For equity markets to perform well, the most important factor is reliable economic growth and its translation into growing company earnings. While economic growth is driven by demographics and productivity, the reliability of earnings centres on institutional depth (such as the rule of law, reliable enforcement of contracts, stable policymaking, and corporate governance).

Although the US may have partially stepped back from its 20th century role as the world’s policeman, it’s still setting geopolitical trends. US President Donald Trump has altered the rules-based international order, and in place of historic norms, the US, China, and Russia have honed their individual spheres of influence.

This is an uneasy dynamic, and over the long run could have implications for other contested territories.

For example, there are rising concerns that China – witnessing the actions of the US and Russia – could seek to exert further influence on Taiwan. For erstwhile resilient markets, this could be a bitter pill to swallow. Taiwan’s semiconductor expertise is critical to the global technology industry, with the potential to disrupt earnings in the technology sector if challenged.

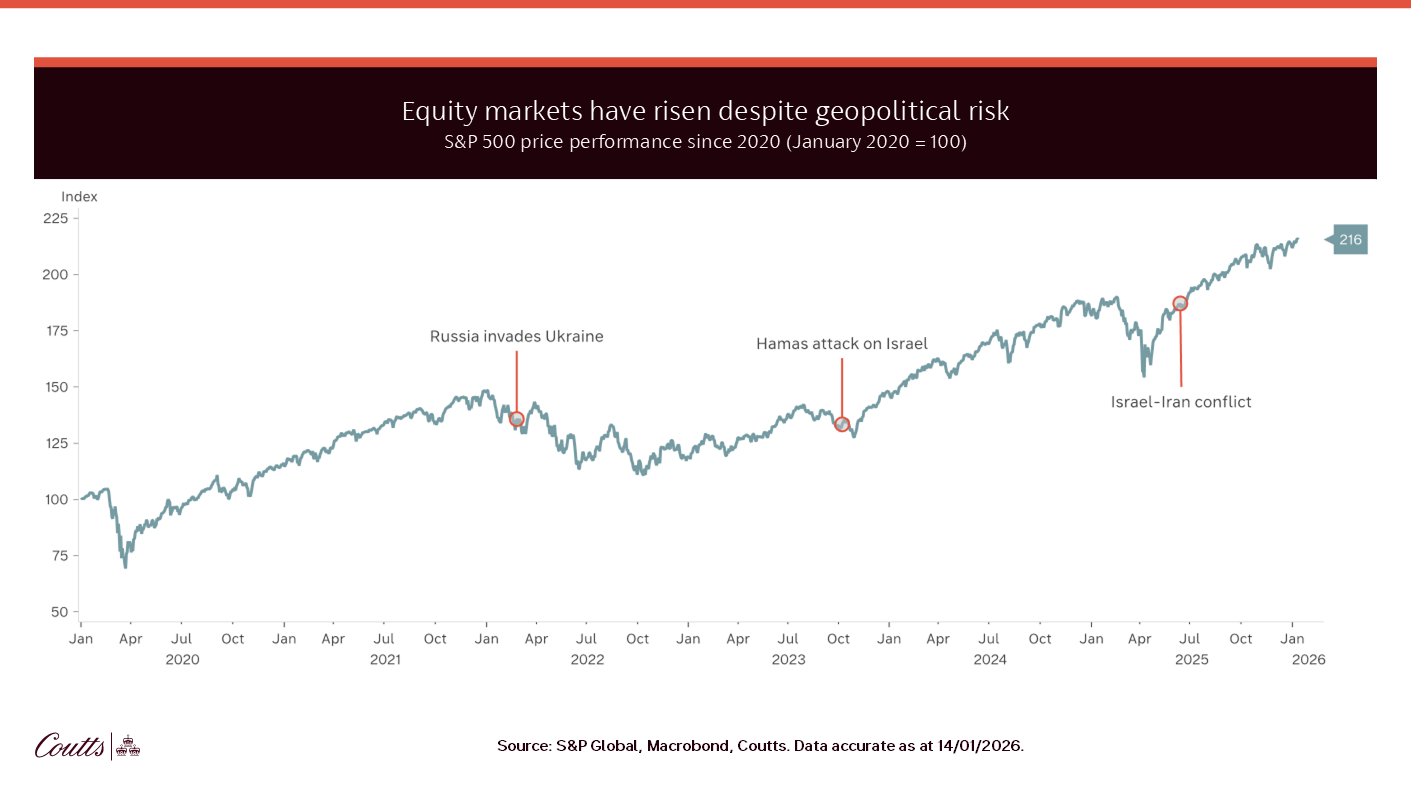

But while this particular issue represents a meaningful threat to equity markets, it’s also a threat which has existed for many years. We could have written these same sentences about Taiwan during Trump’s first term in office, and markets have risen much higher since then. While this doesn’t make the threat a comfortable one, it does highlight that reacting too early to a potential geopolitical flashpoint can lead to missing out on investment returns.