Monthly Update | Happy Christmas for markets?

Stock markets sparkle, the economy lights up and central banks show good will. But could the ghosts of political risk, past, present and future still pay markets a visit?

3 min read

SHARE

Contents

Recent developments suggest it really could be a case of happy holidays for investors.

There are signs that global economic growth, which has been slowing for over a year, is picking up. At Coutts we believe the business cycle may be bottoming out, with recent data showing a modest rise in growth. In light of this, we recently took a slightly more pro-growth stance in our client portfolios and funds by buying more European stocks.

Meanwhile, central banks have shown strong support for their economies and there have been tentative steps forward in the US-China trade talks and Brexit progress.

This has all buoyed stock markets. In the US alone, the S&P 500, Nasdaq Composite and Dow Jones Industrial Average indices all rallied to record highs in November. The MSCI All Country World Index returned 2.9% in local currency terms in November – 22.9% year-to-date – and most major stock markets ended the month in positive territory. As investors took on more risk, government bond yields rose (prices fell).

But without wanting to spoil the Christmas party, Monique Wong, Executive Director, Portfolio Management, says Coutts remains conscious of the political risks still lurking in the background.

“Markets have performed very well so far in 2019, despite talk of a potential recession which now looks less likely than it did earlier in the year,” she says. “This is obviously good news for investors, but we need to keep an eye on potential pitfalls.

“Geopolitical risk remains the Grinch that could steal Christmas. The trade talks rumble on and have made progress but a positive outcome is still not guaranteed, while election-related uncertainty hangs over markets in the UK.”

Global economy perks up

Signs that the global economy may not be slowing as quickly as previously thought include the UK avoiding recession. After falling by 0.2% in the second quarter of 2019, the economy grew by 0.3% in the third quarter, avoiding the dictionary definition of a recession – two quarterly contractions in a row.

Meanwhile, GDP in Germany and Japan also avoided economic falls, growing by 0.1% over the same period compared with the previous three months.

The US economy remains the real bright spot, with official figures showing that it grew at an annualised rate of 2.1% in the three months to the end of September, higher than expected.

The world’s largest economy is practically bursting with Christmas cheer. Unemployment remains at a record low, inflation appears contained and consumer and government spending are still buoyant.

“Markets have performed very well so far in 2019, despite talk of a potential recession which now looks less likely than it did earlier in the year.”

Our Positioning

At Coutts we continue to have a small preference for equities and other risk assets over more defensive investments within our portfolios and funds. As a result, throughout this year we have tilted our investments towards areas that look more attractive in a slower-growth environment, like the US.

Increasing our exposure to European equities was the first step away from that approach for some time. We did it because we think the improving macroeconomic backdrop could lead to Europe’s exports benefitting from rising demand in China.

Supportive policies from the European Central Bank (ECB), including the prospect of fiscal stimulus, are also potentially positive for European equities. A change at the top hasn’t signalled a change of direction. The new ECB president Christine Lagarde used her first official speech this month to confirm her commitment to the direction set by her predecessor, Mario Draghi.

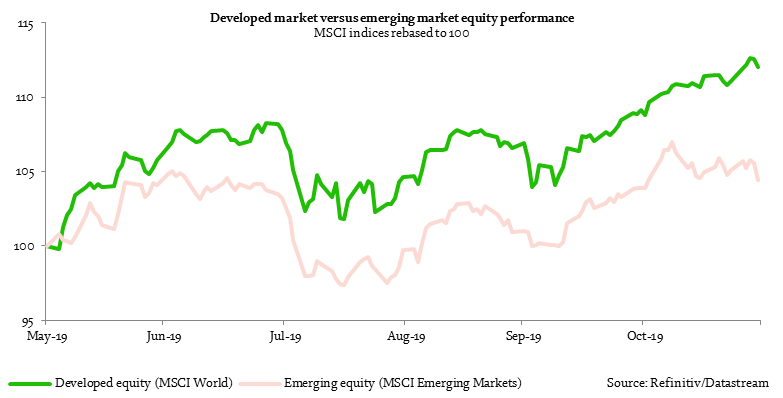

Political upheaval affects emerging markets

Politics has hurt emerging market bonds and equities in recent months. Examples include the Hong Kong protests and political disruption in Latin American countries such as Chile, Colombia and Peru.

We have a low exposure to emerging market equities, with some selective positions in China and Russia where we see particular opportunities. While the improving macroeconomic environment could be beneficial for the region, and a degree of political risk is part and parcel of investing in emerging markets, we remain cautious for the time being.

We are also keeping a close eye on the US dollar as the currency has huge influence over the fortunes of emerging market assets.

When investing, past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can go down as well as up, and you may not recover the amount of your original investment.

-

Market Performance

Market Performance

![]()

Important: This graph shows a very isolated period of past performance. For further context of historic performance over the last five years, please see below. As always, past performance should not be taken as a guide to future performance.

Equity Markets Performance (%tr*, local) 12 month performance to end September As at 30 November 2019 Current -1M -3M YTD 2019 2018 2017 2016 2015 Developed Equity (MSCI) 1,761.59 3.2 7.7 25.2 3.5 12.9 18.6 11.2 -0.2 MSCI UK 2,102.83 1.8 2.6 13.4 2.8 5.9 11.1 18.5 -5.9 MSCI UK Large Cap 1,023.79 1.3 1.6 11.8 3.3 6.5 11.2 21.1 -9.1 S&P 500 3,140.98 3.6 7.9 27.6 4.3 17.9 18.6 15.4 -0.6 Nasdaq Composite 8,665.47 4.6 9.1 31.9 0.5 25.2 23.7 16.4 4.0 DJ EuroStoxx 399.34 2.8 7.9 25.6 5.1 0.3 23.3 3.6 3.9 Nikkei 225 23,293.91 1.6 13.3 18.7 -7.8 20.8 26.0 -3.6 9.4 Hang Seng 26,346.49 -2.0 3.1 5.6 -2.7 4.4 23.0 16.1 -5.9 Emerging Equity (MSCI) 58,288.49 0.6 5.2 12.0 0.2 3.0 22.2 13.4 -6.8 BRIC (MSCI) 699.13 1.2 6.3 15.5 3.3 3.6 26.6 14.5 -6.0 Source: Datastream, all returns in local currency; *tr=total return, including reinvested dividends.

Bond Markets 10-year yield* Performance (%, local) 12 month performance to end September As of: 30-Nov-19 -1M -3M YTD 2019 2018 2017 2016 2015 US Treasury index 1.76 -0.5 -1.8 5.1 8.0 -3.7 -3.9 1.7 1.2 UK gilts index 0.86 -1.2 -2.8 6.7 11.7 -2.0 -7.2 10.5 5.9 Eurozone govt bond index 4.40 0.3 1.7 9.3 8.1 -9.7 -2.7 6.1 -2.0 US investment grade index 2.87 -0.1 -0.9 10.3 8.7 -5.3 -2.3 4.1 -3.4 US high yield index 5.59 0.1 -0.1 7.6 1.0 -3.0 2.4 7.5 -9.1 Source: Barclays indices; Datastream; *current yield on benchmark 10-year Treasury, gilt and bund respectively.

Commodity Markets Performance (%, dollar) 12 month performance to end SepteMBER As of: 30-Nov-19 Current -1M -3M YTD 2019 2018 2017 2016 2015 Dow Jones-AIG Commodity Index (TR) 163.75 -2.6 0.6 2.5 -6.6 2.6 -0.3 -2.6 -26.0 Brent oil price (spot, US$ per barrel) 64.50 8.8 5.5 27.6 -26.3 45.1 18.4 2.0 -50.2 Gold bullion (spot, US$ per ounce) 1,461.54 -3.2 -4.4 14.1 23.7 -7.2 -2.9 18.6 -8.1 Dow Jones Industrial Metals (TR) 236.35 -4.9 -2.7 3.8 -2.1 -2.4 24.0 3.7 -25.3 Source: Datastream

Source: Coutts & Co.

When investing, past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can go down as well as up and you may not recover the amount of your original investment.

SHARE

About Coutts investments

With unstinting focus on client objectives and capital preservation, Coutts Investments provide high-touch investment expertise that centres on diversified solutions and a service-led approach to portfolio management.

Discover more about Coutts investmentsMost Popular

-

CIO Update – Managing risk amid periods of uncertainty | Insights | Coutts

10 Oct 20253 min Whether financial markets ever face a downturn again in the future isn’t a matter of ‘if’ but ‘when’. While it’s impossible to predict the exact moment, managing risk in our portfolios in advance of future events is fundamental to our investment philosophy and process. Read our latest CIO update.

Whether financial markets ever face a downturn again in the future isn’t a matter of ‘if’ but ‘when’. While it’s impossible to predict the exact moment, managing risk in our portfolios in advance of future events is fundamental to our investment philosophy and process. Read our latest CIO update.

-

How could the Budget affect your inheritance planning? | Insights | Coutts

08 Oct 20254 min Coutts Wealth Structuring Manager Irene Wolstenholme and Head of Specialists Greg Kyle-Langley have assessed the current tax landscape and what might change in the upcoming Autumn Budget. They share their view on key considerations when planning for the future.

Coutts Wealth Structuring Manager Irene Wolstenholme and Head of Specialists Greg Kyle-Langley have assessed the current tax landscape and what might change in the upcoming Autumn Budget. They share their view on key considerations when planning for the future.

Related stories

When you become a client of Coutts, you will be part of an exclusive network.