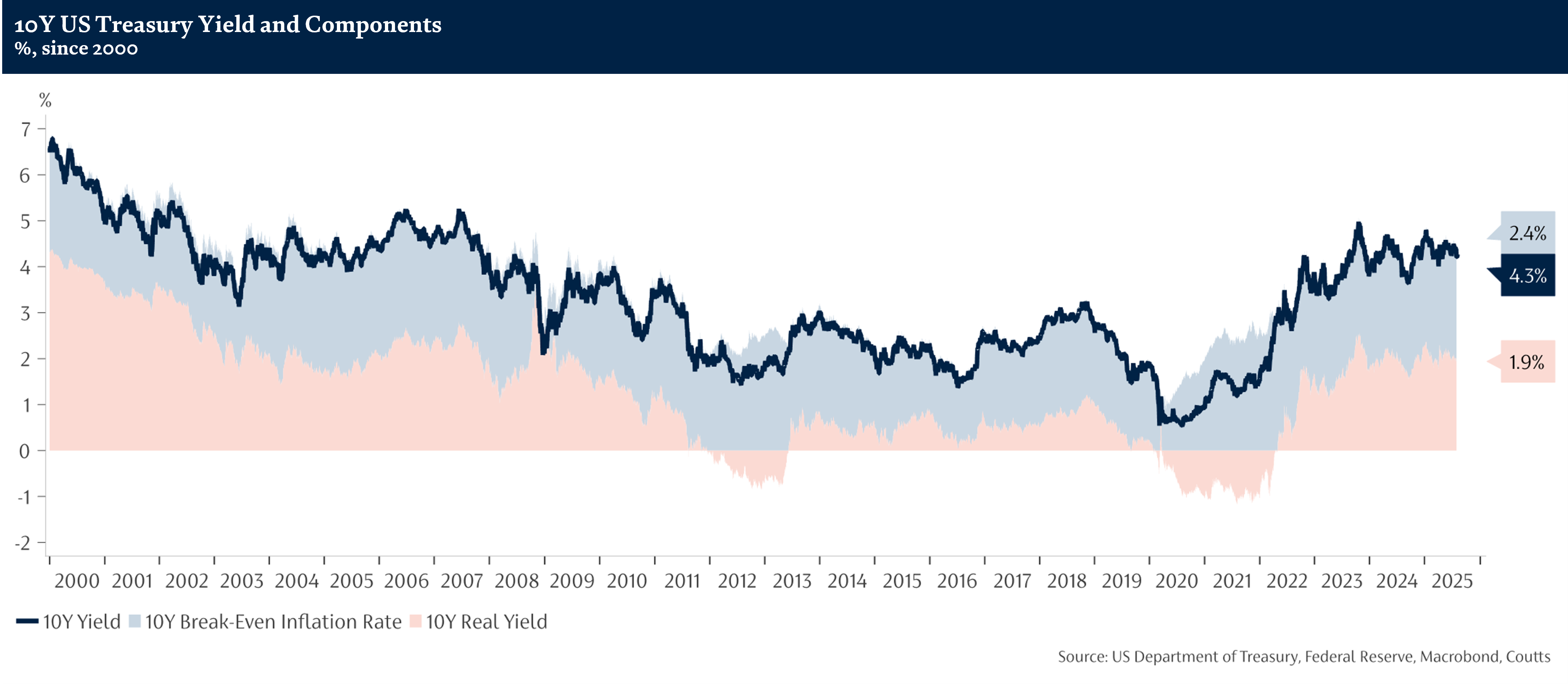

It’s been a volatile year for US government bonds for several reasons. Firstly, growing national debt has raised concerns over the viability of the Treasury market, as President Trump announced plans to increase spending without raising sufficient taxes. This resulted in ratings agency Moody’s downgrading Treasuries from Aaa to Aa1 in May – the last of the major ratings agencies to do so.

Secondly, tariffs have played a role in disrupting the US Federal Reserve’s (Fed) roadmap for cutting interest rates this year. Coming into 2025, markets expected the Fed to continue its rate cutting cycle. However, the unknown impact of tariffs halted the central bank from reducing its base rate until further economic data gave evidence that inflation was still trending down, towards the Fed’s 2% target.

Inflation has ticked up slightly in recent months and the US economy has remained resilient, justifying the Fed’s decision to pause any interest rate changes. However, much of the drivers for this uptick in inflation are likely transitory, and tariffs have not caused the economy to overheat just yet. Therefore, Fed Chair Jerome Powell recently signalled that the central bank would likely resume its rate cutting cycle in September.

Hope of a resumption to interest rate cuts caused yields for both corporate and government bonds to fall, but the recent optimism in the corporate sector sparked increased demand for the riskier option, which narrowed credit spreads.