Monthly Update | Can markets maintain momentum?

Stock markets were up in January but can the positive mood last given the uncertain political and economic outlook?

4 min read

SHARE

Contents

Following disappointing returns in 2018 markets got off to a brighter start in 2019, with solid gains over the first few weeks of the year.

Recovering from the hangover

We’re still cautiously positive on the outlook for investors, but we’ve reduced risk in portfolios in response to heightened market volatility and signs of slower global economic growth.

Global stock markets were upbeat in January, with the seasonal return of liquidity boosted by investors looking for bargains after the December falls. The MSCI All Country World Index returned 7.2%, translating to 4.5% for sterling-based investors due to a stronger pound through the month. Gilt yields were more or less flat, hovering around the 1.3 mark.

While we have reduced risk in our portfolios, we remain cautiously positive on the outlook for investors. Our overall allocation to equities is now very slightly underweight as we increased our allocation to cash in December. This means we are ready to capture any opportunities that appear in the coming months, while also cushioning portfolios against any further short-term volatility.

Dovish Fed soothes markets

Fed luminaries take dovish stance, but we believe data will still be the driver of US rates in 2019.

The US Federal Reserve (Fed) kept interest rates on hold at a range of 2.25% to 2.50% at its latest meeting on 30 January. However, Chairman Jay Powell surprised investors by doubling down on comments earlier in the month that the US central bank would take a “patient” approach to further interest rate rises.

In his comments he cited tepid markets and slowing global growth as reasons to be cautious, saying that the case for rate rises had “weakened somewhat”.

This marks a significant shift in tone from the more hawkish note struck by the bank towards the end of 2018. Fear around interest rates rising too fast is widely credited as one of the key reasons behind December’s market correction. Higher US interest rates will increase borrowing costs which could reduce company profits, dampen consumer demand and fuel a stronger dollar – which has caused problems for emerging market economies.

Investors are clearly relieved by the Fed’s new-found caution, but we don’t think further rises are off the agenda. The language has changed but it’s clear that economic data will still guide the Fed’s hand. Markets are not currently pricing in any rises in 2019 but there may be more to come over the year.

“While we have reduced risk in our portfolios, we remain cautiously positive on the outlook for investors. After increasing our allocation to cash in December, we are also ready to capture any opportunities presented by market volatility in the coming months.”

China attempts to add buoyancy

We think that stimulus from the Chinese government is likely to stem the decline in economic data, but it remains to be seen whether positive movement can be reignited.

The latest official data showed that China’s economy grew by 6.6% in 2018 – the slowest rate since 1990. Although in line with analyst expectations, the slowdown prompted fears about the global economy – China accounts for a third of the world’s growth and plays a particularly important role in emerging markets.

The country has introduced a series of fiscal and monetary measures to stimulate growth in the economy. They include injecting money into the banking system, more infrastructure spending and tax cuts.

China has been managing a transition from a manufacturing-based export economy to a more service-based domestic economy over the past few years, so some bumps in the road are to be expected. How the government navigates the situation is likely to have a significant impact on markets. In the meantime we are holding a modest positive position in China, which will benefit should the government’s measures bear fruit.

Markets cling to hints of trade negotiation progress

We have always believed that the US and China will find solutions to their trade dispute and recent talks have brought this closer, soothing market jitters.

Negotiators from the US and China ended their first round of talks since calling a truce over their trade dispute. Both sides are working towards reaching an agreement before 1 March, after which the US could raise its tariffs significantly if the issues aren’t resolved.

Our view remains that these two economies have more to lose than gain from a trade war. We believe both sides will reach a compromise.

We like Japan, but…

We’ve scaled back our position in Japan as we see a stronger yen and slowing global growth reducing the potential for gains.

The Japanese economy performed well in 2017 but growth was lacklustre in 2018 and ran out of steam in the final quarter. Whilst we continue to have confidence in the long-term outlook – due in part to corporate profitability and reform – the slower global growth in general is currently a headwind for the country. Returns from Japanese equities also tend to fall towards the end of the business cycle as the yen rises, boosted by its status as a safe haven currency.

Our overall position in Japan is neutral, rather than negative, and so we still see potential for gains, but we’ve taken some of our exposure and added it to our cash holdings for now, ready to deploy as new opportunities appear.

Brexit bugbears

While Brexit uncertainty casts a shadow over the UK, we have a positive view on large-cap UK equities that are more closely connected with the global economy.

A tumultuous month in Parliament saw MPs reject the UK government’s agreement with the European Union, then support a government-backed proposal to renegotiate the ‘back stop’ arrangement for the Irish border.

Investors seem largely inured to Brexit turmoil, being more concerned with US interest rates and the US/China trade dispute. Sterling strengthened in January as the Brexit news unfolded more or less in line with market expectations, and the stronger currency hurt UK large-caps. But as the pound settled later in the month, UK equities came back with the MSCI UK Index returning 3.7% over the course of January.

While this highlights the vulnerability of UK equities to currency moves, we have a generally positive view based on attractive valuations and income streams. Brexit uncertainty may be casting a shadow over the UK but the fate of large-cap UK equities is more entwined with the global economy, which remains robust.

When investing, past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can go down as well as up, and you may not recover the amount of your original investment.

-

Market Performance

Chapter 01

Market Performance

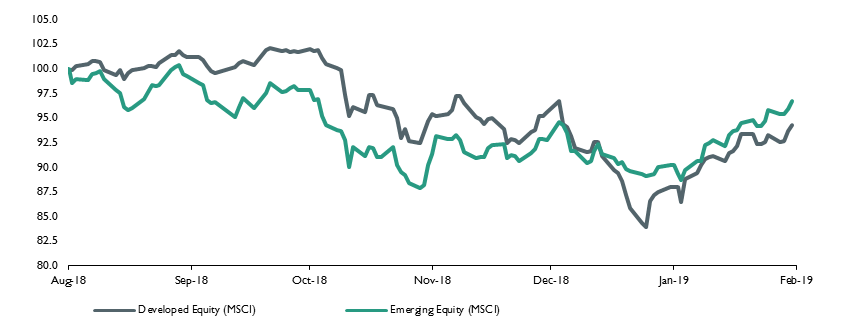

![]()

Source: Datastream, MSCI, rebased to 100

Important: This graph shows a very isolated period of past performance. For further context of historic performance over the last five years, please click on the “Equity Markets Performance” heading above. As always, past performance should not be taken as a guide to future performance.

Source: Datastream, MSCI, rebased to 100Performance (%tr*, local)

12 Month performance to end December As of: 31-Jan-19 Current -1M -3M YTD 2018 2017 2016 2015 2014 Developed Equity (MSCI) 1,544.3 7.3 0.1 19.0 -6.9 19.1 9.6 2.6 10.4 MSCI UK 2,015 3.7 -1.6 5.7 -8.8 11.8 19.2 -2.2 0.5 MSCI UK large cap 992 3.0 -1.9 6.0 -7.7 11.5 22.8 -3.9 -0.8 S&P 500 2,704 8.0 0.3 25.8 -4.4 21.8 12.0 1.4 13.7 Nasdaq Composite 7,282 9.8 0.0 38.3 -2.8 29.6 8.9 7.0 14.7 DJ EuroStoxx 348.5 6.3 -0.9 6.0 -12.1 13.4 5.0 11.1 5.0 Nikkei 225 20,773 3.8 -5.0 13.0 -10.3 21.3 2.4 11.0 9.0 Hang Seng 27,942 8.1 12.0 36.7 -10.5 41.3 4.3 -3.9 5.5 Emerging Equity (MSCI) 57,232 7.2 7.7 26.7 -9.7 31.0 10.1 -5.4 5.6 BRIC (MSCI) 674.8 8.8 10.1 39.3 -8.9 40.6 8.2 -5.3 5.8 Source: Datastream, all returns in local currency; *tr=total return, including reinvested dividends. Inflation & Interest Rates Current Inflation (%) Interest Rate Forecasts (%) Rate Announcement Current April July Next Date United States 1.9 2.50 2.50 2.50 20-Mar United Kingdom 2.1 0.75 0.75 0.75 21-Mar Eurozone 1.4 0.00 0.00 0.00 07-Mar Japan 0.3 -0.10 -0.10 -0.10 26-Mar Performance (%tr, local)

12 month performance to end December As of 31-Jan-19 10-year yield*

-1M

-3M

YTD

2018 2017 2016 2015 2014 US Treasury index 2.64 0.3 3.1 -0.8 -1.2 0.1 -1.4 -1.6 2.6 UK gilts index 1.23 0.7 1.2 -2.8 -2.0 -1.5 7.9 -2.3 10.7 Eurozone govt bond index 0.10 2.6 4.0 -5.0 -9.5 2.3 -1.4 3.4 -1.6 US investment grade index 3.91 2.2 2.8 -2.8 -6.4 1.6 1.8 -5.6 2.2 US high yield index 6.90 4.0 -0.4 -3.6 -8.3 1.1 12.0 -10.1 -4.3 Emerging market index 10.05 6.4 -0.8 -12.0 -22.6 6.8 9.4 20.6 -8.2 Source: Barclays indices; Datastream; *current yield on benchmark 10-year Treasury, gilt and bund respectively Performance (%, Dollar) 12 month performance to end December As Of:31-Jan-19 Current -1M -3M YTD 2018 2017 2016 2015 2014 Commodity index (TR) 168.4 5.4 -2.4 -4.8 -11.3 1.7 11.8 -24.7 -17.0 Brent oil price (spot) 62.5 23.5 -16.5 13.1 -24.2 20.9 51.6 -33.5 -50.3 Gold bullion (spot, per ounce) 1323 3.2 8.8 14.3 -1.7 12.6 9.0 -10.5 -1.8 Industrial metals (TR) 246.0 8.0 4.4 12.5 -19.5 29.4 19.9 -26.9 -6.9 Source: Datastream

SHARE

Key Takeaways

Markets rebounded in January, gaining back some of the ground lost in December. Dovish signals from the Fed and positive noises on US/China trade talks boosted investor confidence, while liquidity returned to markets after the holiday period.

Global economic growth remains positive which we think will continue to support equities. We have reduced our investment in equities recently, maintaining a neutral exposure, and positioned portfolios so we are poised to take advantage of opportunities.

About Coutts investments

With unstinting focus on client objectives and capital preservation, Coutts Investments provide high-touch investment expertise that centres on diversified solutions and a service-led approach to portfolio management.

Discover more about Coutts investmentsRelated stories

Most Popular

-

CIO Update – Managing risk amid periods of uncertainty | Insights | Coutts

10 Oct 20253 min Whether financial markets ever face a downturn again in the future isn’t a matter of ‘if’ but ‘when’. While it’s impossible to predict the exact moment, managing risk in our portfolios in advance of future events is fundamental to our investment philosophy and process. Read our latest CIO update.

Whether financial markets ever face a downturn again in the future isn’t a matter of ‘if’ but ‘when’. While it’s impossible to predict the exact moment, managing risk in our portfolios in advance of future events is fundamental to our investment philosophy and process. Read our latest CIO update.

-

How could the Budget affect your inheritance planning? | Insights | Coutts

08 Oct 20254 min Coutts Wealth Structuring Manager Irene Wolstenholme and Head of Specialists Greg Kyle-Langley have assessed the current tax landscape and what might change in the upcoming Autumn Budget. They share their view on key considerations when planning for the future.

Coutts Wealth Structuring Manager Irene Wolstenholme and Head of Specialists Greg Kyle-Langley have assessed the current tax landscape and what might change in the upcoming Autumn Budget. They share their view on key considerations when planning for the future.

When you become a client of Coutts, you will be part of an exclusive network.