Investing

Post-peak interest rate environment

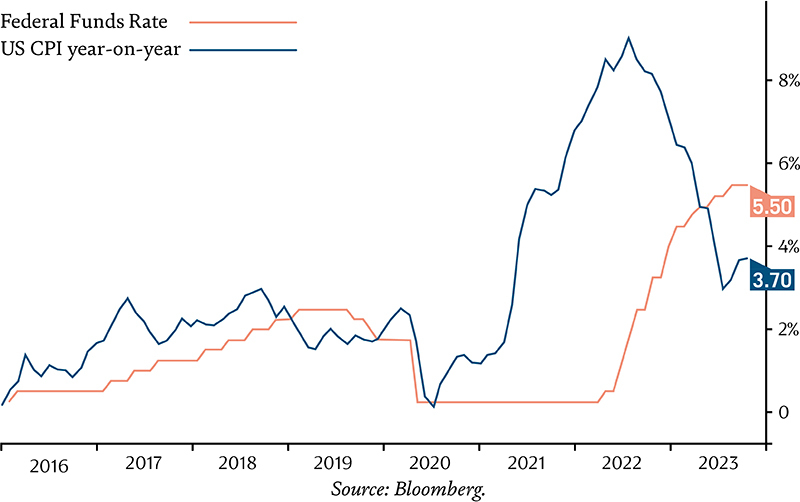

Some central banks paused raising interest rates towards the end of 2023, confirming our view that they might have finally peaked. Before we look at what the world might look like when we’re beyond this peak, let’s look at why central banks raised rates in the first place.