2) The US remains exceptional

Investors have been wrestling with the question of whether the US can remain ‘exceptional’, having outperformed global equities by 160% since 2015 (as at October 2025).

The weight of rising government debt, sizable fiscal deficits, a weaker dollar and America First foreign policy have been cited as examples of waning US influence.

But for us, America’s structural advantages endure, and we believe it will remain exceptional for the foreseeable future.

US still ahead of peers

Two of the most important factors that influence investment returns are economic growth, and how easily that growth translates into company earnings.

Economic expansion depends on demographics and productivity, while its influence on company earnings centres on institutional depth – the rule of law, enforcement of contracts, stable policymaking and corporate governance.

Looking at the US through this lens, its demographic outlook, productivity potential and institutional depth continue to outpace peers. UN figures show the projected US age dependency ratio – the number of people below and above working age as a percentage of the working population – to be 75% by 2100 (the lower the percentage the better for the economy). That’s compared to over 80% for Germany and 114% for China.

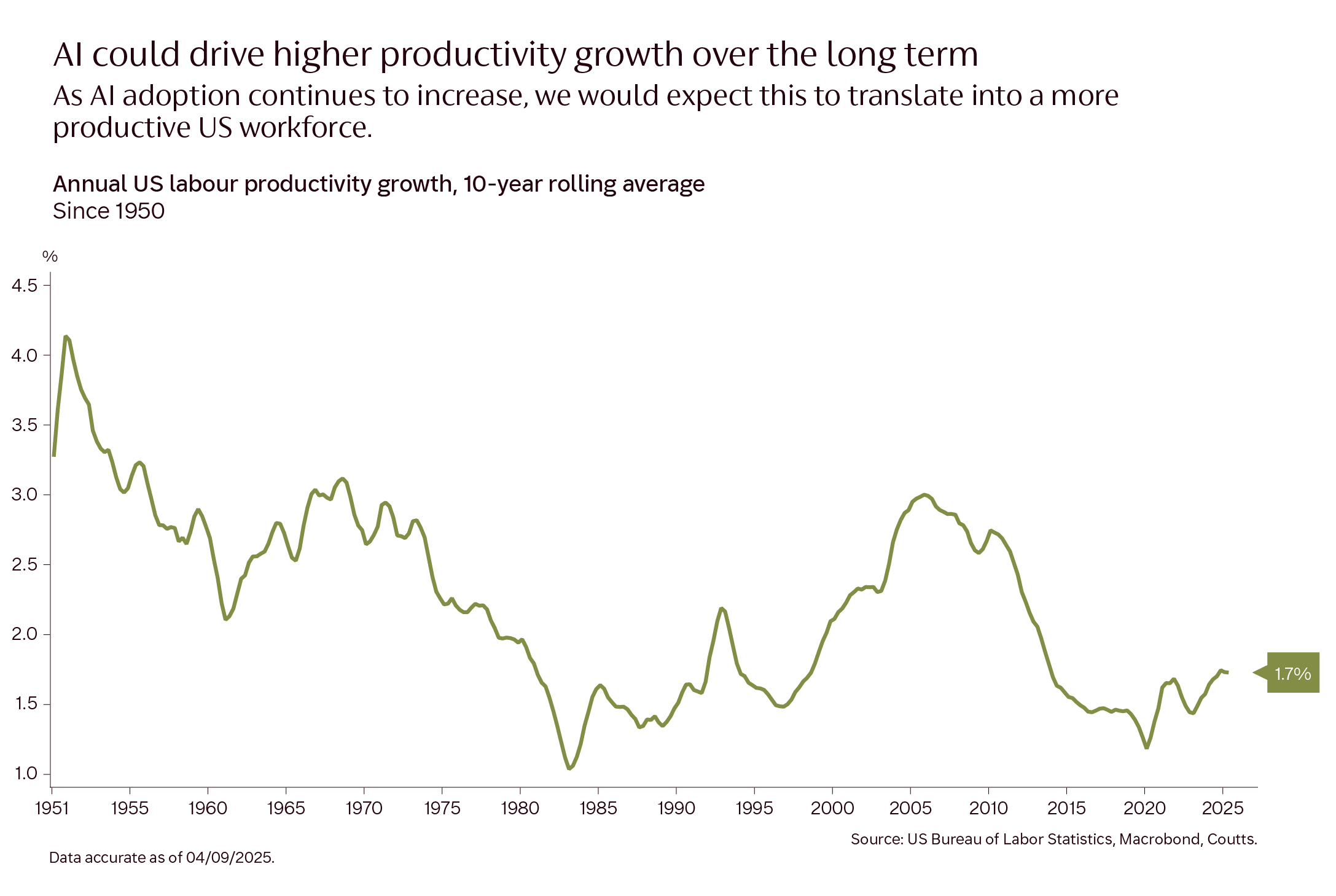

The OECD, meanwhile, found that US labour productivity (GDP per hour worked) increased by 1.6% in 2023, while the average across all its countries was 0.6%.

US productivity growth is also likely to accelerate faster than other developed markets because of the country’s flexible labour markets and strong track record of adopting new technology.

3) Private markets reach pivotal moment

Private market investing has undergone a remarkable transformation. At the end of last year, global assets under management had tripled in size over the previous decade to $15.5 trillion, according to the Financial Conduct Authority.

This growth reflects strong demand from long-term investors seeking diversification beyond traditional public markets. Private market assets include private equity – ownership in non-public companies – and private credit, where asset managers or private funds provide direct loans to businesses outside public markets.

What sets private markets apart from traditional asset classes is their distinct underlying economic exposures, business models and economic sensitivities. As access improves, these opportunities could broaden the investible universe and enhance portfolio outcomes when combined with public market strategies.

The opportunities are striking, with far more private companies in the world than publicly traded enterprises. In the US alone, 99% of middle market businesses are privately owned, according to Ares Management.

Innovation paves the way

Historically, for individuals seeking to maintain and grow their wealth, private markets presented challenges. Extended capital deployment timelines, illiquidity and large minimum investments all presented barriers to entry.

But today, innovation is reshaping the landscape.

So-called evergreen funds, which ease some of the challenges, are increasing in popularity. They allow investors to access a fully diversified portfolio of private assets significantly faster than more traditional, ‘closed-end’ structures. Under normal market conditions, an investor can withdraw part of their investment in a few months, and these funds tend to have lower minimum investment sizes than their traditional counterparts.

For eligible investors, the message is clear: private equity and private credit should not be viewed as replacements for traditional investing, but as complementary components of a well-constructed portfolio. They represent a strategic evolution in wealth management.