Stock markets have been in rude health recently, repeatedly reaching all-time highs. Investors have benefitted from ongoing economic growth, the artificial intelligence revolution and expectations of lower interest rates.

Yet as the old Persian adage reminds us: ‘This too shall pass.’ With inflation proving persistent and speculation about a potential ‘AI bubble’, some may ask whether it’s time to retreat from equities.

In our view, it is not.

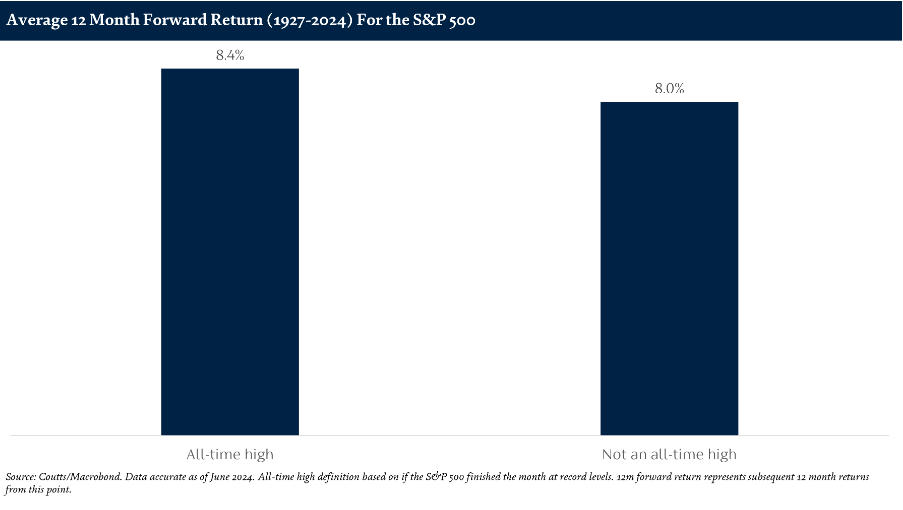

Although all-time highs can feel uncomfortable, they are far from rare. Our research, drawing on data since 1927, shows markets have hit unprecedented peaks around 20% of the time. During that period, returns in the year following an all-time high have outperformed those following other market levels (see chart below).

In an environment where economic and earnings growth are positive, investors should perhaps consider such times to be more ‘normal’ than they initially feel.

Past performance should not be taken as a guide to future performance. The value of investments and the income from them can fall as well as rise and you may not get back what you put in.