A time for moderation

Markets traded around three themes in August: inflation, timing of central bank stimulus reduction and more moderate growth

3 min read

SHARE

Most Popular

-

Ukraine invasion: Keeping our clients informed | Coutts

15 Mar 20221 min

-

Coutts and charitable giving in the Covid era

02 Dec 20214 min

Become A Client

When you become a client of Coutts, you will be part of an exclusive network.

Global economic growth has slowed a little, but stock markets continue to rise, and we see the expansion continuing into next year.

The Office for National Statistics reported that the UK economy grew by 4.8% in the second quarter of 2021, following the easing of lockdown restrictions. This was down to increases in retail trade, food services and hotel accommodation, construction and production output.

However, July data noted a significant slow-down as the economy grew just 0.1%, while inflation plateaued in the UK and US – now at 3.2% and 5.4% respectively.

In terms of markets, most major exchanges finished the month up, except China. The S&P 500 was up around 3% compared to the previous month. While the FTSE 100 ended the month +1.2%, its best monthly performance since April 2021.

Predictably, causes for concern remain, centred on fears of a new wave of Covid-19 as well as signals of a reduction in economic stimulus (tapering) from the European Central Bank (ECB) and US Federal Reserve.

Overall, the MSCI World Index of global equities rose 2.7% in August in local currency terms, while US 10-year Treasury bonds returned -0.2%.

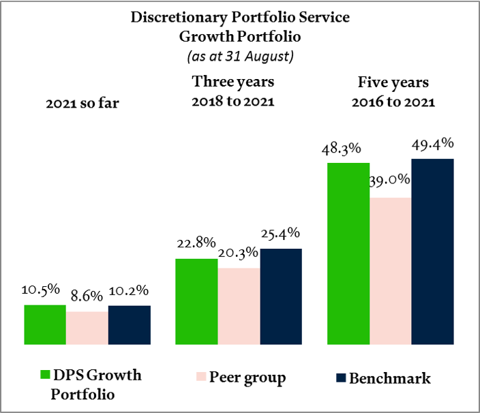

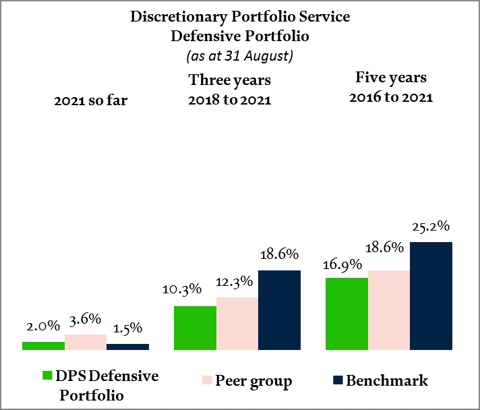

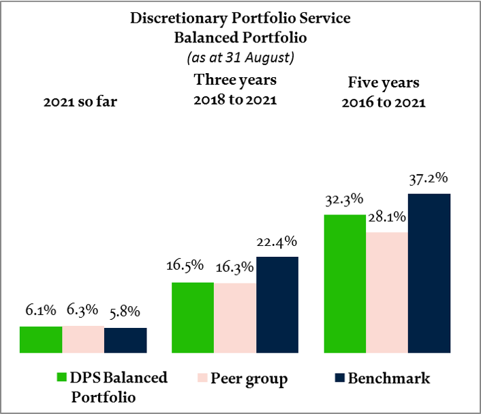

Healthy returns for the month

Global equities performed well in August and our exposure contributed to positive performance for all our portfolios and especially the more equity-focussed Balanced and Growth portfolios. Defensive portfolios recorded a positive return - as well driven by equities as bonds consolidated after July’s price rise.

Cumulative returns calculated on sterling basis, including fees, charges and income to 31 August 2021. These data are based on composite performance, individual portfolio monthly returns are asset-weighted based on their respective asset values at the beginning of the month. Peer group returns provided by Asset Risk Consultants (ARC); end-August data represents ARC estimate. Benchmarks represent a static mix of equities and bonds in proportions relevant to each strategy. Past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can go down as well as up and you may not recover the amount of your original investment. Sources: Coutts & Co, ARC. September 2021.

“The expansion is not over. Growth is likely to be robust into 2022.”

Sven Balzer, Head of Investment Strategy, Coutts

Economic growth moderates

We have started to see slower economic growth – but it is still growth. There are a number of factors behind the slow-down: The rise of Delta variant cases in China led to a partial closure of the country’s third largest container port, resulting in further supply chain bottlenecks across the globe, though these aren’t expected to persist longterm.

Also, consumer sentiment has fallen in the US, partly due to the rise in Delta variant cases as well as concerns about higher inflation. However, it’s important to remember that more moderate economic growth was inevitable as activity had reached very high levels earlier this year.

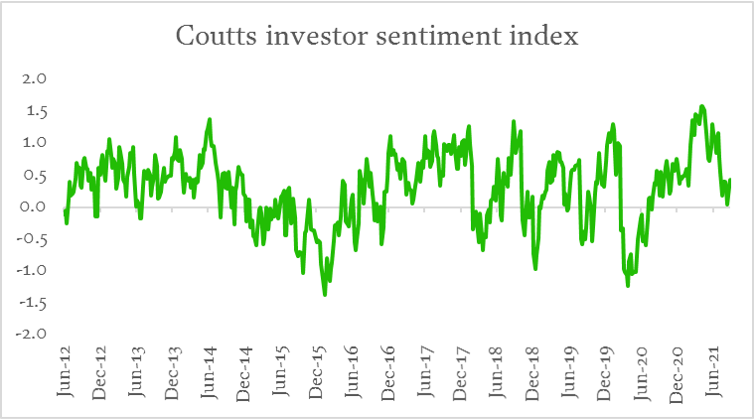

Echoing this, the market mood has changed as well. Our own Coutts Investor Sentiment Index came down to 0.05 from its high reading of 1.6 in March 2021, showing a greater sense of caution. Now in neutral territory, it reflects the recent uncertainty about economic activity, the future of central banks’ bond-buying programmes designed to stimulate the economy, and recent Chinese policy actions designed to clamp down on monopolies.

But as Sven Balzer, Head of Investment Strategy, Coutts, points out, “The expansion is not over. Growth is likely to be robust into 2022. Financial conditions are easy, and consumers have surplus cash and wealth gains.”

US Federal Reserve hints at stimulus withdrawal

The annual Jackson Hole symposium brought together – virtually again this year – central bankers and economists from around the world. Fed chair Jay Powell indicated that tapering would begin this year, but also confirmed that there is “much ground to cover” before the central bank would consider rate hikes.

He continued to emphasise his belief that recent inflation rises were temporary, and that the economy remained far from reaching the Fed’s maximum employment goal.

It was this softer, more nuanced message that gave risk assets a positive boost at the end of the month.

Headlines were also dominated by the unfolding humanitarian crisis in Afghanistan. The crisis itself was further evidence of the profound geopolitical changes underway, though there was no impact on US and global markets.

Outlook for inflation

Inflation levels in the UK increased to 3.2% in August. One of the reasons for this steep rise is mathematical – the current rate compares to an unusually low rate year-on-year, partly because of the August 2020 ‘Eat Out to Help Out’ discounts. Because that scheme ran for a limited time, the Office for National Statistics stressed that its impact was likely temporary. Inflation is likely to remain elevated until the end of 2021, because of things like a rise in utility prices from October, before settling back down from Q2 2022. Meanwhile, over in the US, price rises have steadied and inflation returned 5.3% year-on-year in August.

Share