Mid-year investment outlook 2025

Mid-year investment outlook 2025

Past performance should not be taken as a guide to future performance. The value of investments and the income from them, can fall as well as rise, and you may not get back what you put in. You should continue to hold cash for your short-term needs.

-

1 The year so far

The year so far

![tariff-disruption]()

Tariff disruption

It has been an eventful first six months of the year to say the least. But if you were somehow cut off from all news in 2025 and just saw where markets ended the first half, you would not be aware anything happened.

Investors’ focus this year has been centred on tariffs the US imposed on trading partners which were much more drastic and disruptive than expected. Those tariffs have since been either increased, reduced, or rescinded in the pursuit of comprehensive trade deals.

Examining the consequences of these tariffs, we have witnessed equity markets enter a bear market on an intraday basis, the Volatility Index (VIX) at one stage pricing in 4% expected daily moves in the US equity market, financial institutions cutting risk positions amidst recession fears, and investor and consumer sentiment mirroring levels seen during Covid and the Great Financial Crisis in 2008.

The recovery

By mid-year, global equities had regained all losses and the VIX has come back in line with its long-term average. And while sentiment is still poor, the hard economic growth data remains robust and the labour market appears firm.

At Coutts, we have stayed invested through the cloudier sentiment, and eschewed what would have proved a premature reduction of risk had we acted in the throes of peak volatility.

Where are we now?

Hard data shows that real wages continue to grow, unemployment remains low, consumers continue to spend, and household and corporate balance sheets remain healthy. Critically, corporate earnings expectations remain positive, led by the US and Japan.

Recession?

Undeniably, downside risks have increased. First, erratic policymaking in the US – the fulcrum of global finance and markets – acts as gravity for global economic growth. Recession is not our base case, but the probability of it occurring has increased, and that’s true whether trade deals are made or not. Second, inflation remains above target. This leaves less room for the monetary cavalry to ride to rescue as it has done so reliably over the last decade and a half.

Therefore, and in line with the output from our cycle process, we believe it is imprudent to maintain the same conviction on risk taking as we had coming into the year, so have reduced some of our exposure to risk. We will – as always – continue to follow our process. Should the risks dissipate and expected returns grow more favourable, we will add risk back to portfolios. Equally, if volatility persists and risks skew asymmetrically to the downside, we will continue to take profit and bolster our defences.

POLICY IMPACT

Peak policy uncertainty – and peak performance impact – came in April as a result of the trade tariff announcements made on ‘Liberation Day’. As well as equity market volatility, bonds markets have also endured choppiness through the course of this year. This has been caused by discussions around tax cuts, budget deficits, the tariff-related inflation impact, and concerns about political intervention at the Federal Reserve from the White House.

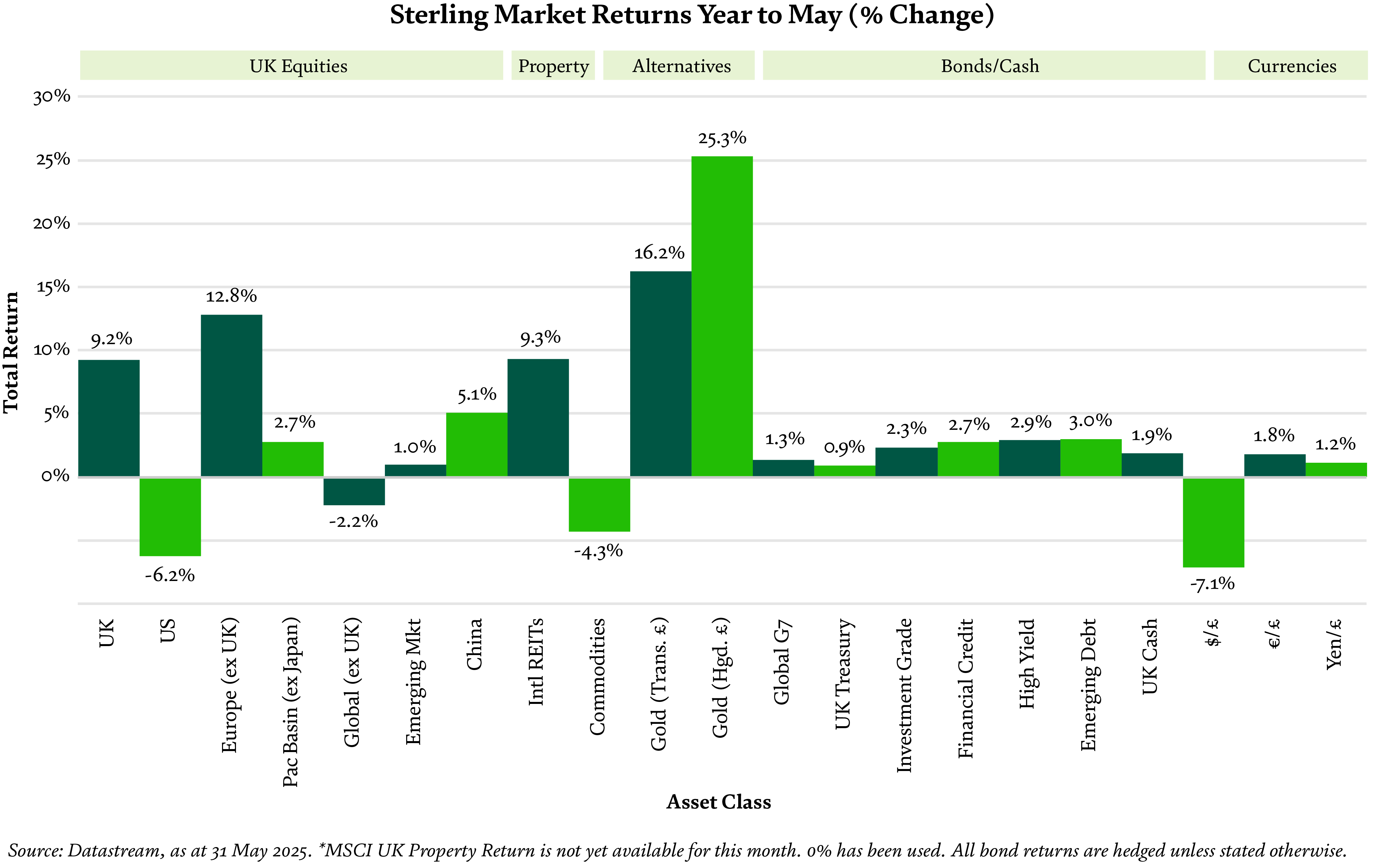

US dollar weakness has played out through the period. Hence, even though global equities are positive this year when measured in US dollars, the reverse is true when measured in sterling. In addition, US equities lagged compared to their global counterparts.

![sterling-market-returns-years-to-may-%-change]()

Standing firm

Since October 2023, we have held an overweight position in global equities. As a result of the unsettled market condition we saw in April, this overweight positioning in portfolios was uncomfortable during that month.

However, holding our nerve and leaning into the investment process proved to be beneficial as the equity market recovered when President Trump rolled back reciprocal tariffs for 90 days and trade negotiations ensued.

![standing-firm]()

DIVERSIFIERS PROVIDE BALLAST

Liquid alternatives - The allocation to liquid alternative strategies has outpaced global bonds year-to-date to the end of May, while displaying lower levels of volatility.

Sterling hedge - Hedging US dollar exposure into sterling mitigated the impact of dollar weakness.

Active management - Our allocation to an actively managed US equity fund dampened the negative market outcomes in April and has maintained outperformance into the market recovery.

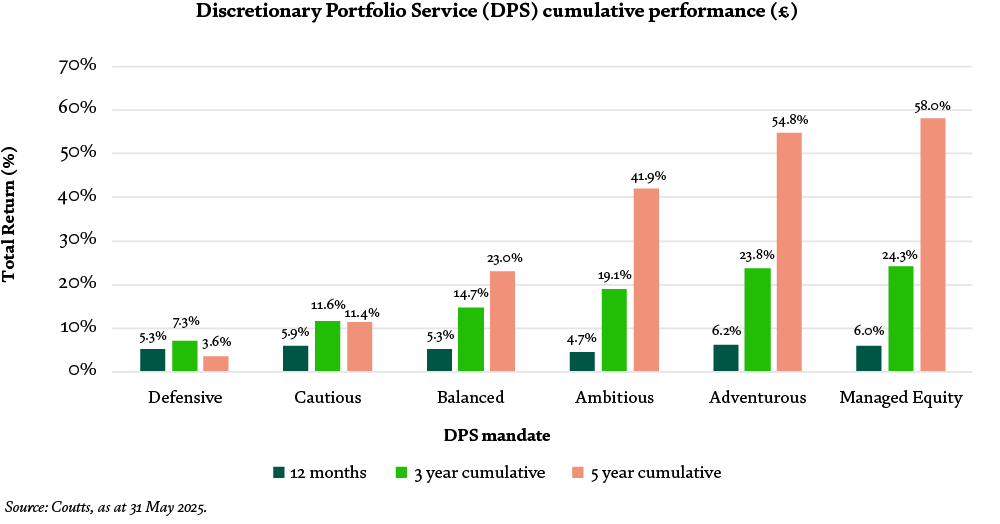

We should be mindful that this is a short period of time that has been particularly marked by President Trump’s erratic policy. Over longer time horizons, investment performance outcomes are smoother and less wide-ranging.

![discretionary-portfolio-service-dps-cumulative-performance]()

-

2 anchor and cycle

Anchor and Cycle

A DIFFERENTIATED PROCESS

Our core optimism remains, resulting in a moderately overweight risk stance. This is informed by the dispassionate analysis of our ‘Anchor and Cycle’ processes. Anchor and Cycle are two complementary engines within our investment strategy, each focused on a distinct time horizon.

Our Anchor process calculates the expected risk premia of various assets – how much additional returns an asset is expected to make depending on its varying risk levels. Essentially, whether the juice is worth the squeeze.

Realised risk premia are generally positive but are highly variable over time. Our analysis finds that for long-term investors, starting valuations and long-term growth/inflation trends are the key to understanding the variation on risk premia.

Our Anchor process seeks to lean into assets when the expected compensation for owning them for the next five years is above average.

The Cycle aspect focuses on shorter-term investment performance which is more influenced by shifts in the business cycle, and their impact on investor sentiment and corporate earnings. Our research has found that the cyclical variation in growth, inflation, and policy interact to drive asset class performance over the short- to medium term (12-18 months).

Diversified decision-making

The independence of our Anchor and Cycle process creates an inherent diversification within our investment decision-making. There will be times when the dispersion of asset class expected returns is low, and so the Anchor opportunity set will be low. At these times our Cycle process may dominate the portfolio.

There will also be times when cyclical trends mean that the Cycle opportunity set will be limited. At these times, the portfolio may rely more on our Anchor process.

Currently, Anchor suggests global equities are still not cheap, while other asset classes remain roughly fair value. In Cycle, we remain in a ‘slowdown’ regime, which is a favourable environment for risk taking.

Contrarian stance

Anchor is our long-term strategic model, designed to allocate across core asset classes when we expect them to deliver superior risk-adjusted returns over time.

Anchor typically takes a contrarian stance, with decisions primarily driven by valuations and the long-term outlook for growth and inflation. Valuations play an important role in this framework, serving as the starting point for positioning over a three- to five-year horizon, where their explanatory power is strongest.

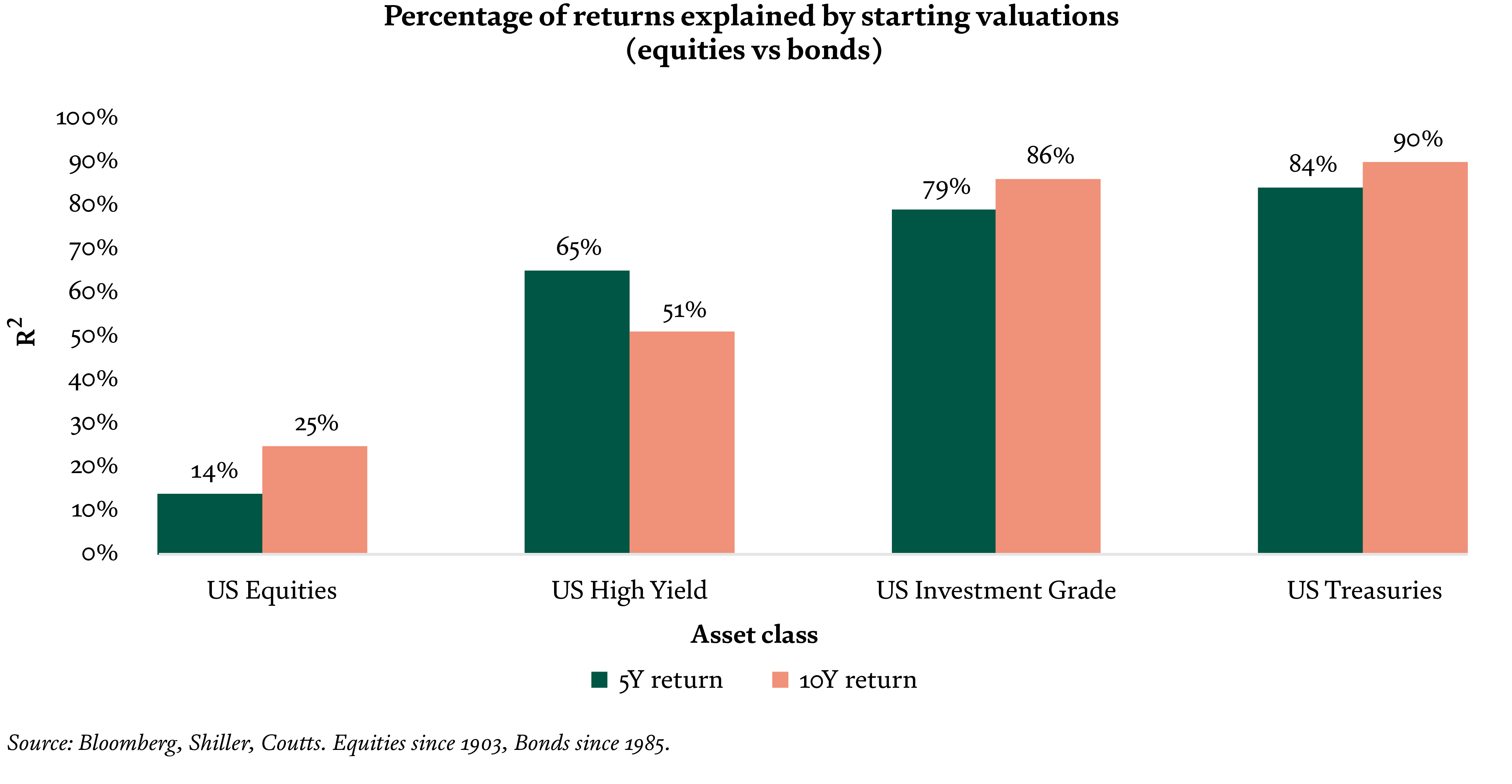

The graph below shows what percentage of actual returns can be explained by starting valuations for equities (price/earnings ratio) and bonds (yield to maturity), using the R2 of their linear regression. It’s more challenging to forecast expected returns for equities compared to bonds by simply using price/earnings. Factors such as earnings and margins for example typically influence share prices over the course of five years and beyond.

This relationship is particularly robust for fixed-income assets but much weaker in the equities market. Our analysis found that on average, just 14% of US equities’ five-year returns could be explained by their initial valuations compared to 84% for US government bonds.

![percentage-of-returns-explained-by-starting-valuations]()

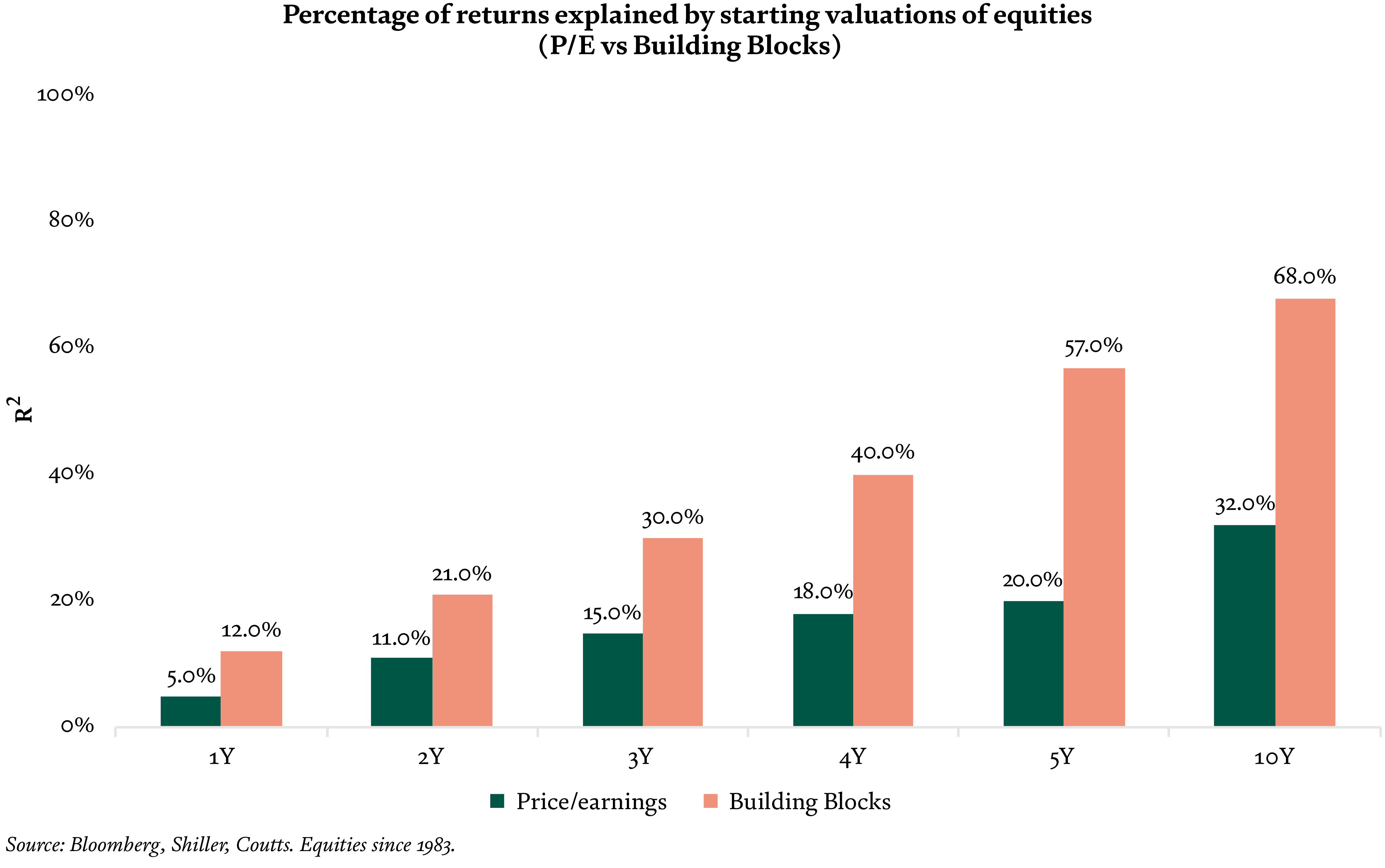

To help improve the visibility of equity forecasts, we complement valuations with our own building blocks which include forward-looking expectations for growth and inflation. This provides a broader insight into the drivers of expected return than valuations alone.

![perentage-of-returns-explained-by-starting-valuations-of-equities]()

This process focuses on identifying opportunities that may be overlooked in the short term. In volatile markets, we can examine the output of our Anchor process daily to ensure we are not missing attractive opportunities.

Tactical allocation

Cycle is our tactical, shorter-term engine. It captures opportunities across and within asset classes by responding to anticipated shifts in the macroeconomic environment and corporate earnings landscape.

Given the inherently dynamic nature of its drivers, Cycle positions are more actively managed and span a broader set of asset classes than those in Anchor. Operating over a 12–18-month horizon, this framework recognises that valuation signals are weak in the short term, while factors such as earnings momentum, investment sentiment, and the prevailing macro regime are much more influential.

We allocate toward risk-seeking assets when the macroenvironment is expected to support corporate earnings and sentiment, shifting toward defensive positions when conditions appear more challenging.

![tactical-allocation]()

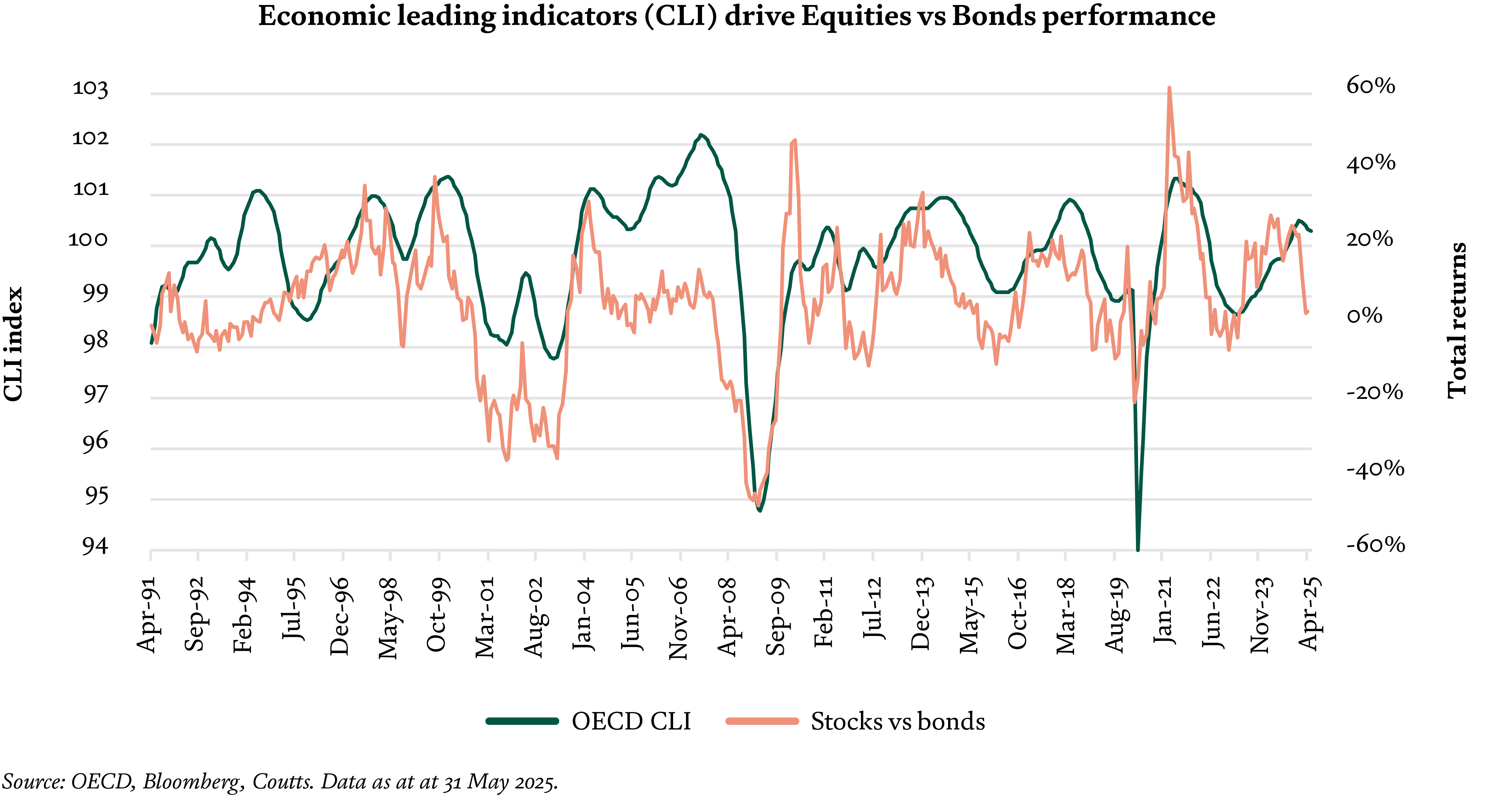

![economic-leading-indicators-drive-equities-vs-bonds-performance]()

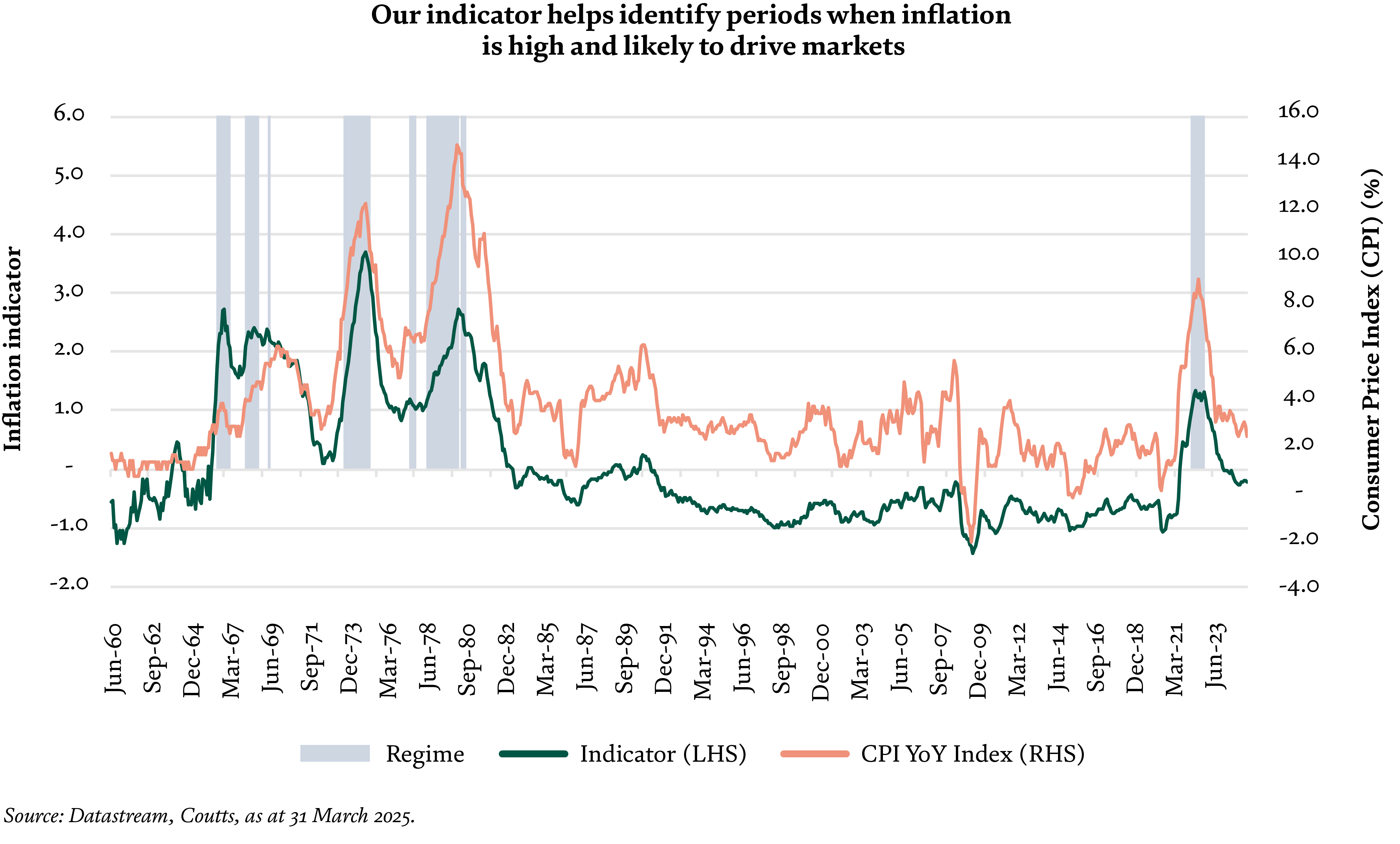

![our-indicator-helps-identify-periods-when-inflation-is-high-and-likely-to-drive-markets]()

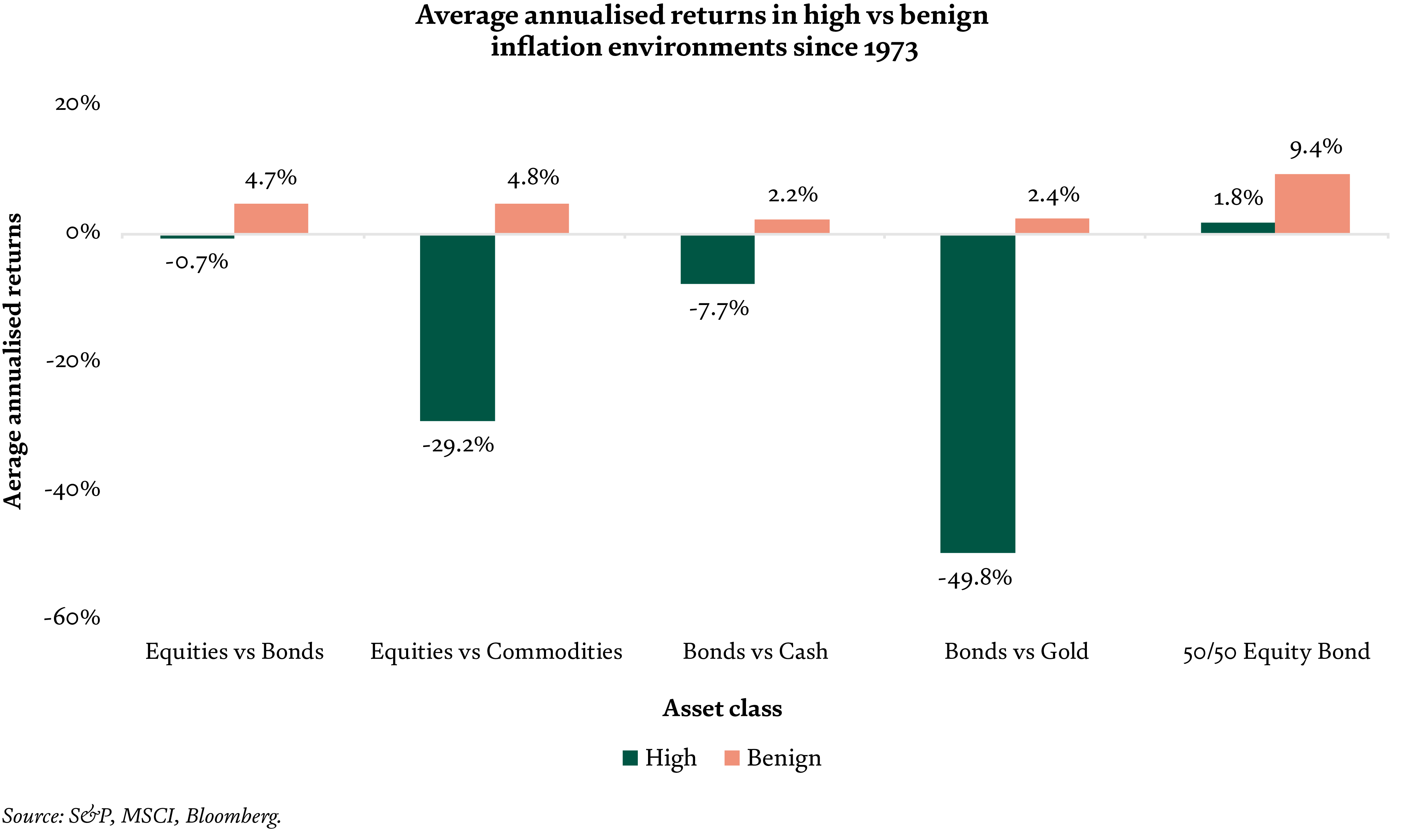

Our analysis has found that inflation plays a more nuanced role in shaping asset price performance compared to growth. Our focus is on identifying when inflation becomes a significant concern for economies and begins to prompt unanticipated policy action, and therefore influence asset class performance.

![average-annualised-returns-in-high-vs-benign-inflation-environments-since-1973]()

-

3 what has worked well for us

What has worked well for us

![]()

STRATEGIC UPDATES

Over the past couple of years, we have made several key changes to our portfolios after our investment process identified attractive opportunities.

Overweight global equities

In 2023 equity markets corrected roughly 10% between July and October over concerns around the path of inflation and interest rates. Our analysis found that recession probability was declining given the end of central bank hiking cycles and corporate earnings were set to grow over the following year. Given this, the correction represented a good opportunity to increase our equity exposure in portfolios, which we did. We maintained this position until May 2025, when we took profits and halved the overweight, given elevated economic uncertainty.

High yield

Given more attractive valuations in high yield compared with equity markets, in December 2023 we diversified our overweight to risk assets by adding a high yield position alongside the existing equity overweight. High yield valuations were highly attractive, with yields in excess of 8%. Buying high yield bonds when yields are at these levels has historically led to very attractive long-term returns, with very high probability of positive returns over the medium-term. In addition, the quality of the high yield index has improved over the last two decades, which meant that we felt valuations were particularly attractive in the context of the potentially structurally lower default risk.

Gold

In late 2023, sticky inflation, geopolitical tensions and record fiscal debt in developed market economies meant that we felt that the diversification properties of gold would be attractive in a portfolio context. We therefore reduced our exposure to government bonds in favour of an allocation to gold. We took profits in Q3 2024, given better-than-expected performance of the position.

Liquid alternatives

We added a liquid alternatives fund to our portfolio in July last year to further diversify our asset allocation. Equities and bonds had been more highly correlated to each other than typical in a volatile manner. Liquid alternatives aim to operate outside of this traditional tide by adopting a range of techniques and financial instruments, such as short-selling. This has been one of our strongest performing allocations amid the turmoil in H1.

-

4 our outlook

Our outlook

FUNDAMENTALS IN FOCUS

We take a top-down approach within our investment strategy, identifying which regions offer the most potential for returns. This is largely based on the fundamentals such as earnings announcements and forecasts.

Artificial intelligence

Macroeconomic noise has been elevated in 2025 but it is important not to lose sight of the earnings picture and the ongoing advancements within the technology sector. Although uncertainty persists regarding geopolitical, economic and fiscal policies, over the long-term, the implications of artificial intelligence (AI) on productivity will be a dominant driver of equity market outcomes.

Companies in a range of industries mentioned the impact AI is having on their efficiency during their Q1 earnings call, in areas ranging from coding to customer service to marketing. The earnings impact of this secular theme has been huge, and we think this can continue. We are overweight US equities, which is the most direct beneficiary of this theme.

Japan

Share buybacks in the Japanese equity market were up 70% year-over-year in 2024 (source: NikkeiAsia). A share buyback is when a company purchases its own shares to return excess cash to shareholders and to reduce the number of shares in circulation. This has continued in 2025, with buybacks for the first four months of the year equating to ¥6.9 trillion (£35.3 billion), more than twice the level at this point in 2024. Importantly this has occurred despite the uncertain economic environment Japanese businesses face.

-

5 portfolio positioning

Portfolio Positioning

![managing-risk]()

Managing risk

We remain risk on within portfolios, being overweight equities albeit at a reduced size than we were coming into 2025. Our Cycle analysis suggests we remain in a slowdown phase of the business cycle. This is typically a favourable environment for taking risk, and the fundamentals that have driven the current economic expansion remain in place. Consumers are experiencing positive real wage growth and balance sheets for households and corporates are healthy.

Despite our positive base case, downside risks have increased. Unpredictable trade policy in the US create risks for the economic outlook. On top of this, the potential short-term impact of tariffs on US inflation may force the Fed to be reactive to slowing growth, rather than proactive as they were in 2024.

beyond government bonds

For over two decades prior to the Covid pandemic, the main risk for multi-asset portfolios was a recession. During recessions, central banks respond quickly with rate cuts and so government bonds protect investors – as yields go down, prices go up.

Looking forward, investors face a broader range of potential risks than was the case in the two decades prior to the pandemic. These risks include sticky or volatile inflation and the potential for a fiscal or energy shock to markets.

Government bonds won’t protect against all of these outcomes, meaning there is potential for periods of elevated correlations between bonds and equities. As a result, the case for other diversifying assets to complement government bonds in a portfolio is increased. This is where our allocation to liquid alternatives will be key as we anticipate it to continue offering much of the diversification it has over the past year.

Sterling

Our house view is positive on sterling, which has risen roughly 6% versus the dollar since we moved overweight in late January. Our long-term process continues to suggest the dollar is 15- 20% overvalued versus sterling based on purchasing power parity (PPP). PPP is the economic theory that states that in the long run, exchange rates between currencies should adjust so that identical goods cost the same in different countries.

Importantly, our currency framework has a time horizon of three- to five years, and so our forecasts reflect a reset in the value of the dollar over the next few years, rather than an immediate closing of the valuation differential.

Future headwinds

Tariffs will likely have a negative impact on growth and positive impact on inflation. But tariffs are not the only element of the President Trump agenda. Congress continues to work on a fiscal package which will include personal and corporate tax cuts.

The sequencing of Trump’s policies have raised concerns among investors as uncertainty clouds the economic outlook in the near term. But we expect the total growth impact of the administration will be more balanced. This view allowed us to hold our nerve during the worst of the market volatility and remains the case today.

FOLLOWING OUR PROCESS

History tells us that geopolitical flashpoints are often investment red herrings. With some exceptions, they cause volatility but do not prevent market upside in many cases. The appropriate response to these kinds of risks is to not disinvest, but to remain well-diversified.

We focus instead on our repeatable investment process that analyses valuations, growth, earnings, and policy. Geopolitical risks are not going away, we are in the most volatile period for geopolitics in a number of decades. Fortunately, historical analysis shows that previous geopolitical events have not precluded markets from rising over time.

.png "2199434945")

investing with coutts

Manage your investments

Review and manage your investments with us through the online banking portal.

LOOKING TO INVEST?

Learn more about investments, what our experts think and marketing investment offers available from us.

investing with coutts

Manage your investments

Review and manage your investments with us through the online banking portal.

LOOKING TO INVEST?

Learn more about investments, what our experts think and marketing investment offers available from us.