January jitters don’t change our positive outlook

Hopes were high at the start of 2021 as investors looked towards the economic recovery

4 min read

SHARE

Most Popular

-

Ukraine invasion: Keeping our clients informed | Coutts

15 Mar 20221 min

-

Coutts and charitable giving in the Covid era

02 Dec 20214 min

Become A Client

When you become a client of Coutts, you will be part of an exclusive network.

Markets started 2021 on a relatively positive note. The optimistic mood that characterised November and December extended into January as vaccination programmes gathered pace around the world, with cyclical sectors and markets performing well.

However, the impact of new strains of the coronavirus and issues over supply and distribution of vaccines in some countries raised the possibility of longer lockdown periods. As a result, and despite strong returns in the initial weeks, investor confidence took a dent and January saw many markets down over the calendar month, with the MSCI World Index returning -1.4%. Unusually, government bonds were also negative – the Barclays UK Treasury Index returning -1.8%. (Data quoted in sterling terms, including income, source: Reuters/Eikon Datastream.)

RECOVERY ON TRACK DESPITE MARKET NERVES

While markets may have been jittery in January, our analysis of underlying economic data supports a global economic recovery in 2021. Some market volatility is to be expected. In fact, as we pointed out in our 2021 Outlook, overly optimistic market sentiment after a strong year-end rally – the MSCI World Index rose by around 15% between the end of October and 8 January – left share prices vulnerable to profit taking and a consolidation. (Data quoted in sterling terms, including income, source: Reuters/Eikon Datastream.)

Added to this, unusual activity around GameStop and some – otherwise unattractive – stocks sent confusing signals that added to investor inclinations to take profits. You can read a more detailed analysis of the phenonmenon here, but the bottom line is that we don’t think these events have undermined the investment case for mainstream equities supported by good fundamentals.

“While markets may have been jittery in January, our analysis of underlying economic data supports a global economic recovery in 2021.”

PORTFOLIOS POSITIONED FOR RECOVERY

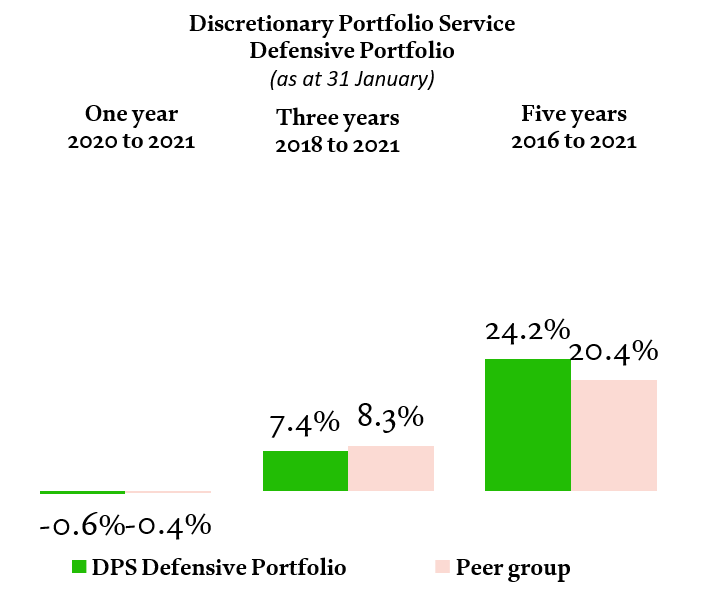

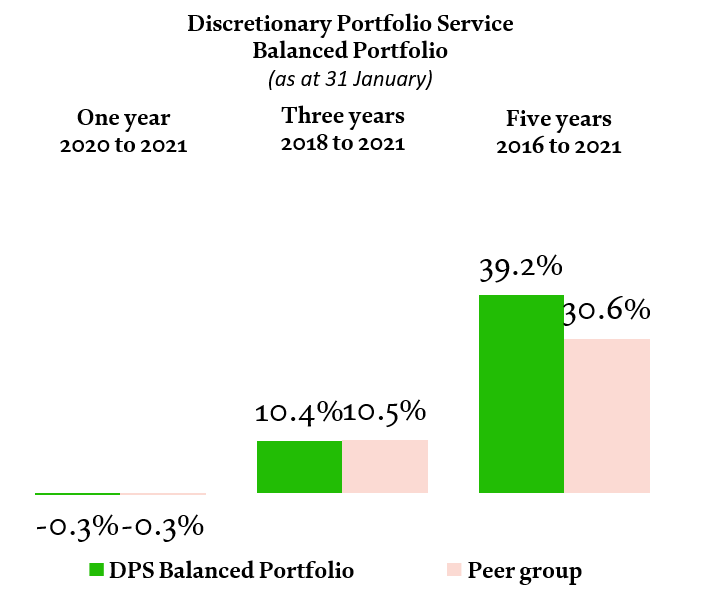

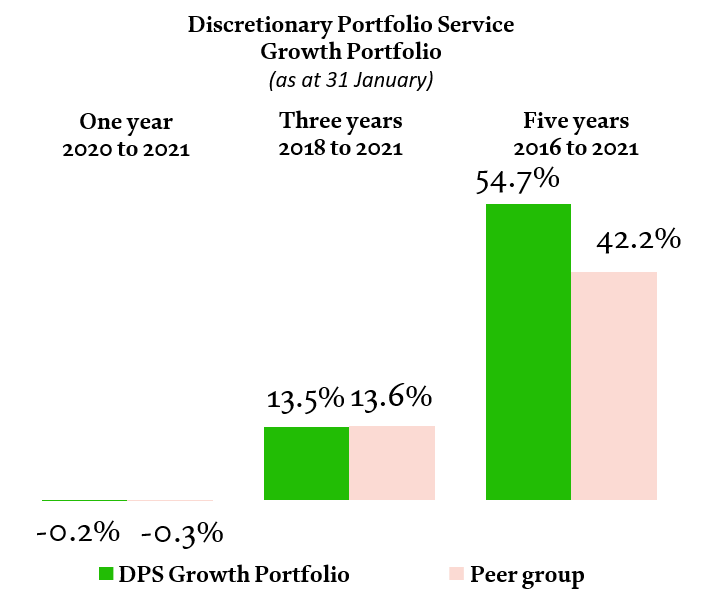

As a result of these various impulses, at the end of January returns for Coutts funds and portfolios were largely flat. After seeing a solid return of around 1% over most of the month, the average balanced portfolio ended up more or less flat on -0.3%.

Longer-term returns remain strongly positive and ahead of peers. The average balanced portfolio has returned over 39% over five years, substantially outpacing inflation and adding to the overall value of our clients’ wealth, compared to a 30.6% average return from our peer group.

Cumulative returns calculated on sterling basis, including fees, charges and income to 31 January 2021. These data are based on composite performance, individual portfolio monthly returns are asset-weighted based on their respective asset values at the beginning of the month. Peer group returns provided by Asset Risk Consultants (ARC); end-January data represents ARC estimate. Past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can go down as well as up and you may not recover the amount of your original investment. Sources: Coutts & Co, ARC. February 2021

This underlines the importance of maintaining a long-term view based on your overall wealth. Although cash can have a role to play in your financial life – to meet day-to-day expenses and for important purchases – investing remains one of the best ways to maintain the long-term value of your wealth for yourself and your family.

Of course, past performance is not a guide to future returns. The value of investments, and the income you get from, can go down as well as up and you may not get back the amount you originally invested.

Emerging markets go from strength to strength

Our allocations to emerging markets helped to offset falling prices elsewhere, as this was one of the few areas to show a positive return in January. Emerging markets have been one of the strongest performers in our portfolios over the past three months, with MSCI Emerging Markets Index returning 5.8% in November, 4.9% in December and 2.6% in January. (Data quoted in sterling terms, income reinvested, source: Reuters/Eikon Datastream).

In particular, emerging Asian countries that export to China are continuing to benefit from the country’s recovery. The Chinese economy has rebounded strongly from the pandemic, growing by 6.5% in the fourth quarter of 2020, up from 4.9% in the previous three months, according to official data.

Dollar weakness has also encouraged investors into emerging market assets. For governments and companies based in those regions with dollar-denominated debt, a weaker dollar reduces the costs of servicing those debts and helps improve investor sentiment towards these countries. The US government’s stimulus plans and general loose financial conditions should also benefit Asian exports and boost demand for emerging market assets.

We’re maintaining our overweight allocation to emerging market equities, after adding to our holdings from some of our US equity exposure in October. During this time, emerging market equities have strongly outperformed other regions, providing a boost to returns.

BIDEN STEPS UP TO THE WORLD STAGE

In the US, Joe Biden was inaugurated as President and the Democrats won the run-off elections in Georgia, giving the party control of both houses of Congress. While markets were initially encouraged by the possibility of the quick passage of a generous stimulus package, the reassertion of political realities later in the month made it clear that getting a the package through the house would be a more laborious process, contributing to the wobble in investor confidence.

BREXIT DEAL BOLSTERS STERLING

The Brexit deal before Christmas boosted the value of sterling, while the dovish outlook from the Federal Reserve depressed the dollar and problems with the EU’s vaccine programme weighed on the euro.

At the same time, UK equities had a marginally better month than peers – MSCI UK fell by -0.7%, compared to -1% for the S&P 500, for example. This pattern is a reversal of what we usually see, as a stronger pound typically raises headwinds for large-cap UK stocks. The situation reflects the UK stock market’s bias towards more economically sensitive areas of the economy, including energy and financials, that did well early in the month.

We’ve also added to our holdings in gilts in our sterling-dominated portfolios and funds, reducing exposure to US Treasuries and taking some profit from investment grade corporate debt. After the Democratic blue wave and the potential for stronger stimulus and inflationary pressure, we believe the outlook for government bonds is better for the UK than the US.

long-term returns

|

31 December 2015 to 31 December 2016 |

31 December 2016 to 31 December 2017 |

31 December 2017 to 31 December 2018 |

31 December 2018 to 31 December 2019 |

31 December 2019 to 31 December 2020 |

MSCI World Index (sterling) |

28.2% |

11.8% |

-3.0% |

22.7% |

12.3% |

MSCI UK Index |

19.2% |

11.7% |

-8.8% |

16.4% |

-13.2% |

MSCI Emerging Markets (sterling) |

32.6% |

25.4% |

-9.3% |

13.8% |

14.7% |

S&P 500 |

32.7% |

10.6% |

1.0% |

25.7% |

14.1% |

Coutts Defensive Portfolio |

8.4% |

5.8% |

-3.7% |

8.3% |

3.5% |

Defensive strategy benchmark |

12.8% |

5.7% |

-1.6% |

11.1% |

7.7% |

Coutts Balanced Portfolio |

12.2% |

9.1% |

-5.1% |

12.4% |

4.4% |

Balanced strategy benchmark |

17.6% |

7.9% |

-2.9% |

14.1% |

6.5% |

Coutts Growth Portfolio |

16.2% |

12.1% |

-6.5% |

16.9% |

4.7% |

Growth strategy benchmark |

21.8% |

10.4% |

-4.2% |

17.0% |

4.9% |

Past performance should not be taken as a guide to future returns. Returns calculated on sterling basis, including fees, charges and income. Benchmarks represent a static mix of equities and bonds in proportions relevant to each strategy. Source: Reuters Eikon/Datastream,Coutts & Co, February 2021.

Share