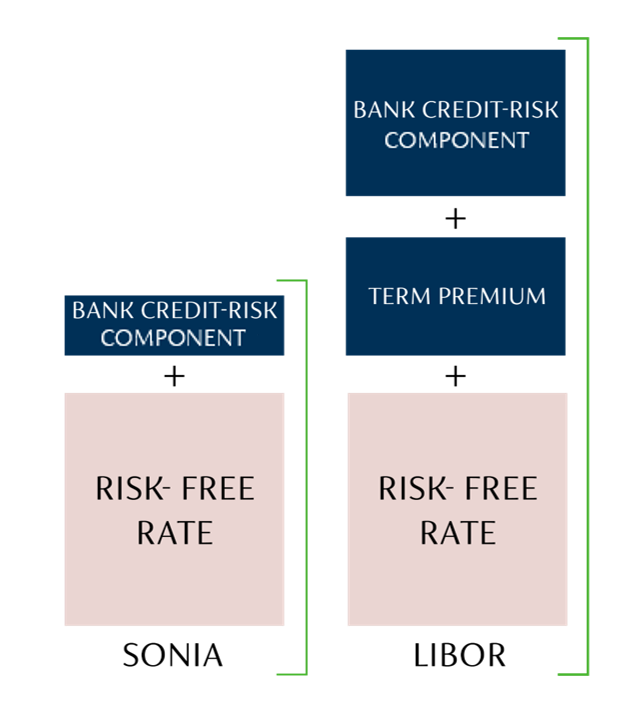

Robust alternative benchmark rates have been established to replace LIBOR (London Interbank Offered Rate) in the UK, such as SONIA (Sterling Overnight Index Average)

GBP LIBOR

- Based on panel bank submissions, lacks an active underlying market

- Forward-looking term rate

- Is set daily for a range of lending periods e.g. 1 week, 3 months, 6 months, 1 year

- Interest is known at the start of the period

- Exposes the borrower to movements in bank credit risk

SONIA

- Deep and liquid underlying market, not based on panel bank submissions

- Overnight rate

- Published daily reflecting economic reality, but needs to be aggregated for use over the lending period

- Interest is not known at the start of the period

- Nearly risk-free rate, minimising term bank credit or liquidity premium

SONIA is not a like-for-like alternative to LIBOR

![]()

SONIA is published every London business day by the Bank of England.

![]()

SONIA is an overnight rate, measured each day over the interest period to produce a final interest rate at the end.

![]()

It is a (nearly) risk free rate, because it minimises any term bank credit risk or liquidity premium.

![]()

SONIA is fully transaction based and more in line with the economic reality of inter bank lending.

![]()

-

Does SONIA move with Bank Rate changes?

Does SONIA move with Bank Rate changes?

Does SONIA move with Bank Rate changes?

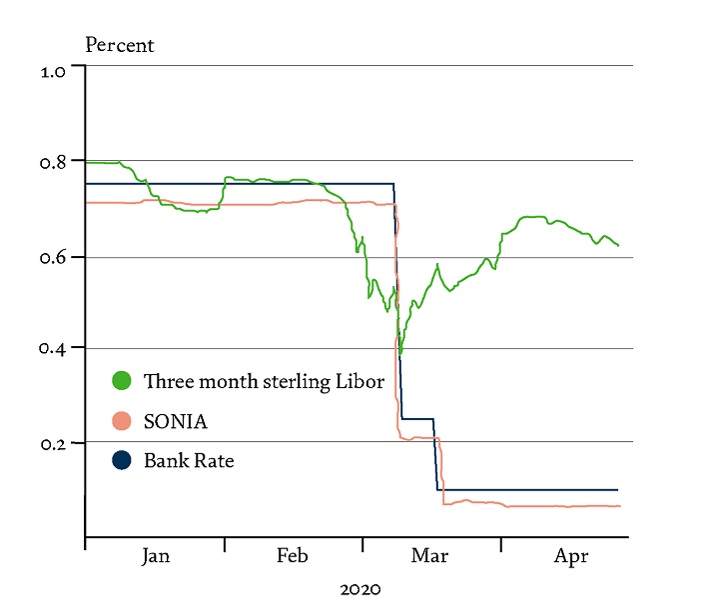

SONIA has shown less volatility as a daily rate

![]()

SONIA has closely tracked the Bank Rate.

![]()

This was demonstrated in March 2020 when policy rates fell in response to COVID 19 disruption. However, LIBOR rates increased.

![]()

Households and businesses paying interest based on SONIA or Bank Rate would have benefitted directly from central bank policy action.

MOVEMENTS IN SHORT-TERM STERLING INTEREST RATES SINCE JANUARY 2020

![]()

Sources: Bank of England, Bloomberg Finance L.P. and Bank calculations

-

What is SONIA compounded in arrears?

What is SONIA compounded in arrears?

What is SONIA compounded in arrears?

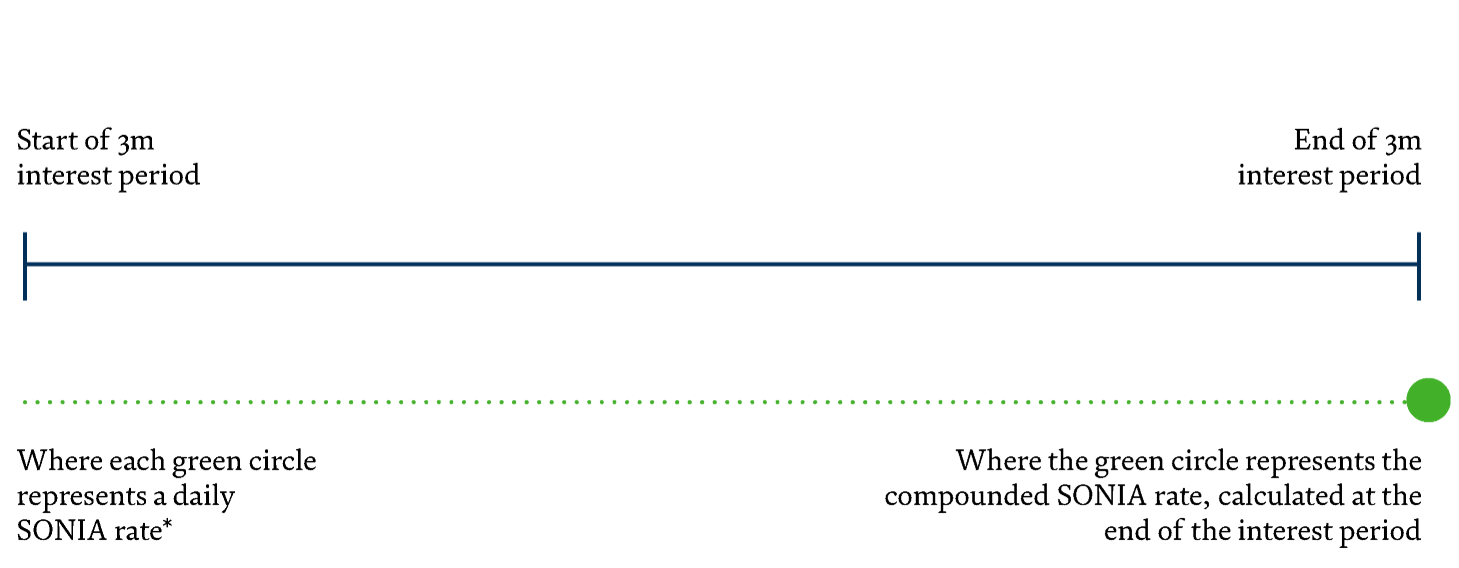

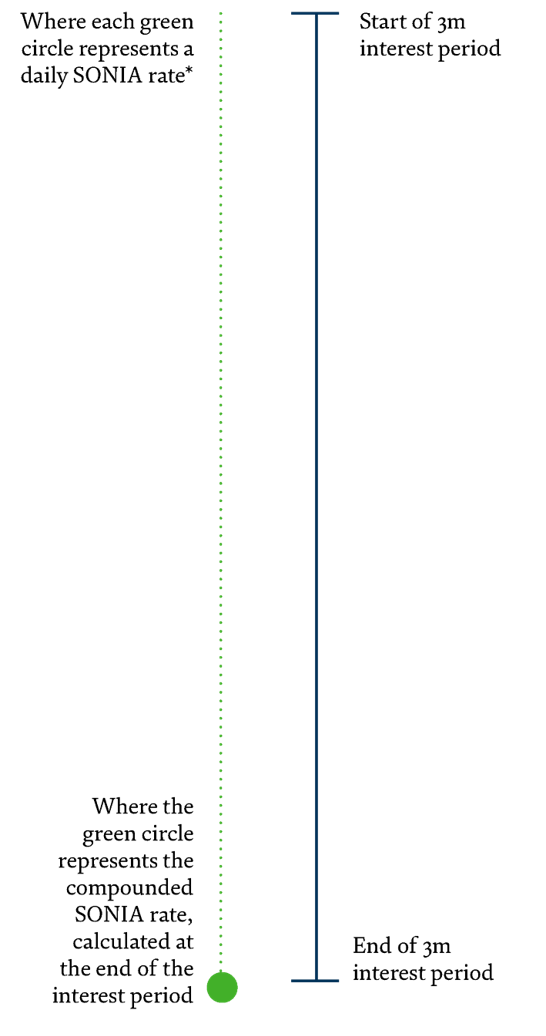

The most established way to use SONIA to calculate interest in contracts is called ‘compounded in arrears’

![]()

![]()

This involves taking the SONIA rate for each business day over the interest period to calculate the applicable rate.

*On weekends and bank holidays, the SONIA rate is held constant from the last working day.

-

What are the benefits of compounded SONIA?

What are the benefits of compounded SONIA?

Benefits of compounded SONIA

Compounded SONIA is extremely robust

![]()

Overnight SONIA is underpinned by *£60bn worth of daily transactions, reported to the Bank of England.

Taking this rate every business day means there is a very large volume of transactions underpinning the final interest rate (e.g. £60bn x number of business days in interest period = significant volume).

![]()

Calculating interest on a compounded basis reduces the contribution of ‘one off’ volatility in interest rates, that may occur due to unusual supply and demand factors affecting a benchmark rate on a particular day.

Conventions for compounded SONIA

- When using compounded SONIA, the interest rate payable is aggregated over the interest period and finalised at the end. The eventual rate becomes increasingly certain as the end of each period approaches and most of the SONIA observations are known.

- But we know firms need a period of certainty over their payments to operate smoothly. The market has therefore developed conventions to provide time after the last SONIA observation for the final interest to be calculated & verified before it needs to be paid.

- For example, the period for calculating interest may start (typically) five days before the actual interest period begins, so it finishes that number of days before the interest is due.

*Q2 2020, as reported in Bank of England Interactive Statistical Database

-

What is a Credit Adjustment Spread?

What is a Credit Adjustment Spread?

What is a credit adjustment spread?

Ensuring fair value as the market transitions away from LIBOR

Ensuring fair value as the market transitions away from LIBOR

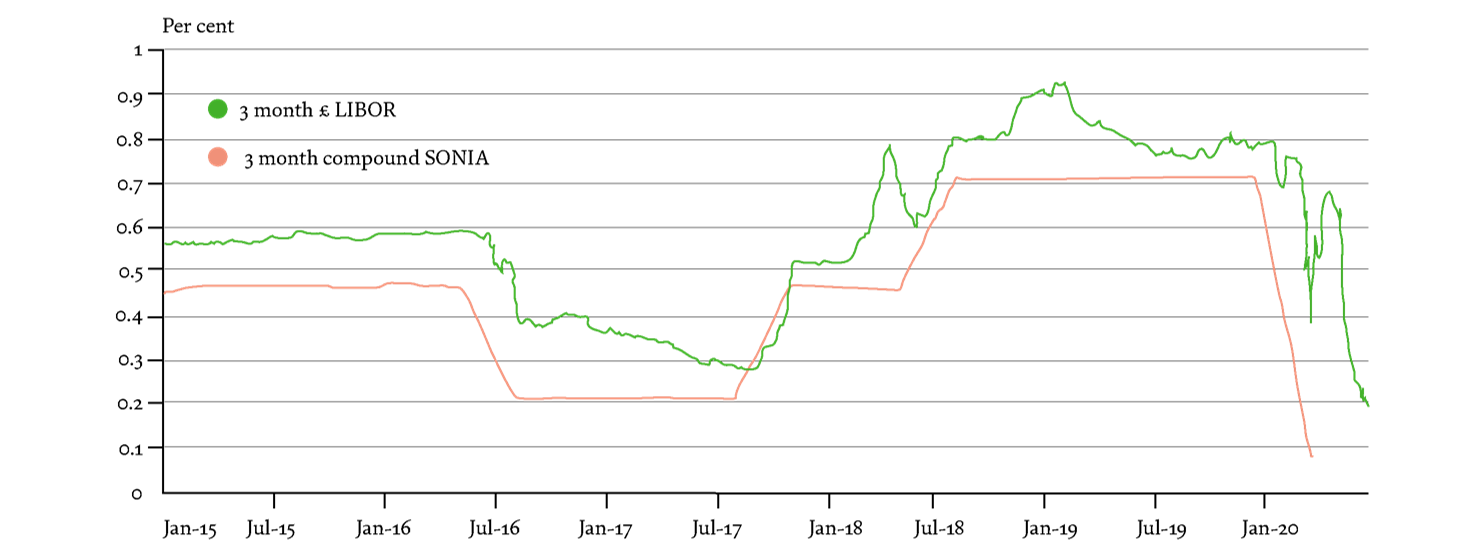

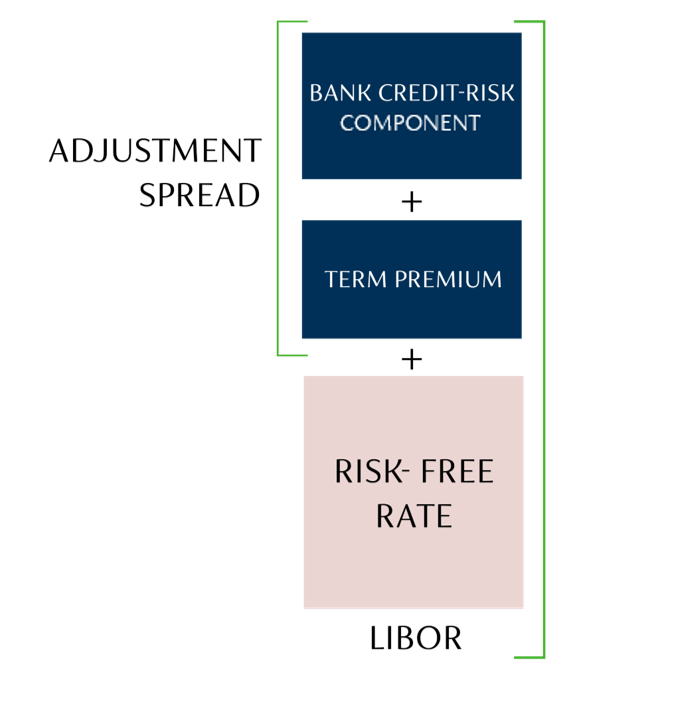

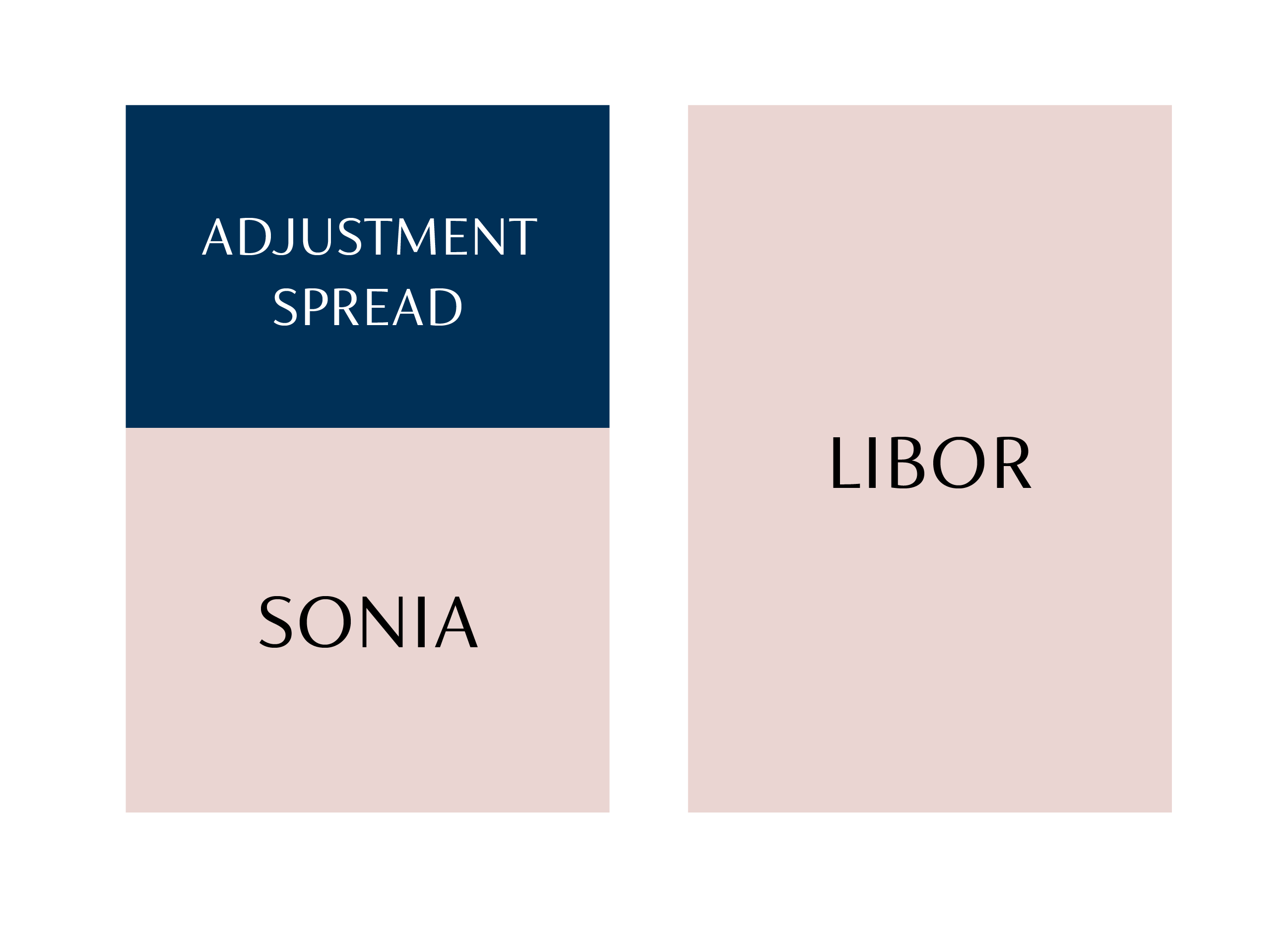

- LIBOR includes a credit element to reflect the cost and risk to banks of lending over a term period.

- As SONIA is an overnight rate, the risk of lending is lower, therefore the SONIA rate is typically lower than LIBOR.

- To ensure a fair conversion of existing contracts, a small adjustment is needed to account for this difference.

3m compounded SONIA and 3m £ LIBOR

![]()

Source: Bank of England and Bloomberg L.P

![]()

-

Fair treatment of customers when replacing LIBOR

Fair treatment of customers when replacing LIBOR

What is a Credit Adjustment Spread?

TREATING CUSTOMERS FAIRLY

It’s important that customers are treated fairly when transitioning away from LIBOR

An overarching concern for the FCA is whether firms have taken reasonable steps to treat their customers fairly. A lot of work has been done to build market consensus on how to calculate a fair replacement to LIBOR.The FCA has made clear that:

- The discontinuation of LIBOR should not be used to move customers with continuing contracts to higher rates.

- They do not expect banks currently receiving interest payments based on LIBOR to give up the adjustment spread.

![]()

![]()

In the derivatives market, the work to fairly replace LIBOR has been led by ISDA (International Swaps and Derivatives Association).

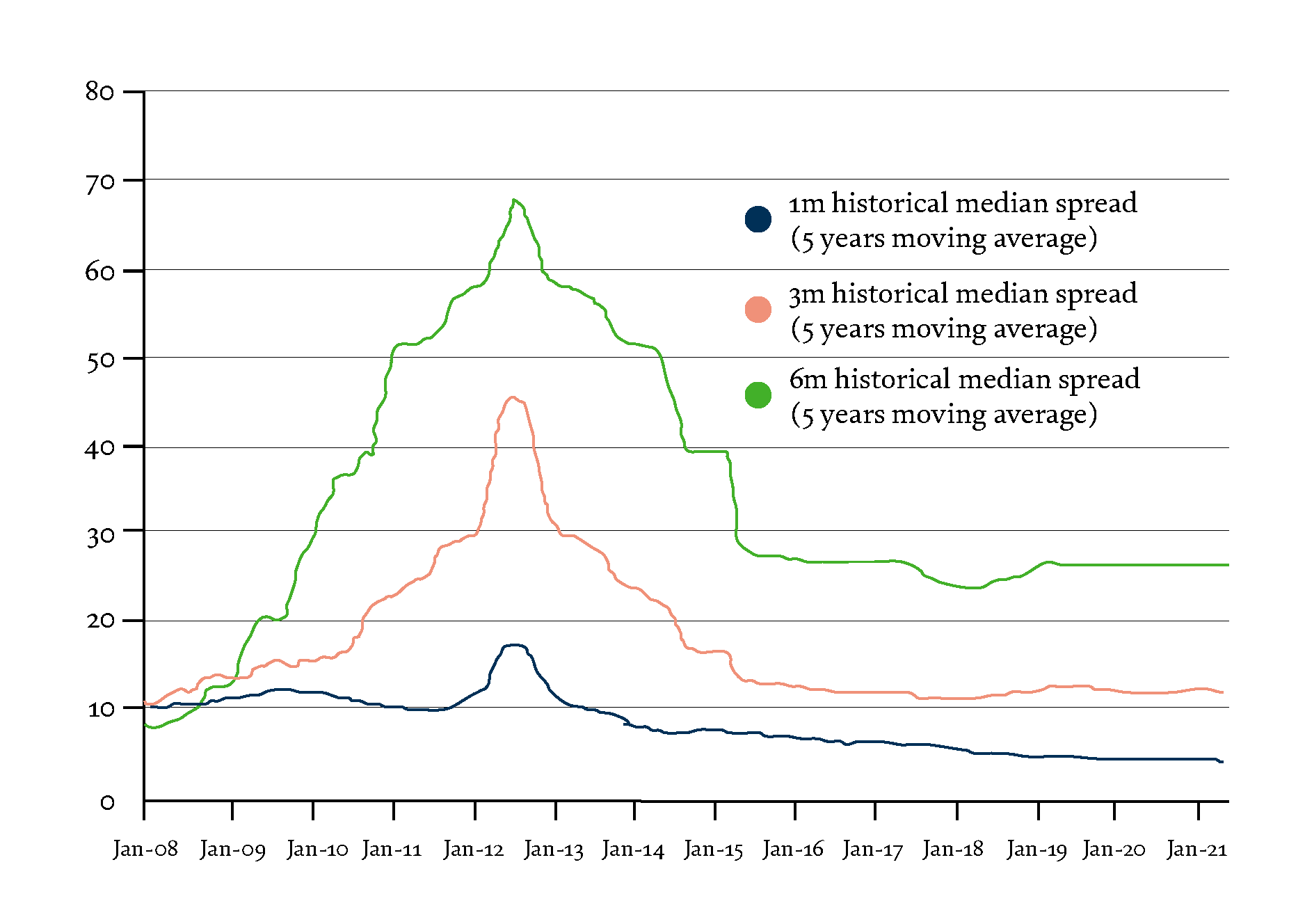

- Following a number of consultations, the preferred methodology is to use the median difference (spread) between LIBOR and SONIA calculated over the previous 5 year period.

- This methodology will therefore be used to apply an adjustment spread to SONIA when loans are transitioned from LIBOR at the first roll over after LIBOR ceases (expected to cease at the end of 2021).

Links to further information:

How could the Budget affect property?

CIO Update – Managing risk amid periods of uncertainty