Green shoots of recovery starting to bloom

Encouraging signs that the economic recovery is gathering momentum boosted investment markets in April

3 min read

SHARE

Most Popular

-

Ukraine invasion: Keeping our clients informed | Coutts

15 Mar 20221 min

-

Coutts and charitable giving in the Covid era

02 Dec 20214 min

Become A Client

When you become a client of Coutts, you will be part of an exclusive network.

After a rocky start to the year, the more settled markets we saw in March continued in April, with shares and bonds both broadly positive. Overall, the MSCI World Index of global equities rose 4.0% in April, while UK government bonds returned 0.5%.

US and UK equities were among the strongest performers, but it was European equities that hit an all-time high during the month owing to growing optimism about the vaccination programme. In contrast, the mood in Japan was more negative as it started to become clear that the lockdowns could last for longer than expected.

Economic data released during April provided validation for the market’s optimism. This included strong retail sales and falling unemployment benefit claims in the US, and a pick-up in inflation in Europe. The Bank of England also revised upwards its prediction for economic growth for 2021, and now expects the strongest period of economic expansion since World War 2.

two good months in a row

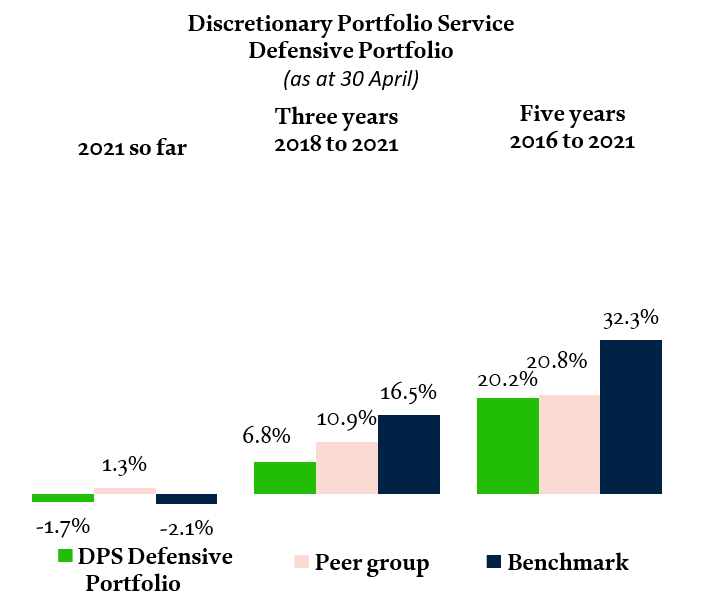

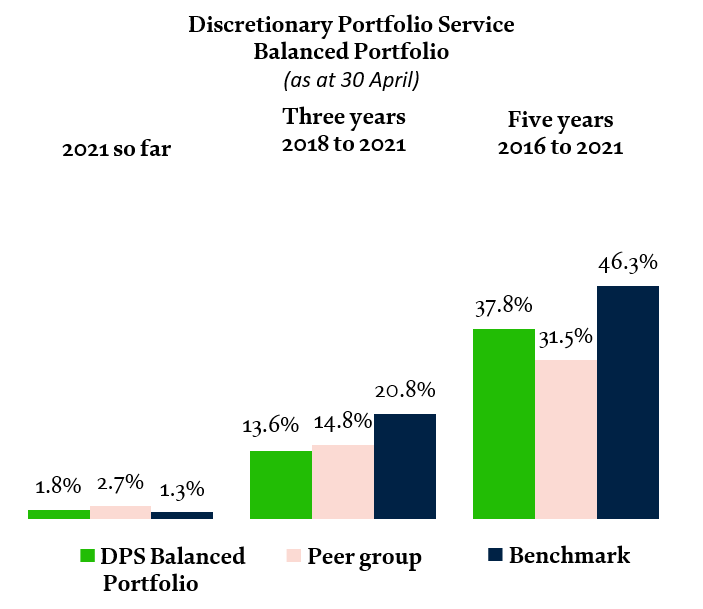

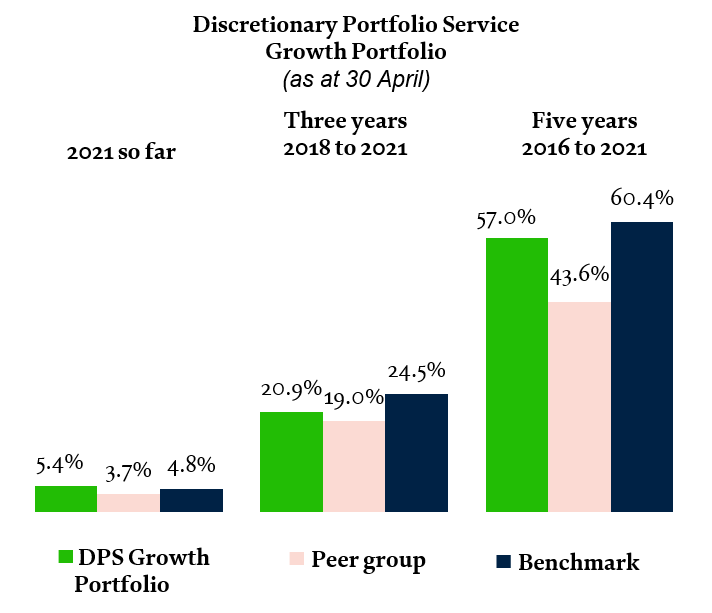

The Coutts portfolios delivered positive returns for the second consecutive month in April. The more equity-focused growth strategies benefited most from the strength in global stock markets. The average returns of balanced and growth portfolios are now positive and ahead of benchmark for the year so far.

Positive returns from government bonds were helpful for defensive strategies as yields fell back slightly (meaning prices rose) in April, and defensive portfolios continue to outperform their benchmark. The impact of rising yields (falling prices) in the early part of the year means defensive strategies still have some ground to make up in the year to date.

In the longer term, all strategies are robust, providing returns ahead of inflation.

Cumulative returns calculated on sterling basis, including fees, charges and income to 30 April 2021. These data are based on composite performance, individual portfolio monthly returns are asset-weighted based on their respective asset values at the beginning of the month. Peer group returns provided by Asset Risk Consultants (ARC); end-April data represents ARC estimate. Benchmarks represent a static mix of equities and bonds in proportions relevant to each strategy. Past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can go down as well as up and you may not recover the amount of your original investment. Sources: Coutts & Co, ARC. May 2021.

These figures show a limited snapshot of performance. For more context, please refer to the long-term performance numbers below.

During the month we closed our US banks portfolio theme, banking profits following a strong period of performance. We initiated the position during the worst days of the pandemic when banks were under threat from rising bad debts, so valuations were attractive. Our analysis suggests most of the gains have been realised and we’re keen to get the money working elsewhere. In the short term, we’ve folded this money back in to our broad US equity exposure.

We also changed the focus of our holdings in Europe and Japan. In Europe, we’re investing in more economically sensitive companies, which should do well as the recovery gains pace on the Continent. In the meantime, we’ve moved away from growth-oriented companies in Japan and taken a more broad-based approach.

Looking forward to a self-sustaining recovery

The economic recovery is progressively shifting from one supported by the government and central banks to one based on rising economic activity.

In April, investors began considering the impact of a reduction in the level of monetary support that we’ve seen since the crisis began last year. This could – however very unlikely in the short term – include raising interest rates, but first and foremost reducing central bank bond repurchasing programmes (otherwise known as quantitative tightening).

This topic could increasingly be on investors’ minds as the year progresses. We think governments are unlikely to threaten the recovery in the short term with any hasty moves, but we are monitoring the shift and the potential impact on portfolios. Any changes would have an impact on inflation and bond yields, and so the topic could become a temporary headwind for performance at some point this year, even if central banks take no action.

Supply chains at full stretch

There’s increasing evidence that companies are paying more for the resources they use, and that supply chains are becoming stretched as the economy comes roaring back to life. This raises the risk that companies may not realise the full potential of their production capacity while costs are rising, which could hit profits for some businesses.

The ISM Manufacturing Prices Paid indices for services and manufacturing, for example, which measure changing prices paid by companies for the products and services they receive, have been rising. Commentary from companies has also highlighted rising input costs. At the same time, the Suez Canal blockage at the end of March led to weeks of disruption for European manufacturers depending on components from elsewhere, demonstrating the impact of even small disruptions to the supply chain.

As stocks are forward-looking investments, we could see these concerns reflected in share prices if they continue to grow. This supports a more cautious tactical approach to investing in equities over the coming months as the world readjusts to life in the wake of the coronavirus pandemic.

This is not an unusual development for financial markets in a post-recession environment. After the initial boom, a flatter period often follows as economies adjust to rising outputs. In the longer term we continue to see positive returns for equities into 2022.

long-term PERFORMAnCE

31 March 2016 to 31 March 2017 |

31 March 2017 to 31 March 2018 |

31 March 2018 to 31 March 2019 |

31 March 2019 to 31 March 2020 |

31 March 2020 to 31 March 2021 |

|

MSCI World (local currency, including income) |

31.9% |

1.3% |

12.0% |

-5.8% |

38.4% |

Coutts Defensive Portfolio |

9.2% |

1.8% |

1.7% |

-1.6% |

6.6% |

Peer group - ARC Cautious PCI |

7.1% |

0.7% |

1.7% |

-2.3% |

11.5% |

Composite benchmark |

11.2% |

1.8% |

5.0% |

3.3% |

6.4% |

Coutts Balanced Portfolio |

15.3% |

2.7% |

2.8% |

-4.6% |

16.0% |

Peer group - ARC Balanced Asset PCI |

11.5% |

0.8% |

3.0% |

-5.4% |

18.5% |

Composite benchmark |

17.3% |

1.9% |

6.2% |

-1.5% |

14.6% |

Coutts Growth Portfolio |

21.4% |

3.3% |

4.1% |

-9.0% |

28.1% |

Peer group - ARC Steady Growth PCI |

15.8% |

1.3% |

4.8% |

-7.7% |

24.8% |

Composite benchmark |

23.0% |

2.1% |

7.5% |

-6.3% |

23.1% |

Returns calculated on a sterling basis, including fees, charges and income. Discretionary portfolio calculated based on composite performance, individual portfolio monthly returns are asset-weighted based on their respective asset values at the beginning of the month. Peer group returns provided by Asset Risk Consultants (ARC); end-March 2021 data represents ARC estimate. Past performance should not be taken as a guide to future performance. The value of investments, and the income you get from them, can go down as well as up and you may not recover the amount of your original investment. Sources: Coutts & Co, ARC, Investment Association, Thomson Reuters Eikon/Datastream. March 2021.

Share