Property

London Prime Property Index Q1 2023

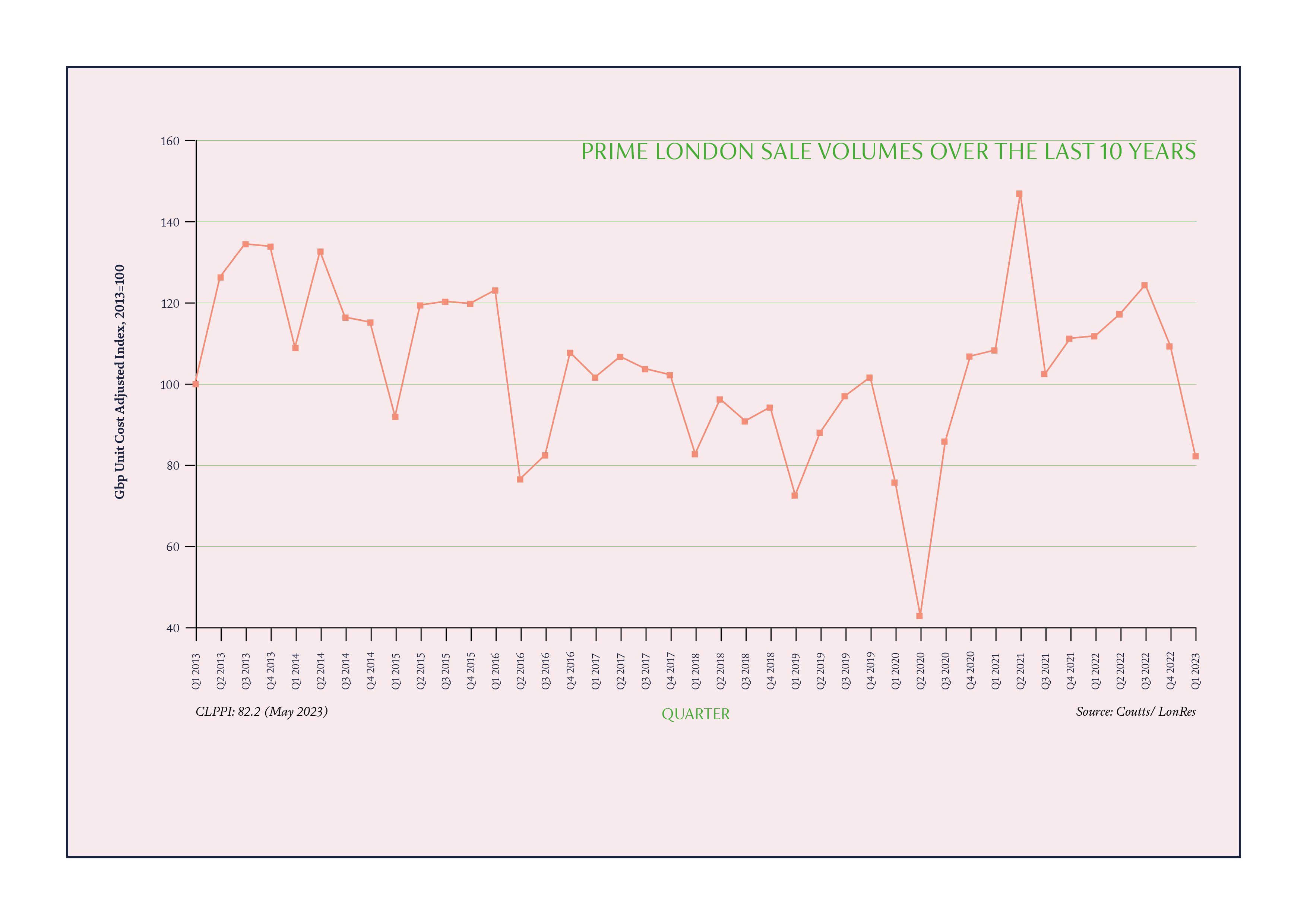

What happened in Q1 and where might the market go from here? Here’s our latest insight on London’s prime property sector.

What happened in Q1 and where might the market go from here? Here’s our latest insight on London’s prime property sector.

Your home or property may be repossessed if you do not keep up repayments on your mortgage. Changes in the exchange rate may increase the sterling equivalent of your debt (multi-currency debt only).

Over-18s only. Terms and conditions apply. You may not be eligible for all Coutts mortgage solutions. Security may be required. Product fees may apply.